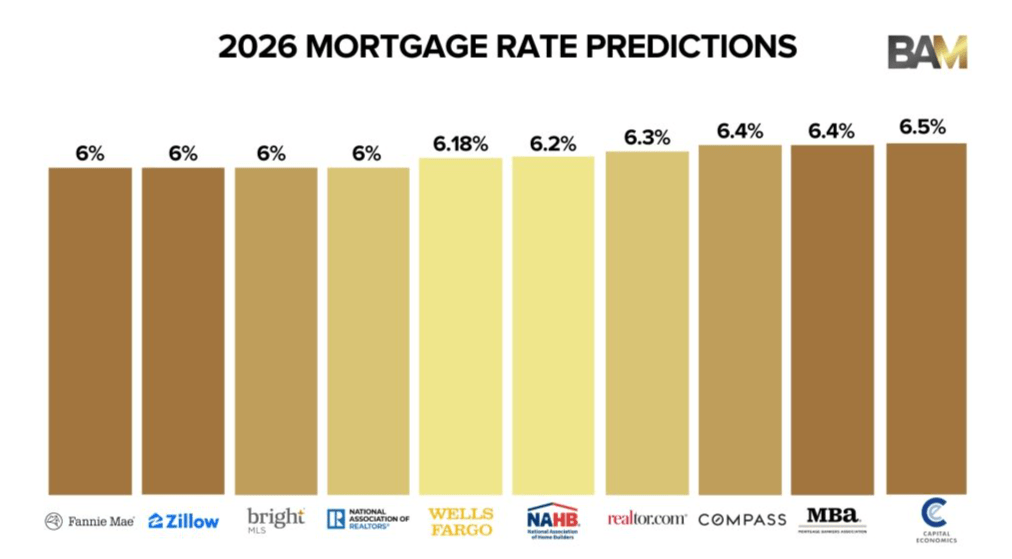

Mortgage rates are cyclical, a roller coaster ride. We’ve seen that firsthand over the last year.

Not long ago, the national average 30-year mortgage rate was around 8%. Just a few months ago, it dipped to approximately 5.99%. Today, it’s sitting just under 6.5%.

That’s a significant swing in a relatively short period of time.

I recently came across a Wall Street Journal article claiming homebuyers are losing tens of billions of dollars because they’re overpaying for their mortgages. While it’s an attention-grabbing headline, it oversimplifies how mortgage pricing actually works.

Here’s the nuance.

For the most part, lenders are buying from the same capital markets. The difference isn’t simply who has the “lowest rate.” It’s how that rate is structured and whether it’s the right loan for the borrower.

Some lenders operate with very lean overhead and may advertise lower rates, but they may not have the infrastructure, underwriting support, or operational capacity to consistently meet aggressive closing deadlines.

More importantly, very few borrowers fit into a perfect box.

Some have lower credit scores. Others are self-employed, have limited down payments, investment properties, asset depletion income, or unique qualifying scenarios. Some borrowers expect to refinance within a year, while others plan to keep the loan for decades.

Those differences matter.

A borrower planning to refinance in 12 months may choose a slightly higher rate with little or no upfront cost rather than paying thousands of dollars in discount points to obtain the lowest possible rate.

Another borrower may require a specialty investor whose pricing is slightly higher because the loan carries more risk or falls outside standard agency guidelines.

The lowest advertised rate isn’t always the lowest-cost loan.

The real question isn’t, “Who has the lowest interest rate?”

It’s “Which loan structure saves this borrower the most money over the time they expect to keep the loan?”

That’s the conversation every borrower should be having.

As for the article…it’s behind a paywall. Kind of ironic for a story about overpaying.

Let’s get you pre-approved http://www.YourApplicationOnline.com