-

He who Controls the Spice Controls the Universe – Frank Herbert, Dune

Today, the spice is oil, and the control lies in the potential and current disruption of critical global shipping channels.

Oil is not just another commodity, it is the lifeblood of global trade, manufacturing, and transportation.

Any instability in the movement of oil through major shipping corridors can quickly drive up energy prices, which in turn raises costs across nearly every sector of the economy. As a result, markets react swiftly, with investors closely watching these developments because the impact reaches far beyond energy, it influences inflation, global trade, financial markets, and ultimately interest rates.

Mortgage rates are higher this morning, as expected, though certainly not welcomed. Until the current unrest and supply disruptions begin to ease, markets will likely remain volatile. Once stability returns and those pressures subside, we should see rates gradually move lower again.

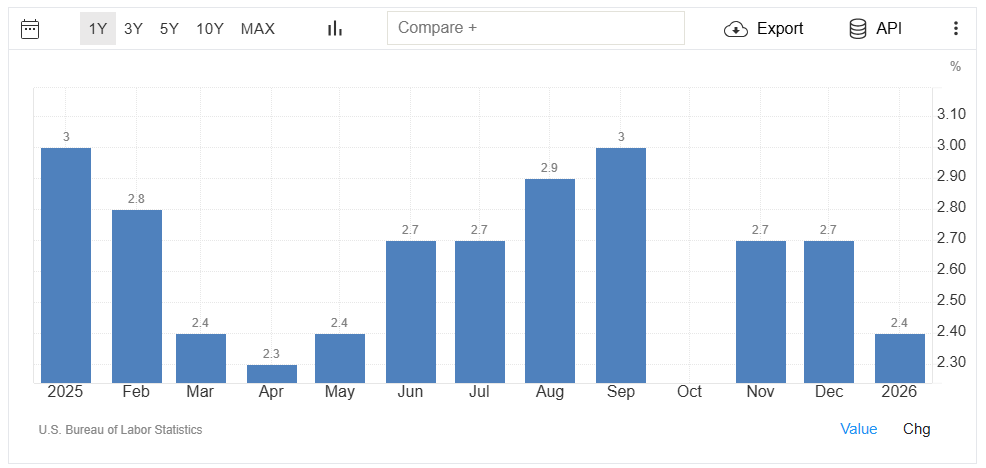

Consumer Price Index cam in as excepted at 2.4% year over year. Shelter rose 0.2% the lowest level in 5 years. Good news for inflation.

Hang in there, rates will come down as will gas prices eventually.

Time to get pre-qualified http://www.YourApplicationOnline.com

-

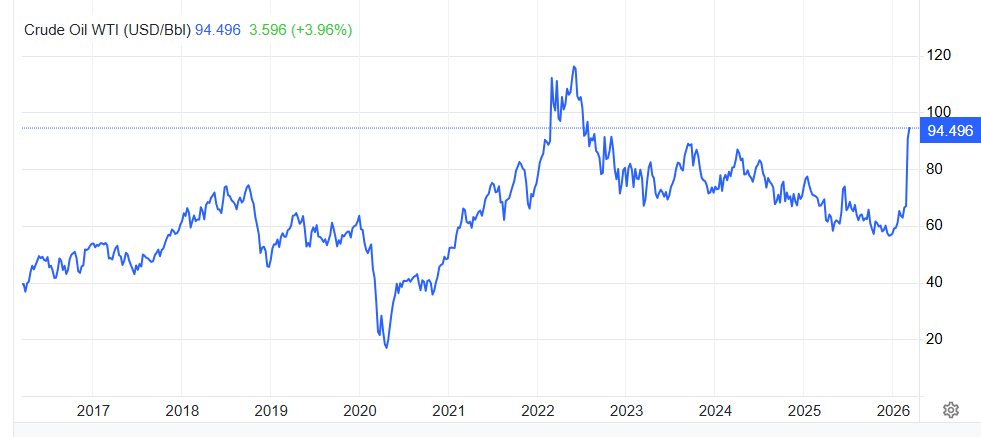

Oil and Rates Move Lower as Markets See Signs of Easing Iran Tensions

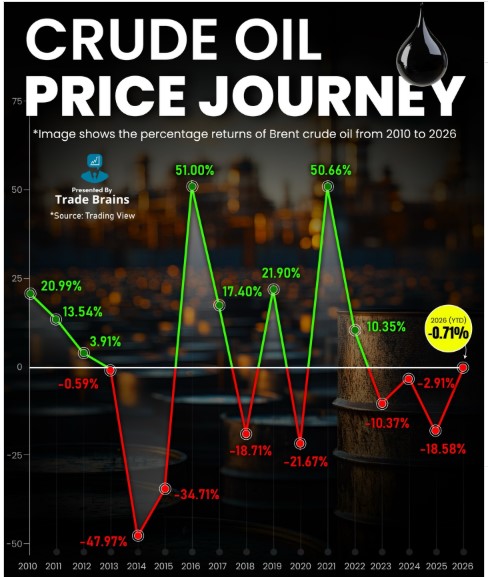

Did we hit the peak? Oil is now trading roughly 10% lower than Monday’s highs. While it is still averaging just under $90 per barrel, the trend is moving in the right direction.

As oil prices move lower, interest rates tend to follow, since energy costs play a major role in inflation. Rates have not yet returned to the lows we saw at the end of February, but the momentum is improving.

In housing, existing home sales rose 1.7%, despite expectations for a 0.5% decline. The main driver continues to be interest rates. When rates begin to improve, buyers quickly notice and the urgency to purchase returns.

The job market, however, remains challenging. The latest ADP employment report showed job growth, but March is still averaging around 60,000 to 70,000 new jobs, which is considered a relatively soft number by historical standards.

Overall, we are beginning to see early signs of stabilization, but markets are still working through the recent volatility.

More Employment numbers to come this week. Stay tuned.

http://www.YourApplicationOnline.com

-

What goes Up must come Down. G7 Oil Reserves pending Release ease markets.

“This too shall pass” is worth reminding ourselves.

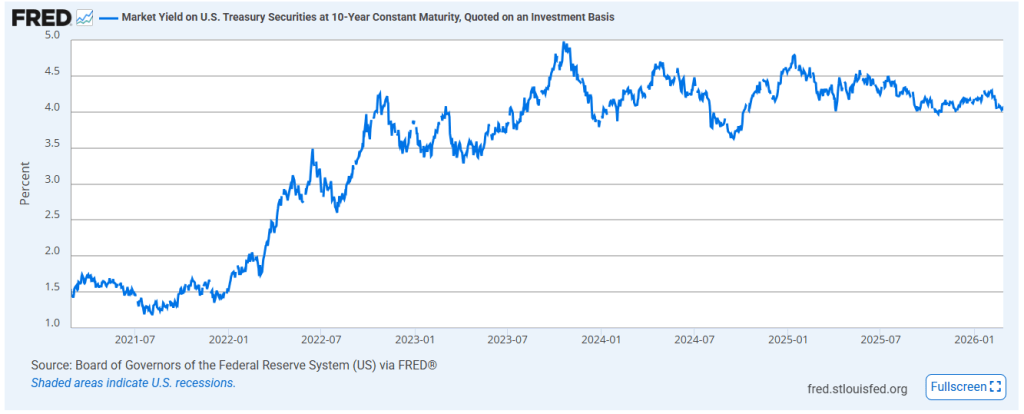

We have lost a lot of rate ground in a very short period of time, with the 10‑Year Treasury Yield spiking above 4.17% after being near 3.96% just last week. That move represents roughly a two-thirds percent increase in rates in just five days.

Markets often react quickly to uncertainty, especially when global tensions and inflation concerns collide.

The G7’s discussion of a potential Strategic Oil Reserve release has helped calm energy markets after the initial spike in oil prices. The signal to increase supply, if needed, has taken some pressure off inflation expectations and helped stabilize bond markets.

It’s shaping up to be a busy economic week, with several key reports that could influence interest rates:

- Tuesday: ADP Employment Report

- Wednesday: CPI – Consumer Price Index (inflation)

- Thursday: Weekly Jobless Claims

- Friday: PCE Inflation Report (the Federal Reserve’s preferred inflation gauge)

These reports will provide important insight into labor market strength and inflation trends, both of which play a major role in determining the direction of Treasury yields and mortgage rates.

If inflation continues to cool, it could help reinforce the case for lower rates as we move into the spring.

Website http://www.YourApplicationOnline.com

-

Significant Job Losses, While Oil Prices Weigh on Bonds! Shiny Ball syndrome

The market’s primary focus right now is the rise in oil prices, a bit of a “shiny ball syndrome”.

Meanwhile, the stock market is down again this morning, and the latest BLS jobs report showed a loss of 90,000 jobs, compared to expectations of 50,000 new jobs.

The war involving Iran is also pushing global tensions closer to a breaking point. This level of uncertainty creates a challenging environment for both professional and individual investors.

In times like these, many investors look for a “flight to safety,” often turning to precious metals such as gold, silver, and platinum as defensive assets. Historically, geopolitical instability tends to drive demand for these metals as investors seek to preserve value during volatile periods.

However, even safe-haven assets have limits. Markets can only absorb so much uncertainty before volatility spreads across all asset classes. Much like a pitcher that can only hold so much water, when the pressure builds too high, even traditionally stable investments can begin to show strain.

Mortgage rates are holding steady for now, though just barely. As market volatility begins to settle, rates should gradually follow and move lower. Position yourself for the potential rate improvements many expect as we move further into the spring.

http://www.YourApplicationOnline.com

-

Iran, Oil Prices, Bond market sell offs, Oh My…. Oh I forgot Inflation.

On a positive note, well, perhaps a realistic one, we continue to navigate a challenging financial and global market environment.

History consistently shows that these periods of volatility do pass.

As conditions stabilize, bond yields typically move lower, mortgage rates follow, and oil prices tend to settle back down.

Patience and perspective are important and needed.

Where do I see things going from here? Given that we’ve lost nearly 0.25% in interest rate improvement this week, my expectation is that it could take roughly another month for rates to work their way back to the levels we saw prior to the Iran conflict.

Higher oil prices tend to push inflation higher because energy is a core input in nearly everything, manufacturing goods, transporting products, and powering supply chains. When energy costs rise, it increases the cost of producing and moving goods throughout the economy.

As inflation expectations rise, bond investors demand higher yields, which in turn pushes mortgage rates higher in the short term. The good news is that historically these geopolitical shocks tend to be temporary, and as markets stabilize, oil prices and bond yields typically settle back down.

Our Team can get you ready for Spring and Summer http://www.YourApplicationOnline.com

-

Calm at least for the Oil and Bond market. Job Numbers better but not best.

As we discussed yesterday, markets often react in predictable patterns. The initial shock has begun to wear off, with both the oil and bond markets stabilizing. If this trend continues, it should support mortgage rates gradually moving back toward the lows we saw last Friday.

ADP Employment Report came in with 63,000 jobs created, a bit stronger than the 50,000 expected but still w weak number. Let’s break it down.

The lion share came from Education/Health Services. a whopping 58,000 jobs. These jobs are not economically sensitive meaning it’s a stable baseline of employment regardless of the economy.

Remember last week when the BLS reported 130,000 new jobs? ADP has now revised its January numbers down from 22,000 to 11,000.

What does this tell us? It points to a softer labor market, with less aggressive hiring and reduced competition among companies for talent. Revisions like this are often early indicators of a slowing economy.

From a rate perspective, a cooling job market can ease inflationary pressure, which is generally supportive of lower interest rates.

Time to get pre-qualified http://www.YourApplicationOnline.com

-

Markets are reacting Emotionally but thinking Strategically. The argument for $120 a barrel.

Tensions between the United States and Iran have sharply escalated. What was geopolitical pressure is now open conflict, with the U.S. taking direct action and Iran responding in kind.

The situation has widened beyond these nations, pulling in and destabilizing the broader region.

Energy markets are reacting, global security feels more fragile, and the sense of uncertainty is real. Compared to last week, the stakes feel higher and the margin for error much smaller.

The argument for $120 a barrel is real. How is the supply replacement, including potential releases from strategic reserves and how quickly mobilized?

We’ll feel this at the gas pump sooner rather than later. Energy is a major component of inflation, and the Federal Reserve is watching closely.

Bond yields have climbed, reversing most of the rate gains we’ve seen over the past two weeks. History suggests geopolitical spikes like this eventually cool off the bigger question isn’t if things settle down, but when.

http://www.YourApplicationOnline.com Mortgage Pre-Approval soft credit pull.

-

Where Oil Prices Go, So Do Interest Rates: Iran Tensions Add Fuel, No Flight to Safety

We may have expected a bond/securities flight to safety this morning, but history suggests otherwise.

If we look back:

- Qasem Soleimani Assassination (2020): Oil jumped from $60 to $66 per barrel (+$6), while the 10-year Treasury increased 10 basis points.

- October 7 attacks (2023): Oil moved from $82 to $90 (+$8), and the 10-year rose 30 basis points.

- 12-Day War (June 16, 2025): Oil climbed from $74 to $83 (+$9), with the 10-year increasing 10 basis points.

The pattern: geopolitical shocks pushed oil higher, and instead of a sustained flight to safety into bonds, yields moved up alongside energy prices.

In all of these cases, oil prices and yields eventually settled back to prior or even lower levels once the initial shock faded.

We also have a busy week ahead for financial and labor market data. That reporting will likely have a far greater impact on rates than this morning’s oil-driven volatility.

Economic fundamentals especially inflation and jobs ultimately carry more weight than short-term geopolitical price spikes.

Let’s get you pre-qualified http://www.YourApplicationOnline.com

-

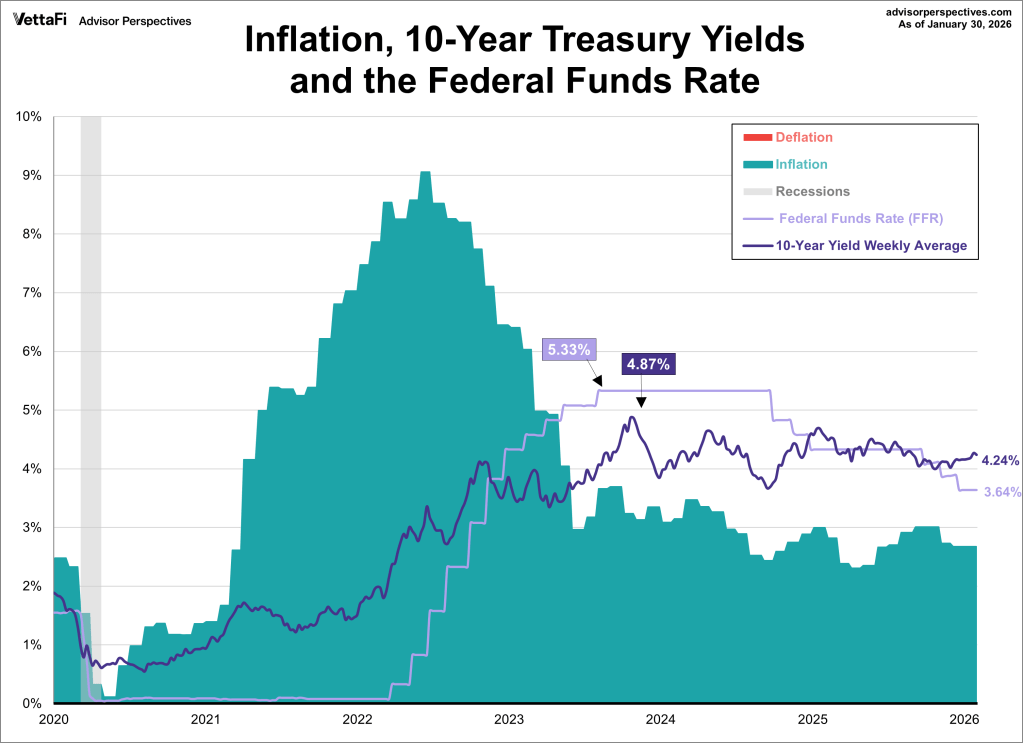

10y Bond Under 4%. Hold please.. Inflation numbers challenging

The stock market is down, and bond yields are following, which means mortgage rates continue to improve. We officially broke through the 4.00% yield floor, hitting 3.971% as of this morning.

That’s good news.

However, rates now need to hold these gains.

The biggest challenge? The latest Producer Price Index (PPI) report.

- Headline inflation rose 0.5% (we expected 0.3%).

- Year-over-year inflation declined to 2.9%, but expectations were 2.6%.

In short, inflation is cooling, just not as fast as projected.

What does that mean? Less motivation for the Fed to cut rates. They remain laser-focused on inflation.

Now this next part is important.

The Bureau of Labor Statistics (BLS) jobs report has a major influence on economic policy, but job growth has been overstated. The primary issue is something called the “Birth-Death Model.” This model estimates job creation from new businesses opening (births) and subtracts estimated losses from businesses closing (deaths).

Here’s where it gets interesting:

In April, May, and June of 2025, the Birth-Death model added 74,000 jobs to payroll estimates.

Today’s updated data shows the actual number was a negative -321,000 jobs.

That’s an overstatement of 395,000 jobs.

The sheer breadth of these downward revisions is staggering.

So what does this mean for interest rates?

Lower.

When economic data weakens and job growth is revised down significantly, investors move money into safer assets like bonds. That “flight to safety” pushes bond prices up and yields down, which ultimately helps mortgage rates improve.

We just need the bond market to keep believing the trend.

Time to get pre-qualified, soft credit pull. http://www.YourApplicationOnline.com

-

Lagging Data Overstates Inflation, Increasing Pressure on the Fed to Cut Rates 10-Year Yield at 4% Floor Nearing Breakthrough

Continuing the theme from earlier this week, the 10-year Treasury yield, which closely tracks mortgage rates, keeps pressing against a key support level. It’s tested that floor multiple times, and momentum suggests a potential break lower next week.

Geopolitical events, particularly involving Iran, could trigger a classic flight to safety into bonds, pushing yields down further. However, because Iran is part of OPEC, any escalation could also drive oil prices higher. That creates a competing pressure: rising energy costs can fuel inflation, especially since transportation and manufacturing remain heavily dependent on oil.

In short, bonds are leaning toward lower yields, but oil and inflation risks could complicate the move.

Time to get ready to refinance or purchase. Our team is nationwide and ready to go. http://www.YourApplicationOnline.com

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.