-

CPI Report Higher Inflation. US Combat Operations continue uncertainty

What markets want and really what everyone wants, is a little more certainty. Right now, there are still a lot of unanswered questions surrounding the conflict and where the markets head from here.

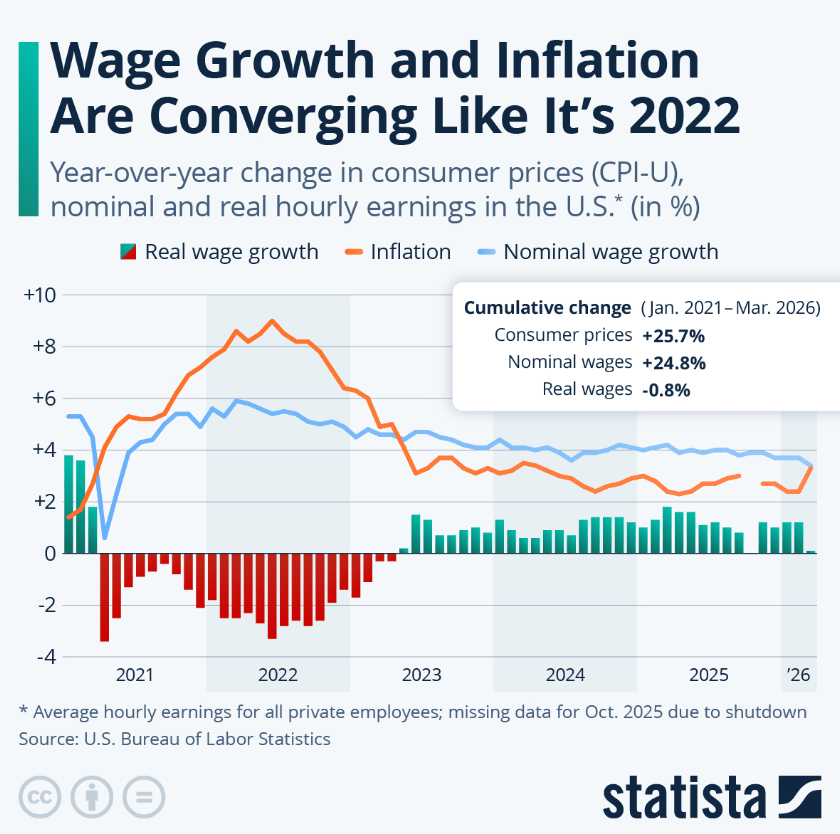

What we do know is that inflation has been trending higher, which was reflected in the latest Consumer Price Index report. That’s not especially surprising considering gas prices are now more than a dollar higher than they were just a couple of months ago, with energy costs still remaining elevated.

Oil prices touch almost every part of the economy. From transportation and shipping to groceries and everyday goods, higher energy costs tend to gradually work their way into consumer prices over time.

That’s also why the bond market and mortgage rates tend to react so closely to moves in oil. As inflation pressures rise, interest rates often follow.

The good news is markets can shift quickly, and any easing in energy prices or geopolitical tension could help improve the outlook moving forward.

We are seeing a great deal of activity regardless and this shows a strong economy and tight inventory. Let’s get you pre-qualified today.

http://www.YourApplicationOnline.com

-

BLS report Strong but Credibility Weak. Is BLS BS? Time will tell.

We’re starting the day with oil prices lower, stocks higher, and mortgage bonds improving , all positive signs for interest rates this morning.

The BLS Employment Report showed 115,000 jobs created versus expectations of 62,000, which the markets are taking as encouraging news overall. That said, the BLS data is survey-based and tends to be more volatile than the ADP payroll data, which is based on actual payroll processing.

So while we’ll take the positive headline, it’s probably best viewed with a small grain of salt.

For now, improving energy prices and stronger bond performance are helping mortgage rates move in the right direction.

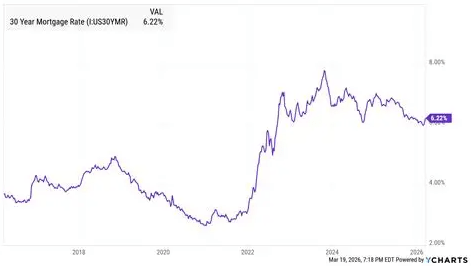

National Average mortgage rates below.

http://www.YourApplicationOnline.com

-

Oil and Rates are Married if they want to or not. Rate improvement on the horizon.

Oil prices and mortgage rates are umbilically connected whether we like it or not. Energy is one of the fastest ways inflation moves through the global economy, and inflation is the silent enemy of value over time.

When oil spikes, transportation, manufacturing, shipping, and consumer costs all rise with it. That pressure flows directly into inflation data, which pushes bond yields higher and forces mortgage rates to react.

It’s why a conflict thousands of miles away can change the monthly payment on a home purchase here almost overnight.

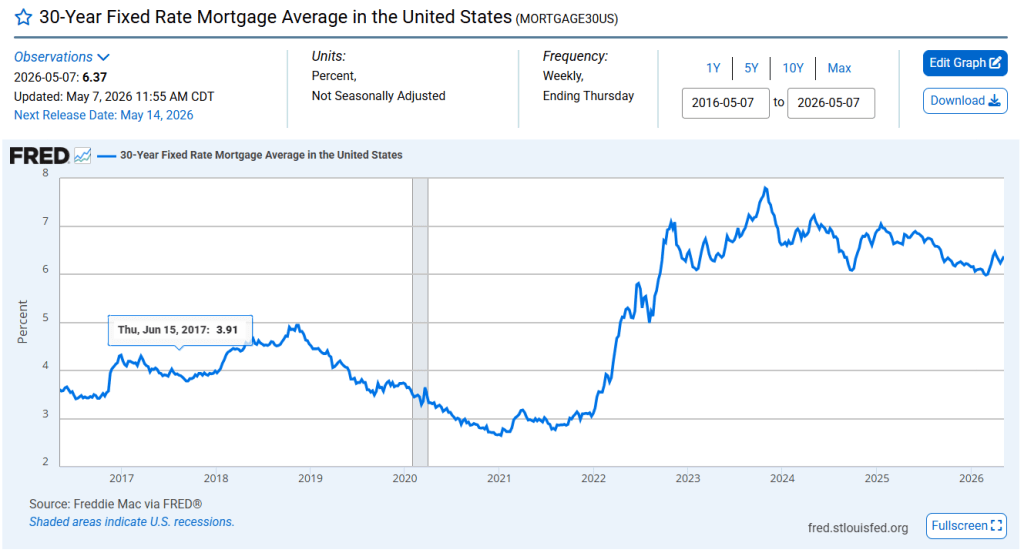

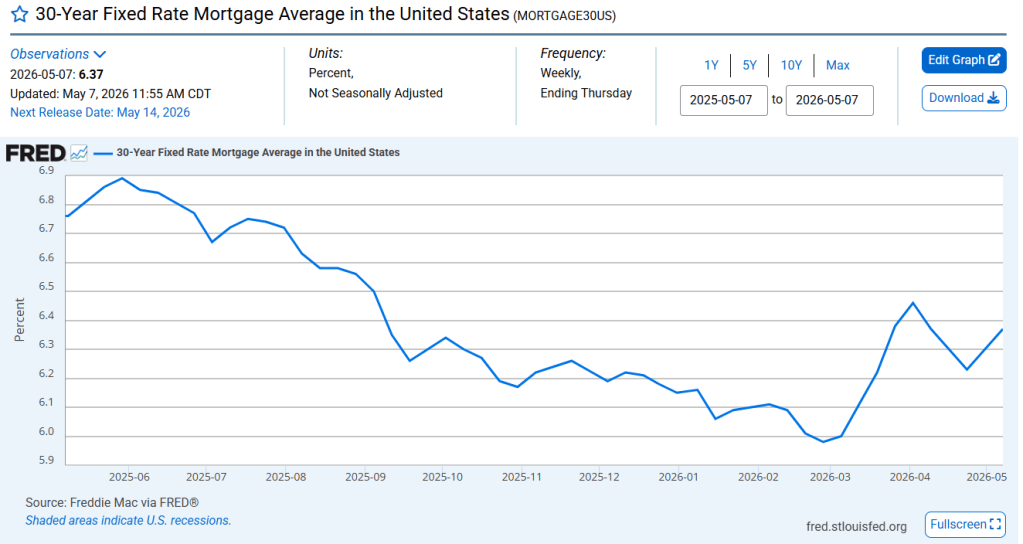

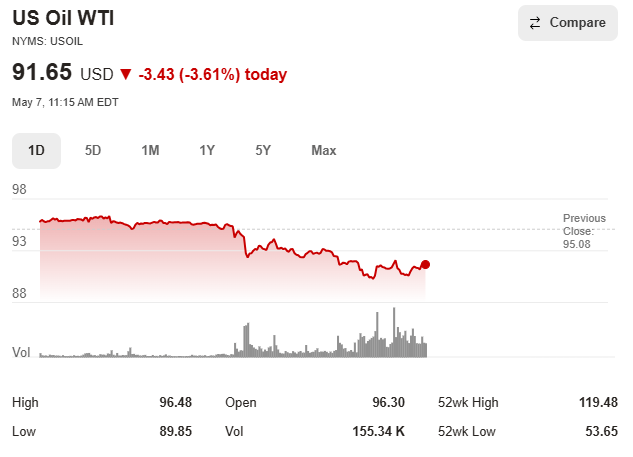

Two months ago, oil traded below $60 a barrel and mortgage rates were comfortably in the 5’s. Today, elevated geopolitical tension has driven energy prices sharply higher, and the bond market has repriced risk just as quickly.

The reality is simple:

Lower energy costs create breathing room for inflation to cool. Cooling inflation helps bonds recover. Stronger bonds help mortgage rates improve.In today’s market, oil is no longer just an energy story, it’s a housing story.

Employment Data Revelio Labs show private payroll date 66,000 jobs created in April, though low, it is a positive. Jobless claims rose 10,000, again low but not a negative number.

We are projecting rates to improve as the Iran conflict subsides.

http://www.YourApplicationOnline.com

-

Oil Prices down on Hopes of Peace deal, rates follow. Will it stick?

The markets, both here and globally, are essentially holding their breath, waiting to see if the Strait of Hormuz reopens and oil prices retreat back toward pre-conflict levels under $60 a barrel.

And it’s worth remembering, just two months ago we were seeing mortgage rates comfortably in the 5’s.

That shift highlights just how quickly geopolitical risk can ripple through energy, inflation, and ultimately borrowing costs.

The ADP Employment Report came in stronger than expected, though still modest by historical standards. We’ll take it, 109,000 jobs added, with small businesses leading the way.

Mortgage applications dipped week over week but remain about 5% higher than this time last year. Even with rates averaging around 6.45%, that’s roughly 40 basis points lower than a year ago, enough to keep some demand in the market.

http://www.YourApplicationOnline.com

-

Oil is acting like a Throttle pushing everything higher. Longer read but concise. Feel free to share.

Home sales are pushing higher despite rising interest rates, largely driven by the ongoing shortage of available inventory.

At the same time, builders have started adjusting prices to keep sales moving, but overall, the median home price has remained relatively stable, highlighting the balance between limited supply and steady demand.

Oil is now trading well over $100 a barrel with no clear signs of meaningful easing. Just two months ago, we saw prices dip below $60, and mortgage rates followed, briefly dropping under 6%.

Since then, the conflict with Iran has changed the entire trajectory.

Oil has surged to multi-year highs due to supply disruptions and ongoing tension in the Middle East, particularly around the Strait of Hormuz. That matters because energy prices feed directly into inflation, and inflation is the single biggest driver of interest rates.

Here’s the chain reaction playing out in real time:

- Conflict disrupts oil supply

- Oil prices spike

- Inflation expectations rise

- The Fed stays higher for longer

- Bond yields increase

- Mortgage rates move up

We saw this almost immediately, rates jumped from below 6% to the mid-6% range as the conflict escalated.

And the longer this conflict drags on, the more it shifts from a short-term shock to a structural issue. The IMF is already warning that prolonged conflict could push oil toward $125 and keep inflation elevated globally.

How this hits housing:

- Affordability gets squeezed (higher monthly payments)

- Buyer demand softens at the margins

- Sellers hesitate → inventory stays tight

- Builders adjust pricing to keep volume moving

So you end up with a strange but very real dynamic:

slower activity, but stable pricing, because supply never really loosens.

Bottom line:

You’re not just watching an oil story, you’re watching a rate story. And right now, oil is acting as the throttle.If oil stays elevated, mortgage rates aren’t coming down in any meaningful way. If oil cools, rates will follow pretty quickly.

Time to get pre-qualified http://www.YourApplicationOnline.com

-

Rental Prices drop, 19% of income. but inventory tightening

We’ve seen over the past year a noticeable slowdown, and in some areas, a decline, in rental prices.

It’s a classic push and pull. When rents drop, affordability improves and demand picks up.

As more consumers re-enter the market, available inventory tightens, which eventually puts upward pressure on prices again.

That cycle is the nature of a free market. Prices adjust based on supply and demand, rarely staying too low or too high for long. The key is timing, what feels like relief today can shift back to pressure tomorrow as the market rebalances.

Realtor.com is showing active listing s are up 6% in April and 4.5% year over year. It’s spring and buyers and sellers are on the move.

http://www.YourApplicationOnline.com

-

Where are Interest Rates headed?

We’re in a precarious position. Persistently high oil prices don’t just show up at the pump, they work their way through the entire economy.

Transportation costs rise, supply chains get more expensive, and businesses eventually pass those costs on to consumers. That’s how energy feeds directly into broader inflation.

So far, consumer behavior hasn’t shifted dramatically, which has helped cushion the immediate impact. But over time, that resilience tends to fade. Higher costs begin to erode purchasing power, margins get squeezed, and both consumers and businesses start to pull back.

If elevated energy prices stick around, the longer-term effect is difficult to ignore: sustained inflation pressure, tighter financial conditions, and an increased likelihood of an economic slowdown, or even a recession.

Trying to make sense of all the moving pieces, the cause and effect across oil, inflation, and rates, can feel overwhelming.

On one hand, oil prices could fall and provide some near-term relief. But some of the impact is already baked in, higher energy costs have likely worked their way into inflation and broader pricing.

If that pressure slows the economy enough and we tip into a recession, history suggests rates would come down. The challenge is the timing: the inflation hit tends to show up first, while rate relief usually comes later.

Always feel free to reach out and have a fantastic weekend. http://www.YourApplicationOnline.com

-

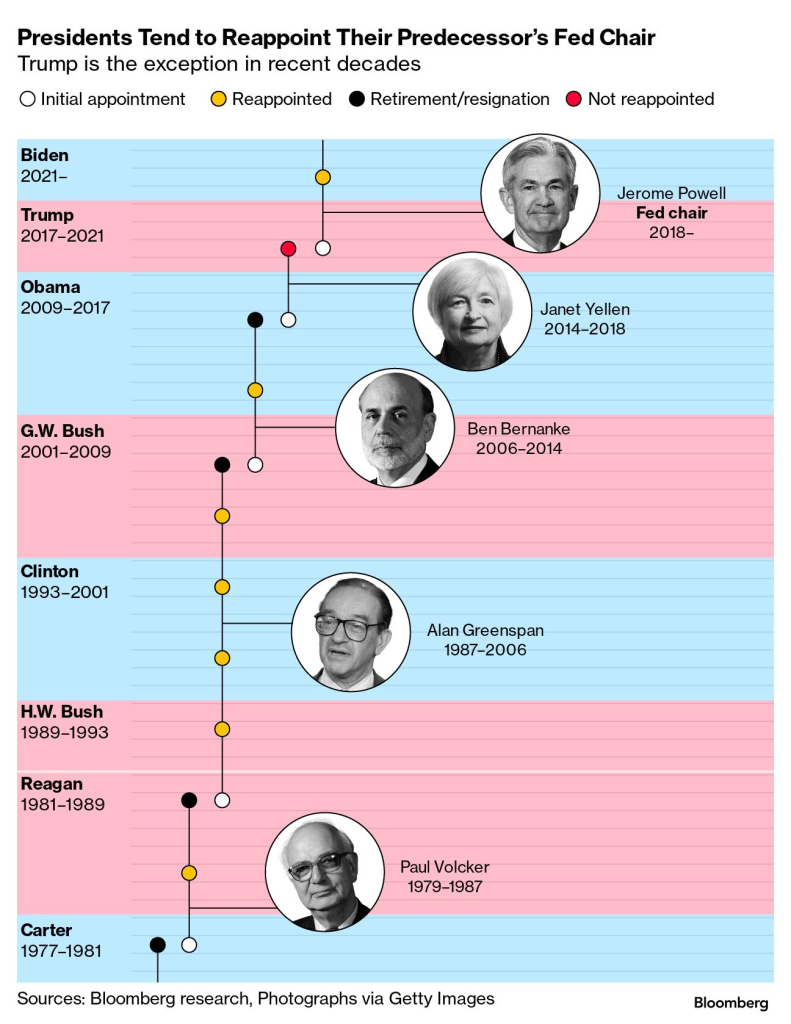

Will he say or Will he go now… He’s staying….

The last time a Fed Chair stayed on beyond their expected transition period dates back decades (1948), so naturally the question is, why stay now?

At the moment, it appears less about precedent and more about unfinished business. With ongoing scrutiny and broader questions surrounding Federal Reserve policy and decision-making, there’s a sense that the job isn’t quite done. Until those issues are fully addressed, Jerome Powell is likely to remain in place to provide continuity and stability.

From a market perspective, that stability matters. The bond market, and ultimately mortgage rates, prefer a steady hand at the wheel. Any uncertainty at the top of the Fed can translate into volatility across interest rates.

So for now, Powell staying put isn’t just about history, it’s about navigating a very complex economic moment where consistency may be more valuable than change.

Time to get pre-qualified http://www.YourApplicationOnline.com

-

One Tweet and Oil prices go up along with Mortgage Rates.

Oil prices have a direct impact on mortgage rates because inflation is the enemy of value over time.

When energy costs rise, it filters through the entire industry, transportation, goods, and services all become more expensive.

That upward pressure fuels inflation, and inflation pushes bond yields higher… which ultimately drives mortgage rates up.

So now what?

For the moment, we wait. Gas prices are sitting at a four-year high, and if this trend holds, we could see inflation reaccelerate just as it was starting to cool.

That puts the Federal Reserve in a tough spot. The market wants rate cuts, but rising inflation tied to energy costs makes that much harder to justify.

Bottom line: we want the Fed cutting rates, but oil may have other plans.

http://www.YourApplicationOnline.com

-

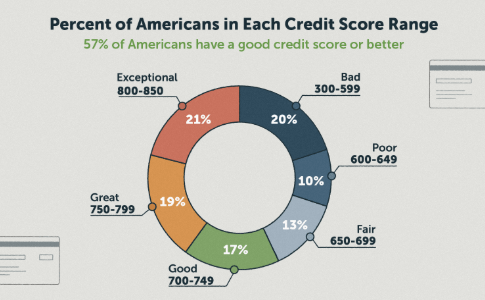

New Fed Chair Coming and what’s VantageScore an alternative FICO, 33 Million new consumers!

Oil prices are edging slightly higher, while stocks and mortgage bonds are down just a bit, net result: mortgage rates are essentially flat for now.

On the Fed front, attention is turning to the path forward following Jerome Powell’s upcoming meeting this Wednesday. Leadership expectations are shifting, with Kevin Warsh being discussed as a potential next Fed Chair in the near term.

Why VantageScore matters

In short, VantageScore is designed to be more inclusive. It captures roughly 33 million more consumers than traditional FICO score models, with about 10 million of those scoring 620 or higher.

Back in 2018, Congress passed the Credit Score Competition Act, opening the door for models like VantageScore 4.0. The focus is on stronger predictive power and broader inclusion.

At its core, a credit score is meant to predict future behavior. With advancements in AI, the industry is moving toward more dynamic and inclusive underwriting, potentially expanding access to home financing for millions of borrowers.

Time to get pre-qualified http://www.YourApplicationOnline.com

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.