-

Yesterday, All my Troubles seemed so Far away….

What looked like a potential off-ramp in the Iran conflict is starting to feel like a much longer road and markets are reacting accordingly.

As uncertainty drags on, oil prices remain elevated, keeping inflation pressures alive, which in turn pushes bond yields and mortgage rates higher or prevents them from improving meaningfully.

Until we see a clear resolution or sustained de-escalation, mortgage rates are likely to remain volatile because right now, the market’s “fuel tank” is being driven by uncertainty.

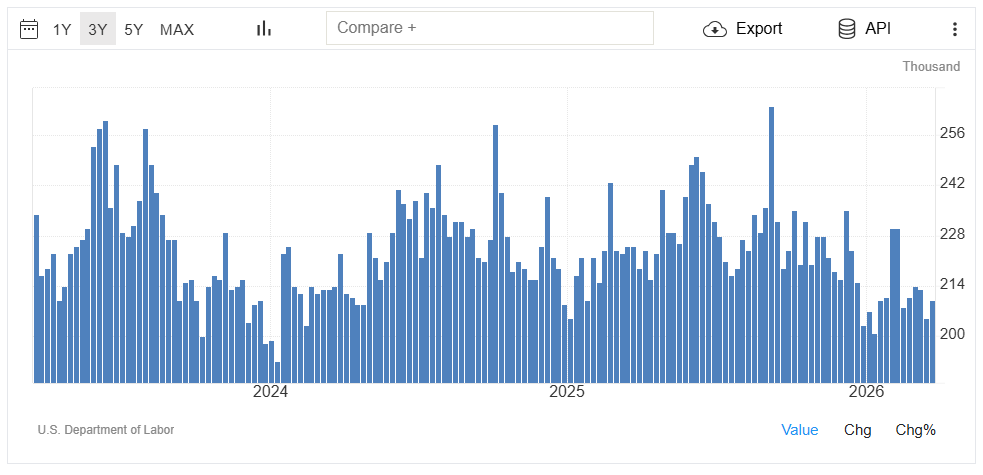

Initial Jobless Claims rose for the first time by 5,000 to 210,000, still a low level, but worth watching as a potential early indicator of softening.

Continuing Claims fell by 32,000 to 1.82M. That decline could reflect people cycling off benefits, either because they’ve exhausted eligibility or are transitioning out of the system.

The key takeaway: while headline numbers remain relatively stable, the underlying trends suggest a labor market that may be starting to lose a bit of momentum.

There is an opportunity to buy and sell. less competition if played correctly can have huge advantages long term.

Time to get pre-qualified http://www.YourApplicationOnline.com

-

Its a Rollercoaster ride in the Markets. Buckle up, it’s a bumpy ride.

Markets are always searching for stability, and over the past month, we’ve had anything but that.

Today, however, there are early signs of relief. A reported 15-point peace framework delivered via Pakistan gave markets a reason to pause, while Iran’s indication that “non-hostile” ships may pass through the Strait of Hormuz under certain conditions helped ease immediate supply fears. Reuters

The result, at least for today, is lower oil prices and improving interest rates as inflation pressures begin to soften.

That said, markets are still highly sensitive to headlines. Let’s see what tomorrow brings.

Those in the market to purchase has a distinct opportunity with higher rates comes less competition and with less competition, negotiations have more teeth.

Time to get qualified http://www.YourApplicationOnline.com

-

Structural Inflation, That’s a new one. But important.

Structural inflation is the foundation of the economy.

Picture it like a house:

- The foundation = structural inflation (stable, slow-moving, hard to change)

- A spike in oil prices = a tornado hitting the house

If the tornado is brief, maybe you lose a few shingles, short-term price pressure, but no real damage.

If it lingers, it might break a window, letting inflation start to seep into transportation, goods, and services.

If it sticks around even longer, now you’re talking about roof damage, broader inflation where higher energy costs spread across the entire economy.

Right now, the house is still standing strong. The foundation is solid, and while oil prices have picked up, that pressure hasn’t fully bled into the broader cost of goods and services.

The key question:

Does the storm pass… or does it stick around long enough to cause real damage?Lets get you pre-qualified http://www.YourApplicationOnline.com

-

ECB Signals Rate hike. US Fed holding for now. TGIF

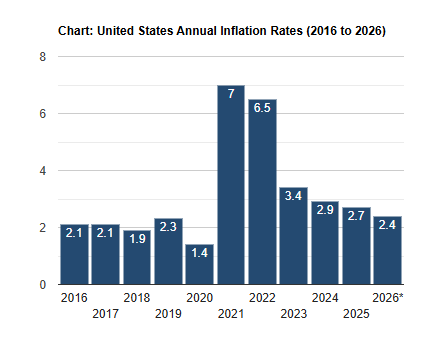

The ongoing conflict, and the resulting spike in oil prices, is fueling inflation fears and could have broader consequences beyond just the gas pump. With prices up roughly $0.90 over the past month, higher energy costs are likely to bleed into the broader economy, driving up the cost of goods and services across the board.

European Central Bank – ECB and Bank of England indicated they are ready to hike rates. The Feds are less anxious and may drop rates later this year.

On the labor market, zero job growth can be considered roughly breakeven, meaning it may not push the unemployment rate higher. That said, it all hinges on the upcoming March jobs report.

I’ll keep you posted as the data comes in.

I’m advising my purchasing clients to stay active, continue looking and submitting offers. While there’s understandable hesitation around higher interest rates, that same uncertainty is creating opportunity. Less competition, more negotiating power, and better positioning for those willing to step in while others sit on the sidelines.

Let’s get you pre-qualified http://www.YourApplicationOnline.com

-

Powell Whistling past the graveyard on jobs reports.

One of the biggest challenges with the Federal Reserve is their tendency to emphasize that “we don’t react to just one month of data”, which is fair, but it can sometimes overlook the broader trend over the past 12 months.

A good example was yesterday when Jerome Powell addressed the 92,000 job losses and reiterated that the Fed doesn’t focus on a single report. However, when you zoom out, most of 2025 has shown minimal job growth, suggesting a more persistent slowdown.

We’re seeing a similar dynamic in housing. New Home Sales, which measure signed contracts, fell 18% in January. While that sounds significant, it comes after a strong 17% gain in October and November, reinforcing that over time, activity has remained relatively consistent despite short-term swings.

On the labor side, Initial Jobless Claims dropped by 8,000 to 205,000, which appears encouraging on the surface. But Continuing Claims, a better measure of ongoing unemployment, rose by 10,000 to 1.86 million, pointing to a labor market that may be gradually losing momentum.

The takeaway: while single data points can be noisy, the trend beneath the surface is what really matters, and right now, it’s showing signs of a slower, more uneven economy.

Time to get pre-qualified http://www.YourApplicationOnline.com

-

Labor Market, BLS Jobs Report PCE Headline Inflation. and Iran.

Let’s pull the Band-Aid off and get straight to it.

We have a problem, so what’s the solution?

The Federal Reserve wraps up its two-day meeting this afternoon, and they’re walking a tightrope.

On one side, the Bureau of Labor Statistics reported 92,000 job losses in February, signaling potential weakness in the labor market. On the other, Producer Price Index (PPI) inflation jumped 0.7%, more than double expectations, pushing year-over-year inflation from 2.9% to 3.4%.

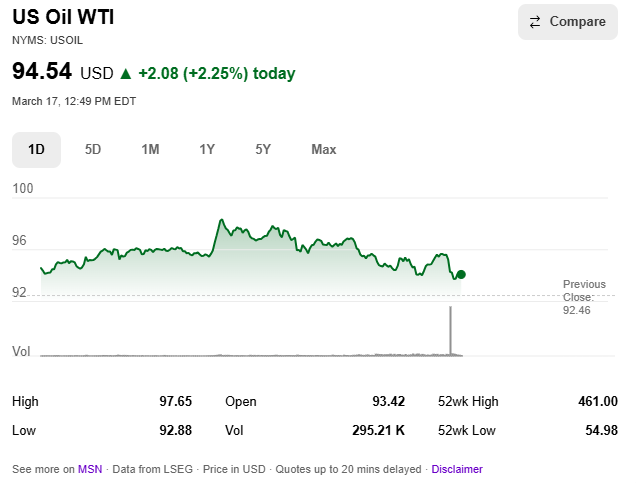

And then there’s the wildcard, geopolitics. The conflict involving Iran has helped keep oil prices elevated above $94 per barrel, adding more fuel to the inflation narrative.

So here’s the dilemma:

- Weakening jobs data argues for easing policy

- Rising inflation argues for staying tight

- Higher oil prices complicate everything

The Fed’s likely path? Hold steady and stay cautious. They can’t afford to cut with inflation reaccelerating, but they also can’t ignore cracks forming in the labor market.

Bottom line: this isn’t a moment for bold moves, it’s a moment for patience, messaging, and watching the next set of data very closely.

While we wait, let’s get you pre-qualified and ready for your new or next home. Rates will drop again with refinancing on the horizon.

http://www.YourApplicationOnline.com

-

Bonds Bounce Back, Painting It Green.

We’re on a bit of a streak, three days in a row with bonds improving, a welcome tailwind for mortgage rates.

Pending Home Sales rose 1.8% in February, a strong rebound compared to expectations for a decline. However, that data reflects a very specific moment in time, when mortgage rates briefly dipped below 6% before the recent volatility tied to geopolitical tensions.

It’s a great reminder of how impactful even a small drop in rates can be. That short window of improved affordability was enough to quickly pull buyers back into the market.

But timing matters, this is backward-looking data. The bigger question is how the recent rise in rates and global uncertainty will shape demand as we move into the spring market.

Let’s get you Pre-Qualified today so we are ready for the rate drop http://www.YourApplicationOnline.com

-

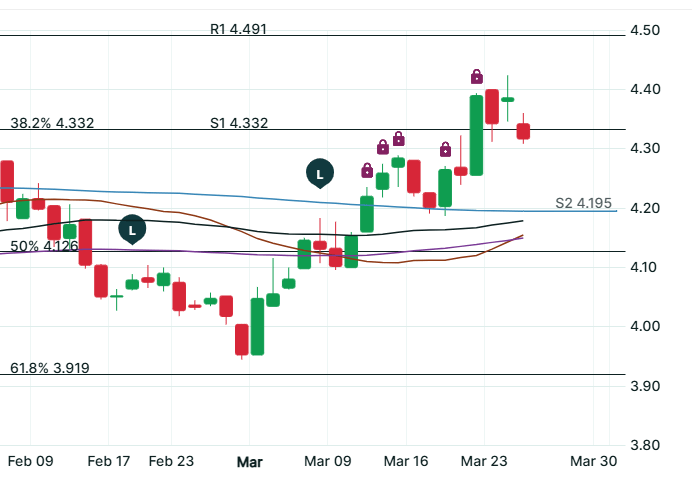

Oil down-Rates down

I could say a lot of words, but I’ll cut to the chase, Oil is below $100, bond yields dropped, and mortgage rates complied.

Will the Feds drop interest rates? most likely not until Oil prices go back to where they were below $60 a Barrell.

Rates nationally are 6.41% from the 5.99% two weeks ago but we are seeing movement in the right direction.

Have a fantastic day and week.

http://www.YourApplicationOnline.com

Below image down is higher rates. Today rates improved just a bit.

-

GDP Weak, Russian oils sanctions lifted. Oil prices still the issue.

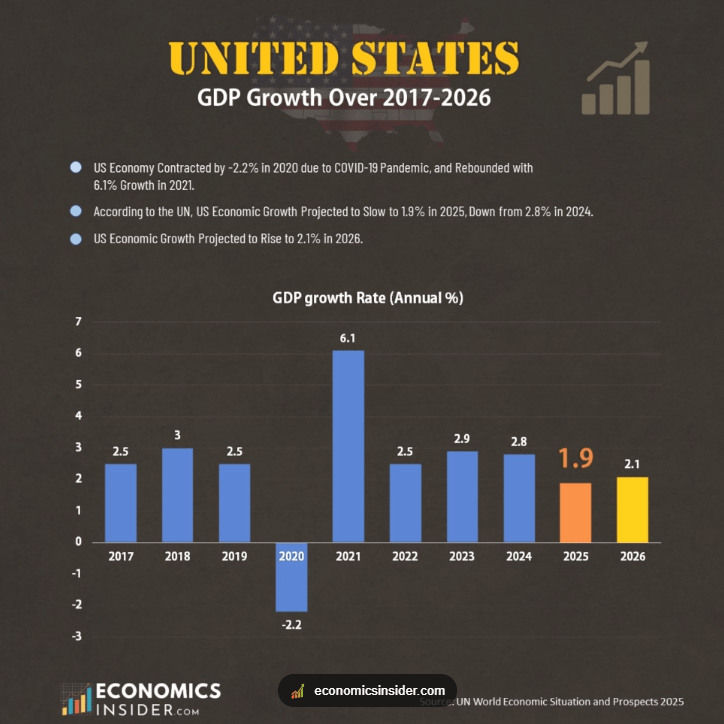

GDP for Q4 came in at 0.7% growth, a notable slowdown and roughly half of the initial estimate. The revision highlights that economic momentum late in the year was much softer than originally believed and came in well below market expectations. Slower growth at the end of the quarter suggests that consumers and businesses were already beginning to show signs of caution.

At the same time, Personal Consumption Expenditures (PCE)—the inflation measure closely watched by the Federal Reserve—came in right in line with expectations, offering little surprise to markets. Stable PCE data indicates inflation pressures are not accelerating, but they also are not easing dramatically enough to force immediate policy changes.

The challenge with economic data like this is timing. These numbers reflect what already happened in the fourth quarter, meaning we are essentially looking through the rear-view mirror. Since then, markets have been dealing with new geopolitical tensions and volatility in energy and bond markets, which could alter the economic trajectory moving forward.

In other words, the data tells us where the economy was, not necessarily where it is going. The real question now is how the latest global uncertainty and market reactions will influence growth, inflation, and ultimately interest rate policy in the months ahead.

website http://www.YourApplicationOnline.com

-

Optimism of a short War is fading causing Inflation fears.

Markets don’t always react to what is actually happening, but rather to what investors perceive is happening, or what they believe might happen next.

That’s the challenge. Oil reserves are being released, over 400 million barrels, to help stabilize supply and calm markets. However, replenishing those reserves takes significant time, making the release more of a temporary band-aid than a long-term solution.

Why is a mortgage professional talking about oil and global tensions? Because oil touches nearly every part of the economy, from heating homes to powering manufacturing and moving goods around the world.

When energy prices rise or supply is threatened, it pushes inflation higher, affects financial markets, and ultimately influences interest rates and mortgage pricing.

PCE report on inflation due out tomorrow but may have little effect even if inflation is lower for January.

This too shall pass just not sure when.

Website Nation Wide http://www.YourApplicationOnline.com

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.