-

SPF 100 Required: Lower Rates Ahead & Appreciation Heating up.

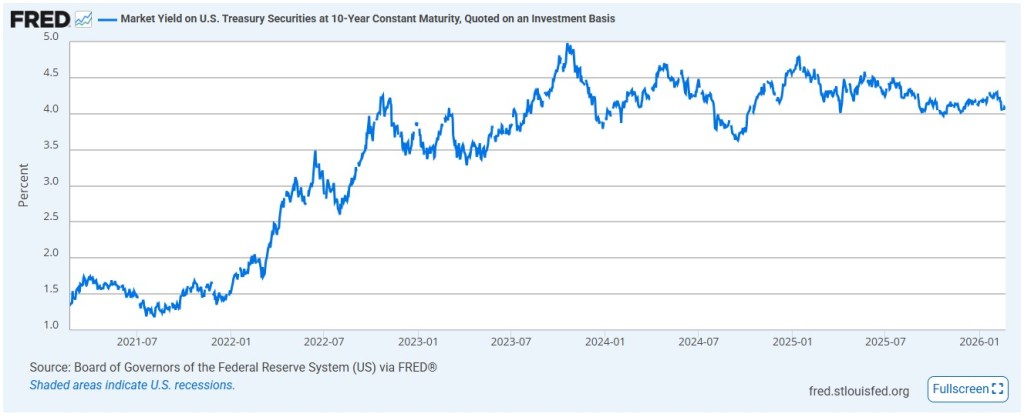

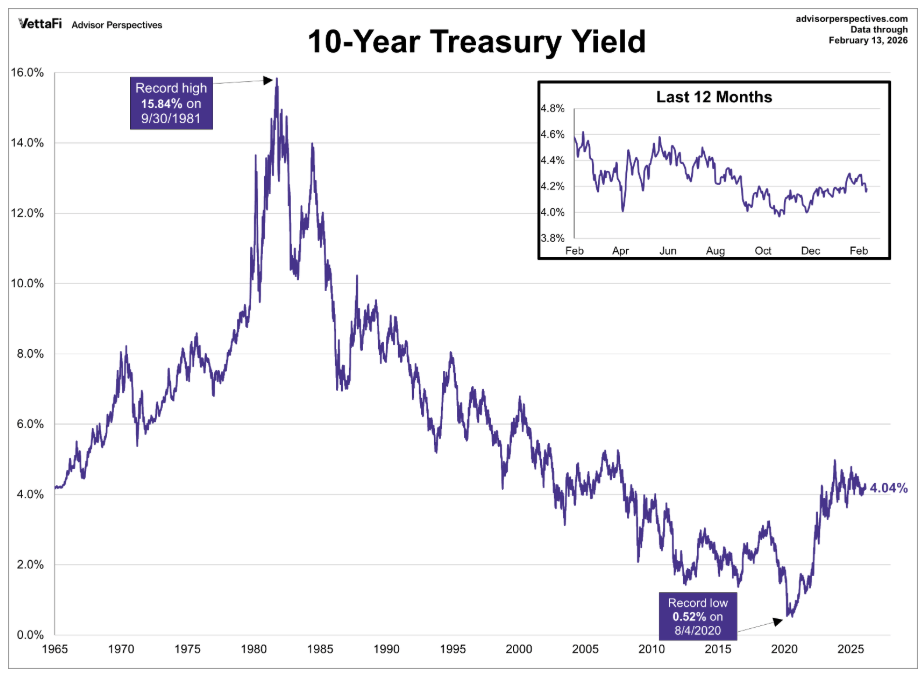

The market tried to stretch its legs today, small rebound, while bonds are down there tapping on the 4.00% yield floor like,

“Hello? Is this thing load-bearing or can we break through?”

If that floor cracks, rates could take an important step lower. And not a baby step. A real one.

Meanwhile, the appreciation reports came in and basically said,

“Yep… still going up.”Both S&P CoreLogic Case-Shiller Index and Federal Housing Finance Agency showed seasonally adjusted home prices rising 0.4%.

Translation:

Rates dipped → buyers woke up → demand showed up → prices said “thank you very much.”And now… let’s address the elephant.

Rates are the only thing that will eventually pry the 3% crowd out of their homes. You Know the Group. the 3-percenters.

They speak of their rate the way grandparents talk about buying gas for $0.89.

Some are frozen by fear.

Others wear it like a badge of honor.“Back in my day, we locked at 2.875%…”

But here’s the reality:

As rates ease, life events start outweighing nostalgia.Jobs change. Families grow. Downsizing happens. Opportunities knock.

And when that 4.00% yield floor finally gives way, the conversation shifts from: I’m never moving, to Okay…run the numbers.

Time to get pre-qualified http://www.YourApplicationOnline.com

-

The Phycological 4.0% Bond Yield Floor is going to break. Rates are starting to make their move.

The recent decision by the Supreme Court of the United States to halt tariffs could have meaningful long-term implications for inflation and rates.

Most financial analysts and economic data indicate that U.S. consumers have borne the majority of tariff costs through higher prices on imported goods. When tariffs are imposed, those added costs are often passed directly to businesses and ultimately to households.

If those tariffs are reduced or removed, it eases input costs across supply chains, from raw materials to finished goods. That creates downward pressure on prices, particularly in consumer goods categories that were heavily exposed to trade restrictions.

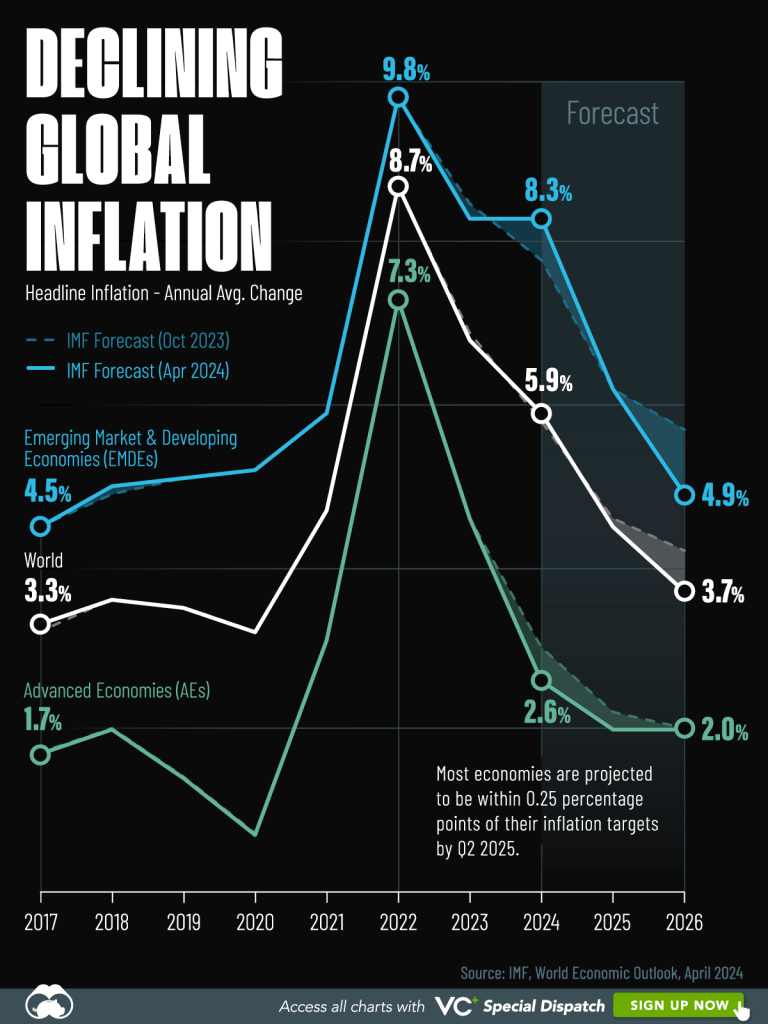

With inflation currently around 3%, the removal or softening of tariff-related price pressures gives inflation a clearer path toward the Federal Reserve’s target of 2%. While tariffs are not the sole driver of inflation, reducing structural cost burdens within the economy meaningfully improves the probability of achieving price stability without additional tightening.

In short: fewer tariffs = lower embedded costs = improved odds of returning to the “golden” 2% inflation target and Rates dropping.

Let’s get you pre-approved today. http://www.YourApplicationOnline.com

-

I say Potato you say Patato. Fed Meeting Notes show sharp division.

Yesterday afternoon we got the January 28th Fed meeting minutes, and the split could not be more obvious.

Some Fed members are basically saying, “Everything looks fine. Let’s pause. Maybe even hike again if inflation doesn’t cooperate.”

Fine? Based on what data? It feels disconnected from what’s actually happening on the ground.

Other Fed members see what the numbers are clearly showing:

- The labor market is weakening, especially once you factor in downward revisions.

- Deregulation is picking up momentum.

- Tariff pressures are easing.

- Housing is actively disinflating.

That’s two very different readings of the same economy.

One side sees lingering inflation risk.

The other sees slowing growth and cooling price pressures.This isn’t a minor difference in tone, it’s a fundamental disagreement about where the economy really stands.

And markets are paying attention.

My opinion? reality is going to hit and hit hard in the coming months. Rates will drop and we hope significantly by summer. The emperor is not wearing cloths.

Lets get you pre-qualified today http://www.YourApplicationOnline.com

-

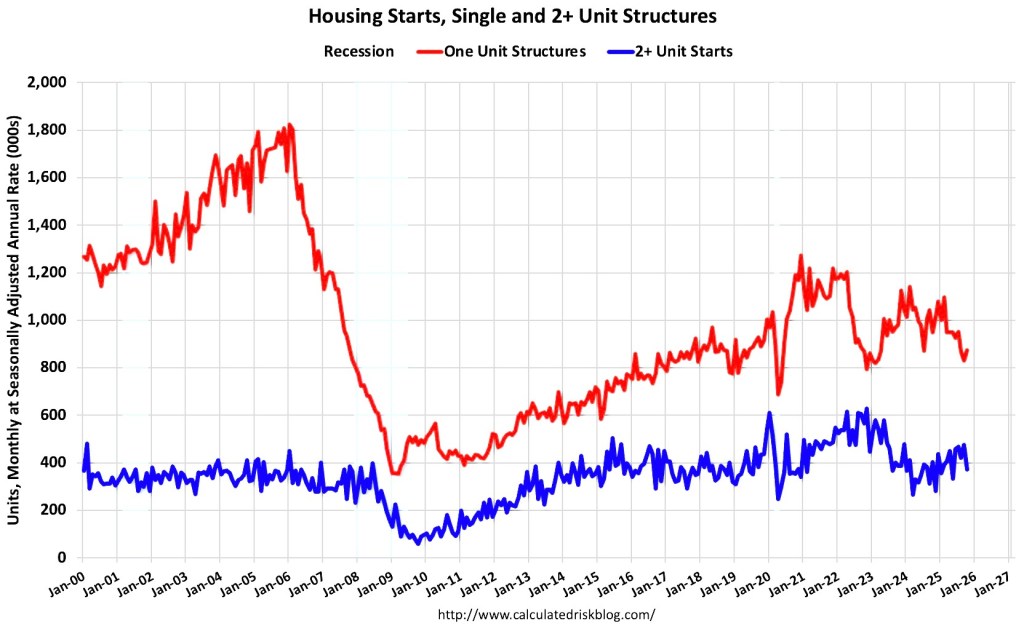

Is the Juice worth the Squeeze

Housing permits, housing starts, and housing completions are all moving higher. While they’re still below last year’s levels, the trend is clearly improving.

Helped in part by lower interest rates bringing builders and buyers back into the game.

There are still plenty of buyers and sellers sitting on the sidelines. Some are waiting for rates to drop further. Others are hoping for more inventory. And many just want a little more stability in the job market before making a move.

It’s understandable, real estate decisions aren’t small ones.

But here’s the bigger picture: real estate has always been a long-term play. Markets move in cycles. Rates rise and fall. Inventory tightens and expands.

Yet over time, home values have consistently proven to be one of the strongest and most stable wealth-building tools available.

Timing the perfect rate is difficult. Building equity over time is predictable.

The market may not feel perfect, but it rarely is. The key isn’t waiting for ideal conditions. It’s understanding your options and positioning yourself when opportunity knocks.

And right now? The early signs of recovery are starting to show.

http://www.YourApplicationOnline.com Let’s get you pre-qualified.

-

4% Bond Yield in Sight. Can it break through and What is a Floor, What is a celling?

If the 10y Bond drops below the 4% floor, look-out, rates are headed lower . We are almost there.

Think of the bond market like a house with very opinionated architecture.

The floor is that stubborn support level where yields drop(lower rates), knock politely, and the market says, “Nope. That’s cheap enough.” Buyers rush in Rates drop. The floor did its job.

The ceiling is the opposite. Yields climb higher (rates go up), peek their head up, and investors say, “Absolutely not. That’s too much.” Money pours into bonds, prices rise, yields fall, and rates back off. Ceiling holds.

Sometimes bonds pace between the floor and ceiling like a kid stuck inside on a rainy day, restless but contained. Other times they break through like the Kool-Aid Man yelling, “Oh yeah!” and suddenly we’re repricing before lunch.

We are dancing on the floor and it’s going to break through driving rates down.

http://www.YourApplicationOnline.com

-

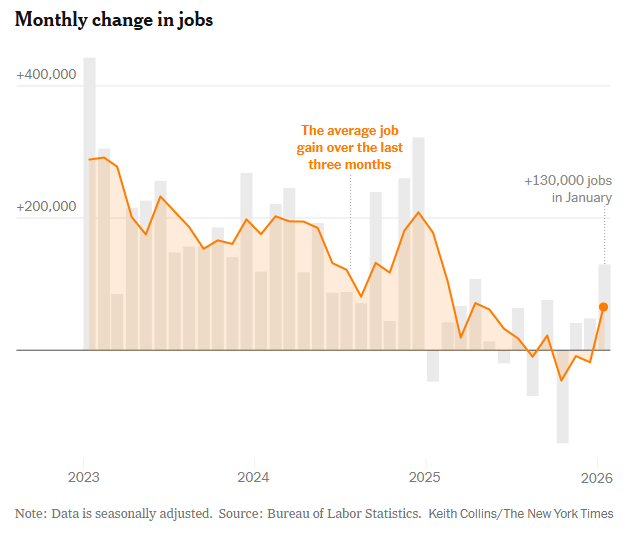

Hum Not sure about that BLS Jobs report. Market thinks something fishy is going on and pulled back.

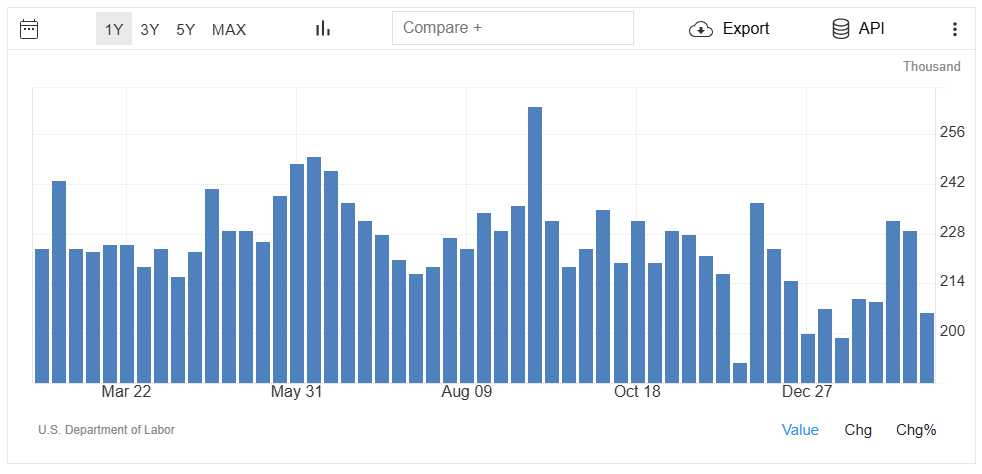

The Bureau of Labor Statistics (BLS) reported 130,000 jobs created in January.

But let’s pause for a moment.

The prior two months were both revised lower in November down to 41,000 and December down to 48,000. A combined 17,000 jobs quietly erased from the prior trend.

January is also a month that deserves context. Historically, it reflects post-holiday seasonal adjustments, retail layoffs, and annual benchmark revisions. The headline number rarely tells the full story without understanding how the seasonal factors are applied.

What stands out is the divergence between reports. ADP showed just 22,000 private-sector jobs added, while Revelio data reflected a decline of 13,300 jobs. That’s a meaningful gap compared to the BLS headline figure.

When alternative datasets are signaling softer private-sector momentum, and prior months are being revised lower, it suggests the labor market may be cooling more than the surface number implies.

The bigger question isn’t whether 130,000 is “good” or “bad.” It’s whether the underlying trend is slowing, and whether policymakers are looking at forward indicators or relying on backward revisions.

As always, the headline grabs attention. The revisions and cross-currents tell the real story.

Rates initially took a hit this morning but cooler heads prevailed and we are almost back to our improved pricing yesterday.

Let’s get you pre-qualified http://www.YourApplicationOnline.com

-

Critical week. Inflation forecast higher, Employment rate higher. Is A.I to blame?

The Federal Reserve’s mandate is to maintain price stability, with a long-term inflation target of 2%, while also supporting maximum employment. To do this, the Fed adjusts monetary policy to either slow an overheating economy or stimulate one that’s losing momentum.

Today, the economy remains relatively robust by historical standards, but unemployment is beginning to move in the wrong direction. That puts the Fed in a difficult position: growth is holding up, yet cracks are forming beneath the surface of the labor market.

This is increasingly uncharted territory, and artificial intelligence may be playing a meaningful role. The productivity gains from AI are real, but they come with side effects. Efficiency improvements are already reducing the need for certain middle-management roles, administrative positions, ad agency functions, and segments of the labor force.

In the near term, that means higher productivity without higher wages—an environment that can cool inflation without traditional economic overheating. The challenge for policymakers is that these shifts don’t show up cleanly in backward-looking data. Job losses driven by efficiency look different than those caused by recessions.

In short, the Fed is navigating an economy that appears strong on the surface, while structural changes especially AI-driven efficiency, are quietly reshaping employment and inflation dynamics. This makes policy decisions more complex and increases the risk of reacting too late to trends that are already in motion.

Let’s get you Pre-Qualified http://www.YourApplicationOnline.com

-

Housing Wealth increase 78 of the last 83 years. Bitcoin effect Classic risk-off behavior

According to a recent National Association of Realtors article, the net worth of homeowners has increased by roughly $150,000 over the past five years, largely driven by price appreciation and principal paydown. That’s a meaningful wealth effect that continues to support housing demand.

On the supply side, Realtor.com reports listings were down 7% in January, yet still up 10% year over year. In other words, inventory is improving, but it remains tight enough to keep pricing supported hardly the setup for a housing collapse.

And then there’s crypto. Bitcoin fell nearly 50% from its October all-time high above $120,000, and a big driver has been a shift in liquidity toward precious metals. As tech particularly software has struggled, risk appetite has faded. Investors, especially retail money, did what it always does in moments of uncertainty: panic first, rotate later, moving capital into gold and silver as perceived safe havens.

Classic risk-off behavior. Different asset, same psychology.

Time to get pre-qualified soft credit pull http://www.YourApplicationOnline.com

-

JOLTS Job Report was a Jolt. seriously. Rates improve New Fed Chair wants to cut now.

The JOLTS job report for December came in with 6.5 million job openings, well below the 7.2 million expected and officially the lowest level since 2020. Oof.

November didn’t escape either, getting revised down from 7.15M to 6.93M. So yes, the labor market is quietly taking its foot off the gas while pretending everything is fine.

Now layer in the AI boom. Counterintuitive take: AI won’t stoke inflation—it does the opposite.

Why? Productivity goes up, but jobs go down. Fewer jobs = less consumer spending. Less spending = retailers sharpening their pencils and cutting prices just to move inventory. Congrats, that’s disinflation with a Silicon Valley accent.And this is exactly why Kevin Warsh (or at least the future-looking Fed crowd) keeps nudging toward rate cuts. He’s not staring at last quarter’s data like it’s a backup camera, he’s looking through the front windshield at where the economy is actually headed.

Rear-view Fed vs. windshield Fed.

One taps the brakes late. The other sees the curve coming.Let’s get you pre-approved and ready to buy or refinance. http://www.YourApplicationOnline.com

-

Jobs Report: Not Great, Not Terrible (But Rate-Friendly)

ADP released weaker-than-expected jobs data today, and for once, “bad news” was good news for bonds. Bonds caught a bid, which helped nudge mortgage rates slightly lower. No victory parade, but we’ll take the win.

Digging into the details (because the headline never tells the full story):

- Small businesses: created exactly zero jobs. Not negative… just aggressively neutral.

- Large businesses: shed about 18,000 jobs, which lines up with the layoffs we’ve been hearing about from companies like Amazon, UPS, and others.

- Medium-sized businesses: the overachievers of the group, adding roughly 41,000 jobs and doing all the heavy lifting.

So while the job market isn’t falling off a cliff, it’s clearly losing momentum. And that’s important.

A cooling economy and a softer labor market are exactly the signals the Fed watches for when deciding whether it’s time to lower rates, especially if inflation continues trending down as expected.

Bottom line:

Strong jobs push rates up.

Weak jobs pull rates down.

Today leaned more toward “rate-friendly slowdown” than “red-hot economy.”And once again, what looks like bad news at first glance ends up being pretty decent news if you’re watching mortgage rates.

Let’s get you pre-approved http://www.YourApplicationOnline.com

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.