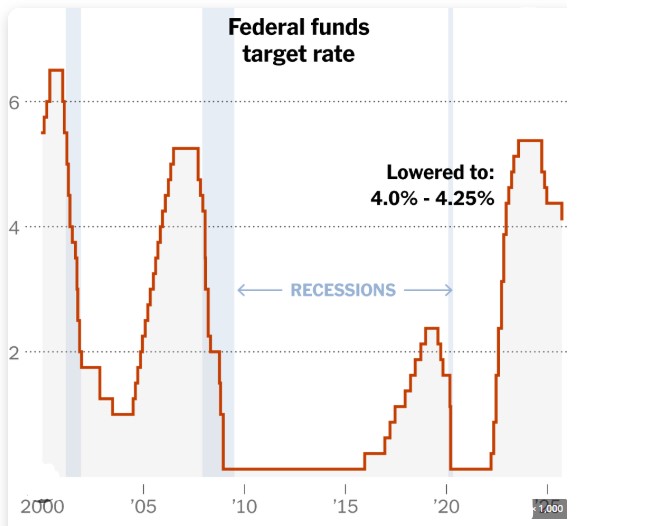

The Feds cut rates this week, just as everyone expected but they did it in a noticeably more dovish tone.

In plain English, that means they’re more open to another rate cut, but they’ve set the bar higher. We’d need to see inflation continue to cool and the labor market weaken further before they pull that trigger again.

Powell also noted that the BLS jobs report may be overstating employment growth by roughly 60,000 jobs per month, suggesting the labor market is softer than the headline numbers imply. With next week’s BLS report on deck, we could be looking at a genuine market-mover.

Another major development: the Fed has shifted back toward quantitative easing (QE), adding an estimated $40 billion in Treasury bills per month to its balance sheet.

The last time we saw this level of balance-sheet expansion was during the 2008 global financial crisis and again during the 2020 pandemic response both moments of significant economic recalibration.

2026 is shaping up to be a noticeably more dovish year as several of the Fed’s more hawkish voices rotate out. The current voting members, Powell, Goolsbee, Schmid, Musalem, and Collins will be replaced as part of the routine rotation of regional Fed Presidents.

With a new Fed Chair stepping in for Powell, the committee’s tone is expected to shift. A fresh leadership approach combined with a more dovish voting slate means the Fed may be more open to additional rate cuts in 2026, especially if inflation continues to cool and labor market data softens.

Time to take advantage of the lower rates http://www.YourApplicationOnline.com