-

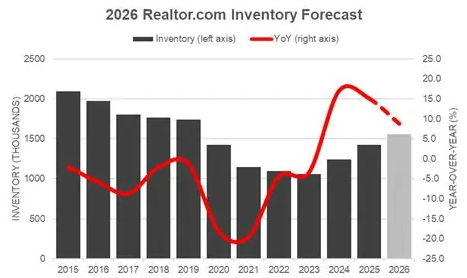

New Housing Bill: What It Could Mean for Homebuyers

This is good news for future home buyers and first time home buyers. Now we just need rates to cooperate.

- More housing supply: The bill is designed to encourage the construction of more homes to help address the nationwide housing shortage.

- Faster development: It includes measures to streamline permitting and reduce barriers that can delay new housing projects.

- Support for affordable housing: Expands programs aimed at increasing affordable housing opportunities for first-time buyers and working families.

- Manufactured housing: Provides additional support for manufactured housing as an affordable homeownership option.

- Potentially more inventory: More homes on the market could help ease upward pressure on home prices over time.

- Not an overnight fix: The impact will take time, but it’s a positive step toward improving housing affordability.

- What it means for buyers: Combined with improving inflation and a more favorable interest rate outlook, increased housing supply could create better buying opportunities in the coming months and years.

Bottom Line: More homes, more choices, and a healthier housing market are good news for buyers, sellers, and the real estate industry. While it won’t change the market overnight, it’s an encouraging step in the right direction.

http://www.YourApplicationOnline.com

-

Podcast Episode: Fed Policy And Market Signals

Pip: Mortgage rates, Fed minutes, oil prices, and a Fed chair who apparently has to talk the board out of hiking rates — welcome to the bond market's version of a group project where nobody agrees on the deadline.

Mara: Today we're working through posts from Jackkammer covering two connected territories: where the Fed actually stands on rates, and what falling oil prices are and aren't doing to inflation and the bond market.

Pip: Let's start with the Fed's internal divide.

The Fed's Split on Rates

Mara: The question here is simple but consequential — when Fed policymakers look at the same economic data, are they actually reaching the same conclusions about what to do next?

Pip: The June 17 meeting minutes answer that pretty directly. Setting up the numbers: "Eight members favored no rate cuts this year, one favored a single cut, and nine projected one rate hike."

Mara: So the upshot is that the Fed is almost perfectly split between holding steady and tightening further — which is not a committee that's going to move quickly in either direction.

Pip: A nearly even split on a body that's supposed to set unified policy — that's a faculty meeting with trillion-dollar consequences.

Mara: What the post calls constructive is that most members still expect inflation to keep easing as oil prices decline and tariff pressures fade. Existing home sales missed expectations, falling 2.4% in June to 4.09 million, and the labor market is softening gradually but holding. The post flags that U.S.-Iran tensions are driving real volatility in Treasury markets, which flows directly into mortgage rate swings.

Pip: Which brings us to the oil side of this — because the Fed's inflation outlook depends heavily on what energy prices actually do.

Oil Prices, Gas Prices, and the Gap Between Them

Mara: The tension in this territory is that falling oil prices are supposed to relieve inflation pressure — but the relief isn't arriving evenly or quickly across the economy.

Pip: The post on Fed chair Kevin Warsh puts the gap in concrete terms: "Oil prices have retraced 98% of their recent increase, but gasoline prices have only fallen back about 46%, and the bond market has recovered just 30%."

Mara: What this means in practice is that consumers and the bond market are both lagging behind what crude oil is already telling us. The structural reason is straightforward — gas prices spike fast when oil rises, but they come down slowly. OPEC+ announcing production increases should accelerate that normalization.

Pip: And that's where Warsh becomes the actual story.

Mara: Right. The post draws a clear contrast: some Fed voting members are pushing for rate hikes, while Warsh has signaled that's not the direction he's taking things. The framing is that Warsh is willing to look at forward-looking data rather than reacting to lagging indicators — which, given how slowly gasoline and bond markets are catching up to oil, matters quite a bit for where rates land.

Pip: Patience as monetary policy. Novel concept.

Mara: The post's conclusion is cautiously optimistic — encouraging signals from both an inflation and bond market perspective, with the reminder that markets move in cycles and the data, watched carefully, points toward improvement.

Pip: So the Fed is divided, oil is ahead of gas prices, and the bond market is somewhere in the middle, catching up.

Mara: The thread connecting both segments is timing — when signals arrive, when markets respond, and whether policymakers read the data forward or backward. Worth watching as those gaps close.

-

PCE new Math starts in September. It’s about time and this is Huge.

A Potentially Big Change in How Inflation Is Measured

The U.S. Bureau of Economic Analysis (BEA) is changing how the Personal Consumption Expenditures (PCE) index measures certain components of inflation.

Why does this matter?

Sometimes what looks like inflation really isn’t.

Here’s an example:

Imagine you have a financial advisor who charges a fee of 1% of your investment portfolio. If the stock market grows and your portfolio value increases, the dollar amount of the advisor’s fee also increases, even though the advisor is still charging the exact same 1%.

Under the current methodology, some increases like this can be reflected as higher prices, even though the percentage charged hasn’t changed. You’re paying the same rate; the underlying asset simply became more valuable.

The updated calculation is designed to remove more of these types of “false inflation” signals so the inflation data better reflects actual price changes rather than increases driven by higher asset values.

Why it matters:

The Federal Reserve pays close attention to PCE inflation when making interest rate decisions. If inflation is measured more accurately and comes in lower as a result, it could support a more favorable outlook for bonds and, ultimately, mortgage rates.

It’s too early to know the full impact, but this change has the potential to be meaningful for financial markets.

Time to get pre-qualified soft credit pull. http://www.YourApplicationOnline.com

-

Fed Bifurcated. It’s a good thing

Market Update

The Fed minutes from the June 17 meeting showed policymakers are nearly split down the middle on the path for interest rates. Eight members favored no rate cuts this year, one favored a single cut, and nine projected one rate hike.

Most Fed members also expect inflation to continue easing as oil prices decline and the impact of tariffs diminishes.

Translation: The inflationary “mess” is expected to continue cleaning itself up.

Existing home sales fell 2.4% in June to a seasonally adjusted annual rate of 4.09 million, missing expectations for a 0.7% increase. The Northeast was the only region to post a gain in sales.

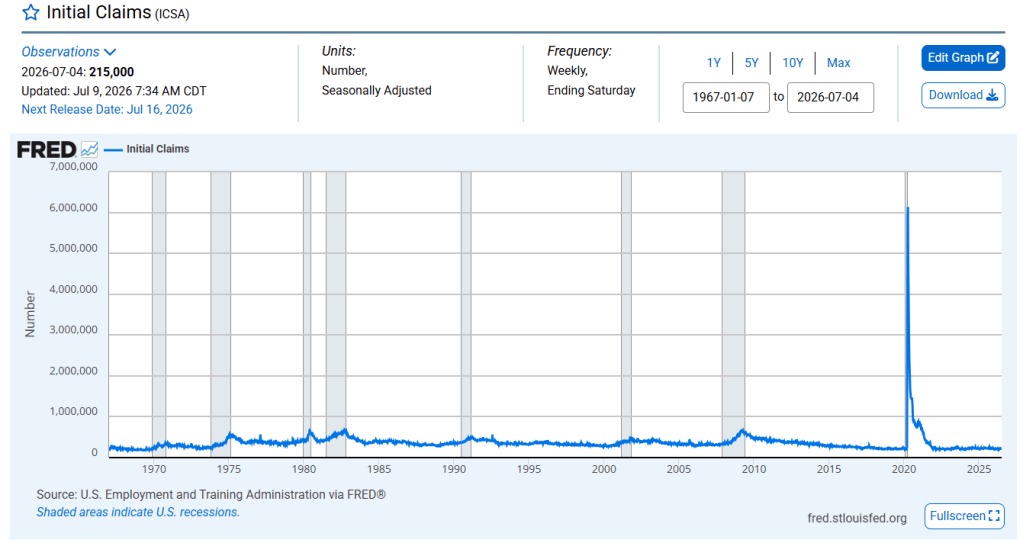

Initial jobless claims remained stable at 215,000, while continuing claims increased by 8,000 to 1.814 million, indicating the labor market is gradually softening but remains resilient.

The ongoing U.S.-Iran conflict continues to create volatility in both the 10-year and 30-year Treasury markets, resulting in significant swings in mortgage rates.

My Take:

The overall picture remains constructive. Cooling inflation, lower oil prices, and a stable labor market are all positive signals for the bond market. While no one can predict exactly where mortgage rates are headed, staying informed and watching the data, not the headlines, can create opportunities. As always, timing matters.http://www.YourApplicationOnline.com

-

Feds Favorite Drug? Rate Hikes! but Warsh is taking it away.

Oil prices have retraced 98% of their recent increase, but gasoline prices have only fallen back about 46%, and the bond market has recovered just 30%.

Gasoline prices tend to rise almost immediately when oil prices increase, but they usually take much longer to come back down. That should begin to improve as OPEC+ has announced plans to increase production.

My take:

These developments are encouraging from both an inflation and bond market perspective.

While no one can predict exactly where interest rates are headed, history reminds us that markets move in cycles. If we pay attention to the data and learn from the past, there appears to be light at the end of the tunnel.

Warsh is a breath of fresh air regarding the true impact of inflation and being able to look forward not backwards. Some Fed voting Presidents want rate hikes. Warsh has signaled that’s not going to happen.

Let’s get you pre-approved today http://www.YourApplicationOnline.com

-

Thanks Beth (Debbie Downer)

Fed voting member Beth Hammack had me scratching my head this week.

First, higher oil prices contribute to inflation… fair enough.

Then came the twist: lower oil prices could also cause inflation because consumers would have more money left over to spend.

So… higher oil prices are inflationary, and lower oil prices are inflationary?

Sometimes it feels like the Fed’s answer is, “No matter what happens, inflation!”

From where most Americans sit, the math seems a little simpler. Higher Fed rates make mortgages, car loans, credit cards, and business loans more expensive. Those higher borrowing costs show up in family budgets every single month.

Maybe it’s time for a few Fed members to spend less time staring at economic models and more time standing in line at the grocery store or making a mortgage payment.

Just a thought.

let’s get you pre qualified http://www.YourApplicationOnline.com

-

WSJ Article, Did they Lie about Borrower Rates? Yes, Higher rate may be the right choice.

Mortgage rates are cyclical, a roller coaster ride. We’ve seen that firsthand over the last year.

Not long ago, the national average 30-year mortgage rate was around 8%. Just a few months ago, it dipped to approximately 5.99%. Today, it’s sitting just under 6.5%.

That’s a significant swing in a relatively short period of time.

I recently came across a Wall Street Journal article claiming homebuyers are losing tens of billions of dollars because they’re overpaying for their mortgages. While it’s an attention-grabbing headline, it oversimplifies how mortgage pricing actually works.

Here’s the nuance.

For the most part, lenders are buying from the same capital markets. The difference isn’t simply who has the “lowest rate.” It’s how that rate is structured and whether it’s the right loan for the borrower.

Some lenders operate with very lean overhead and may advertise lower rates, but they may not have the infrastructure, underwriting support, or operational capacity to consistently meet aggressive closing deadlines.

More importantly, very few borrowers fit into a perfect box.

Some have lower credit scores. Others are self-employed, have limited down payments, investment properties, asset depletion income, or unique qualifying scenarios. Some borrowers expect to refinance within a year, while others plan to keep the loan for decades.

Those differences matter.

A borrower planning to refinance in 12 months may choose a slightly higher rate with little or no upfront cost rather than paying thousands of dollars in discount points to obtain the lowest possible rate.

Another borrower may require a specialty investor whose pricing is slightly higher because the loan carries more risk or falls outside standard agency guidelines.

The lowest advertised rate isn’t always the lowest-cost loan.

The real question isn’t, “Who has the lowest interest rate?”

It’s “Which loan structure saves this borrower the most money over the time they expect to keep the loan?”

That’s the conversation every borrower should be having.

As for the article…it’s behind a paywall. Kind of ironic for a story about overpaying.

Let’s get you pre-approved http://www.YourApplicationOnline.com

-

Dallas Fed Trimmed mean Inflation 2.4% in May. Warsh Fav Benchmark

One of the biggest challenges in economics is making sure you’re watching the dog—not the tail.

It’s easy to get caught up in the latest inflation headline, but the underlying trend often tells a very different story.

That’s one reason the Dallas Fed publishes its Trimmed Mean Inflation measure. Rather than treating every price change equally, it removes the most extreme price movements, both the highest and the lowest, to filter out temporary spikes and localized swings.

The result? A clearer picture of underlying inflation. Instead of reacting to every headline, policymakers can better see the “forest through the trees.”

This is one of the inflation measures many economists watch because it tends to be more stable and may provide a better indication of where inflation is actually headed.

Meanwhile, oil has fallen to around $68 per barrel, continuing to ease inflation concerns and providing support for the bond market. Mortgage bonds are improving this morning, which is helping keep downward pressure on interest rates.

For now, we’re continuing to float our clients while watching the market closely. Volatility can still change the picture quickly, but the overall trend has become more encouraging.

Have a fantastic weekend, and I’ll see you Monday!

http://www.YourApplicationOnline.com

-

PCE High for May but bond market shrugs. That’s so yesterday…

The Personal Consumption Expenditures (PCE) Index, the Fed’s preferred measure of inflation, rose 0.4% in May as expected. On a year-over-year basis, inflation increased from 3.8% to 4.1%.

At first glance, that’s not great news. However, much of this increase reflects the surge in oil prices we’ve experienced over the past several months. In many ways, the market has already priced this in. It’s yesterday’s news.

Now it’s time for a little GDP math. Look away if you’re squeamish.

The formula for GDP is:

GDP = C + I + G + (X – M)

Where:

- C = Consumer Spending

- I = Investment

- G = Government Spending

- X = Exports

- M = Imports

The interesting part of the latest GDP revision is that growth was revised higher because imports came in lower than previously estimated.

Why does that matter?

Imports are subtracted from GDP. So when the U.S. imports less, there is less of a negative drag on economic growth. Think of it as removing an anchor from the boat, the economy doesn’t necessarily speed up, but it isn’t being pulled down as much.

The takeaway is that the stronger GDP number wasn’t driven by consumers suddenly spending more or businesses investing aggressively. Instead, it was largely a result of trade math.

Lower oil prices, easing geopolitical tensions, and moderating energy costs continue to be the bigger story looking forward. The market is always focused on what’s next, not what already happened.

let’s get you pre-qualified http://www.YourApplicationOnline.com

-

$70 a Barrel, Rates follow slide down

Oil prices are now sitting around $70 per barrel this morning, a significant improvement from the recent highs and getting much closer to the pre-conflict levels near $56.

Mortgage rates have improved as well, but not nearly as fast as oil prices have fallen. The reason? The Federal Reserve remains cautious. While lower energy prices are certainly helpful, policymakers are still concerned about the inflationary impact from the past several months when oil prices were elevated. The Fed wants more evidence that inflation is sustainably moving lower before becoming less restrictive.

Housing data this morning reflected the impact of higher rates.

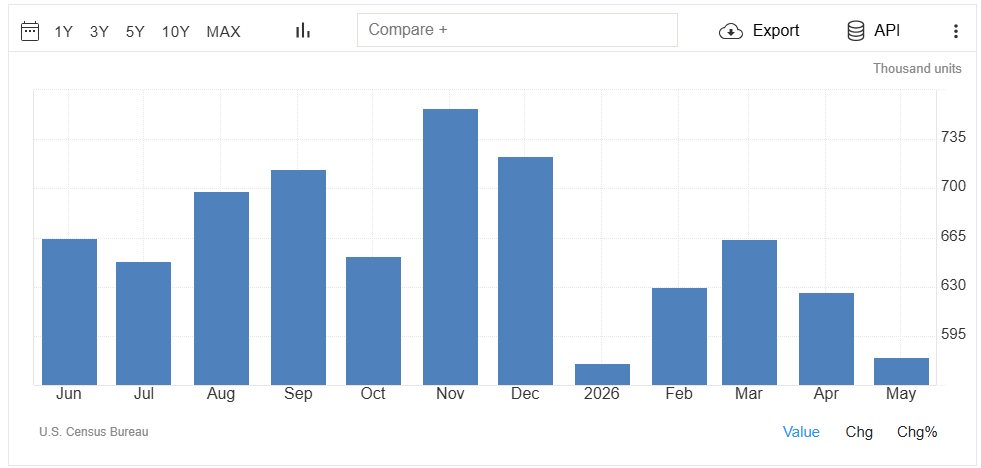

New Home Sales, which measure signed contracts on newly constructed homes, fell 7.3% in May. The West led the decline, down a substantial 27%, suggesting affordability challenges and elevated mortgage rates may be causing some buyers to pause.

Mortgage application activity remains relatively unchanged. Buyers continue to shop for homes, but many appear to be waiting for a clearer signal on the direction of interest rates before making a move.

The takeaway?

Lower oil prices are a positive development and should help the inflation story over time. However, the Fed is focused on where inflation is headed, not where oil prices are today. Until policymakers gain confidence that inflation is under control, rates may be slower to fall than many consumers expect.

For now, the market is balancing improving inflation prospects against a Fed that remains firmly focused on price stability.

http://www.YourApplicationOnline.com

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.