-

The Balancing act of negotiating Disappointment and Softer GDP and PCE.

Bear with me for a moment:

With every good comes some bad. With every high, a low. We only recognize light because we have seen darkness, and we only appreciate the climb because we have felt the fall. One gives meaning to the other.

Stocks are lower this morning, oil prices are ticking a bit higher, but Mortgage Bonds are slightly positive after softer-than-expected economic data helped stabilize the bond market.

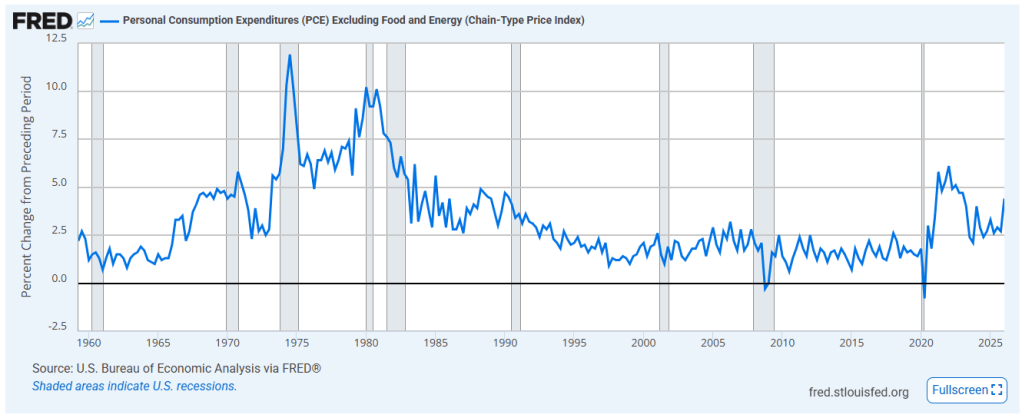

On the heels of more disappointment surrounding the Iran/U.S. peace discussions, markets were looking for something positive, and they found it in weaker GDP growth figures and cooler monthly PCE inflation readings.

That combination helped offset some of the pressure coming from rising oil prices and ongoing geopolitical uncertainty.

The market is essentially stuck between two competing forces right now:

- Higher oil prices and global tension pushing inflation fears higher

- Slower economic growth and softer inflation data helping bonds recover

For mortgage rates, that means continued volatility. One headline can move the market quickly in either direction.

Bottom line: the bond market is still searching for stability while trying to determine whether inflation or slowing growth becomes the bigger story moving forward.

http://www.YourApplicationOnline.com

-

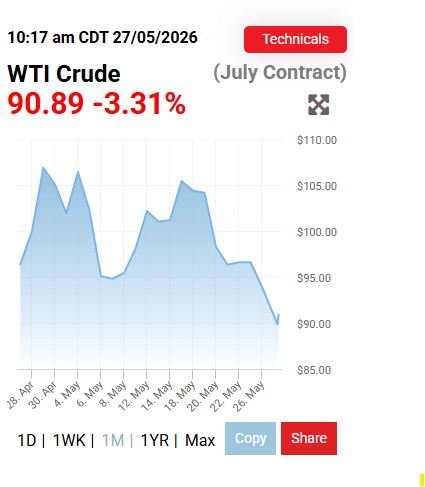

Under $90/barrel Yeah. Funny how quickly market and expectations adjust.

Two months ago, if someone said oil would be sitting just under $90 a barrel, the reaction would have been a collective gasp of dread.

Funny how quickly things change.

Now the market is practically celebrating oil at $90 a barrel.

Bottom line, the market wants stability. Even a small hint that the Strait could reopen within the next 30 days is enough to give investors some optimism. Let’s cross our fingers and hope cooler heads prevail.

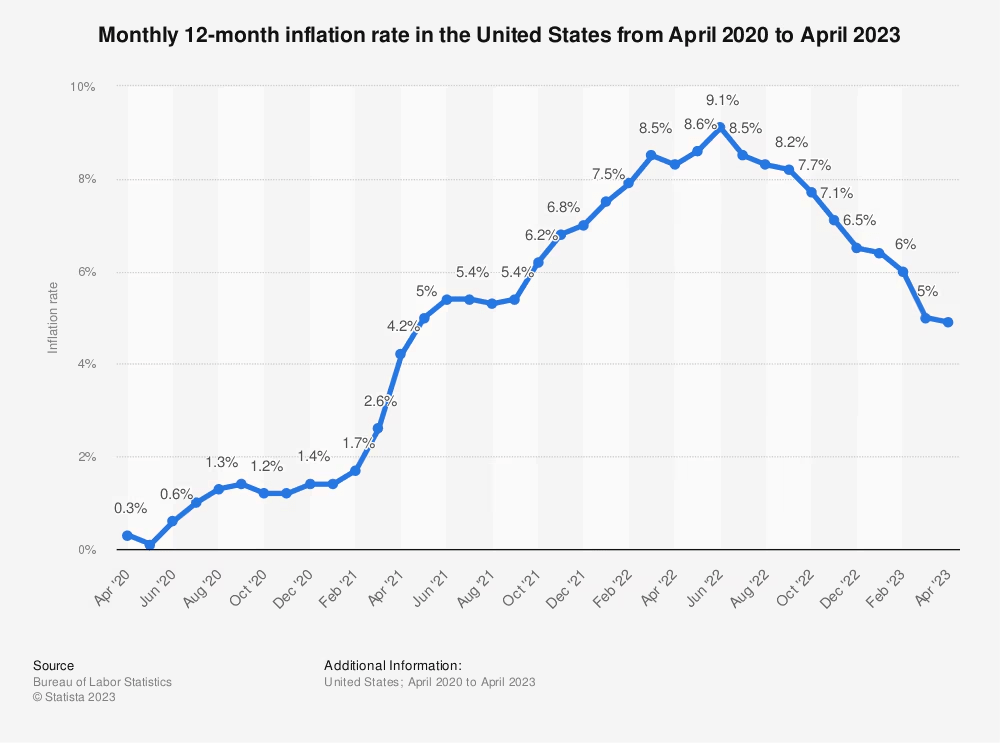

In other news, the upcoming Personal Consumption Expenditures (PCE) inflation report is expected to show headline inflation rising from 3.5% to 3.8% year over year. Under normal circumstances, that would likely pressure both bonds and mortgage rates higher.

But right now, geopolitics and oil are driving the bus. As long as there are no major negative developments surrounding the U.S./Iran peace talks, the market may be willing to look past a hotter inflation reading, at least temporarily.

http://www.YourApplicationOnline.com

-

Peace? Uncertainty and some Optimism helps Bond Markets Globally

Oil prices and Treasury yields are lower this morning as optimism builds around a potential U.S./Iran peace deal.

At this point, markets are grasping not at straws, but at any dangling rope or piece of twine that appears. The world collectively wants this conflict to end preferably yesterday.

For now, markets are reacting positively to even the possibility of progress, though investors remain cautious after several false starts and headline reversals along the way.

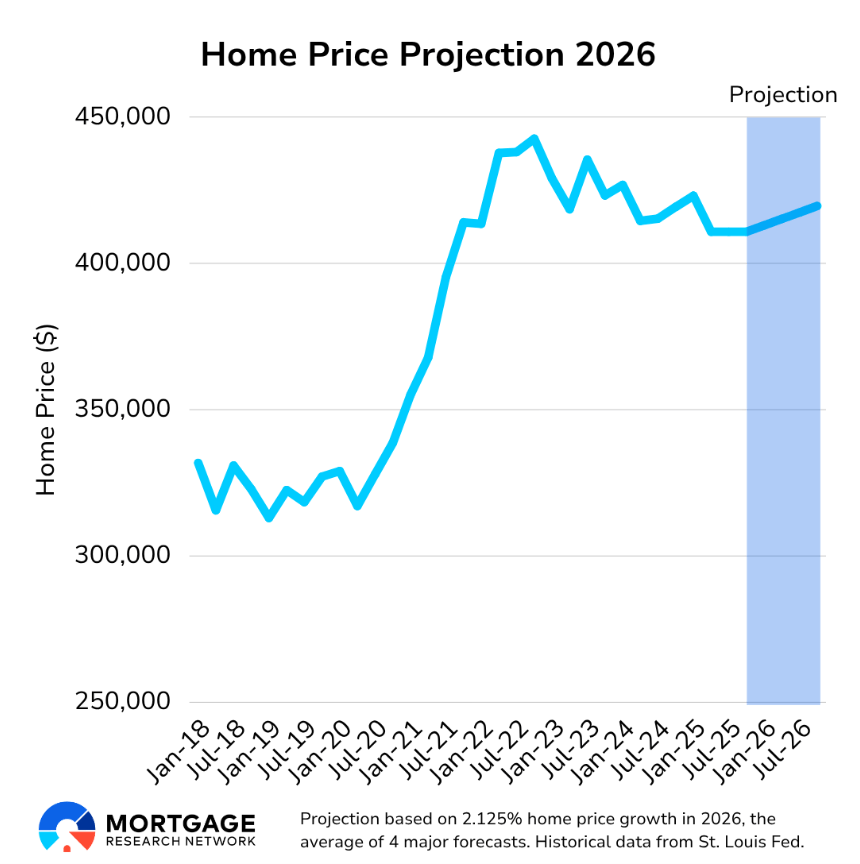

Housing Appreciation Data showed decent gains in March, but digging deeper into the numbers reveals a relatively flat overall reading beneath the surface.

That is not entirely unexpected given the current housing market, higher rate environment, affordability pressures, and broader global uncertainty. On paper the market still appears stable, but momentum has clearly slowed compared to prior years.

Time to get pre-qualified, Soft credit pull.

http://www.YourApplicationOnline.com

-

Pressure Building on both sides and Memorial Day Ultimate sacrifice for our freedom.

There is significant pressure building between Iran and the U.S. At this point, nobody truly wins in these situations, and over time we all end up paying the price one way or another, whether through higher oil prices, inflation, market volatility, or broader economic uncertainty.

The bond market and oil prices continue to modestly improve. We’ll take that for now, but markets would likely improve more substantially once an official compromise is reached.

That said, we’ve seen plenty of head fakes over the last few months, so there’s still skepticism around whether anything permanent ultimately materializes. For now, there are ongoing discussions surrounding a potential interim deal, and markets appear cautiously optimistic.

This Memorial Day, we remember and honor the brave men and women who made the ultimate sacrifice for our freedom. Grateful today and every day for those who served and gave everything for this country.

http://www.YourApplicationOnline.com

-

Deal, No-Deal, Deal, No-Deal. Peace deal fades as Oil prices rise.

Oil prices and bond yields are moving higher again this morning as optimism surrounding a potential Iran-U.S. peace deal continues to fade. Markets are reacting to uncertainty, and uncertainty is rarely friendly to interest rates.

The Fed hawks are also back in the conversation, with growing speculation that another rate hike could still be on the table as inflation remains stubbornly above 3%. New Fed President Kevin Warsh added fuel to that discussion as markets continue trying to price in the next move.

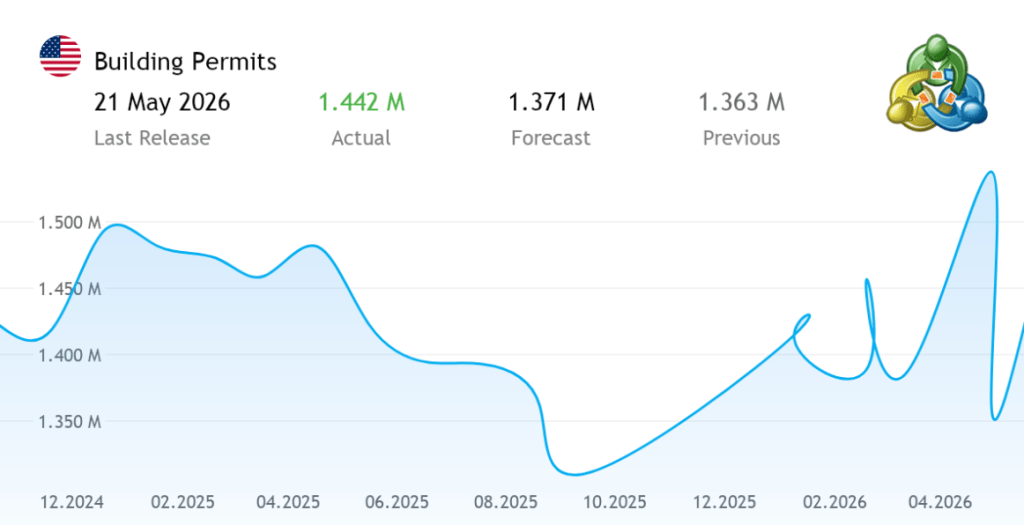

On the other side of the economy, housing data came in stronger than expected. Housing permits rose 5.8% in April while housing starts slipped only slightly. Both reports beat expectations and continue to reinforce the point that, regardless of rates, life keeps moving forward.

People still relocate, families grow, jobs change, and homes continue to be bought and sold.

Another interesting piece of the inflation story: rent growth remains relatively tame, rising only 1.3% year over year. That’s a meaningful slowdown compared to the sharp rental increases we saw over the last few years.

So where do we go from here?

We do what markets, homeowners, and buyers always do; we adjust, adapt, and plow forward to live another day.

http://www.YourApplicationOnline.com

-

Home Sales Up 1.4% despite higher rates. Life moves on regardless.

Pending Home Sales, which measure signed contracts on existing homes, rose 1.4% in April despite higher interest rates. March was also revised higher to 1.7%.

So what’s going on?

First, real estate data is often measured against the previous 12-month period. If last year’s numbers were weak, even modest improvement can show as growth.

But more importantly, life keeps moving forward regardless of headlines or mortgage rates.

People don’t just buy and sell homes because rates are low. Life events drive housing decisions far more than the daily market cycle. Divorce, death, marriage, growing families, job relocations, retirement, downsizing, those realities continue no matter where interest rates are sitting.

That’s why housing never completely stops. Buyers and sellers will always have motivations beyond the day-to-day market noise.

The market may slow, adjust, or shift strategies, but life events continue to create demand.

Let’s get you pre-approved http://www.YourApplicationOnline.com

-

The Pressure is building, Oil prices, Stock market and Bonds. Something has to give.

Oil prices are higher this morning, with WTI trading around $109/barrel. The stock market is lower, and Mortgage Bonds are also down sharply to start the day. Meanwhile, the 10-year Treasury yield continues to push higher, now trading above 4.65%.

As a general rule of thumb, adding roughly 2% to the 10-year Treasury yield puts us close to the current national average mortgage rate environment, which is hovering around 6.75%.

The combination of higher interest rates and rising home values has continued to create a “lock-in effect” for many homeowners. In addition, outdated tax rules are not helping encourage inventory movement.

Currently, homeowners who have lived in their primary residence for 2 out of the last 5 years may qualify for a capital gains exclusion of up to $250,000 for single filers and $500,000 for married couples filing jointly.

Those exclusion limits have not been updated since 1997, despite home values increasing more than 2.5x in many markets over that same period.

There are proposals being discussed that would potentially double those exclusion limits. At present, approximately 15% of homeowners are estimated to have gains above the current thresholds, which becomes yet another reason many homeowners choose not to sell.

Not trying to be Debbie Downer here, but it’s important to take an eyes-wide-open approach.

http://www.YourApplicationOnline.com

-

Why are the Feds buying $40B worth of Bonds from Banks?

Liquidity. One word, but incredibly powerful.

When the Fed injects liquidity into the banking system, banks have more money to lend. More lending means more money flowing through the economy, which can fuel inflation. Why they are doing this, we don’t exactly know but its not necessarily normal.

But this is very different from the Quantitative Easing (QE) we saw in prior years, when the Fed was heavily buying Mortgage-Backed Securities and 10-year Treasuries. That directly helped long-term bond pricing and pushed mortgage rates lower.

Today, the biggest driver of higher rates is oil and geopolitical uncertainty. Rising energy prices ripple through everything — transportation, goods, manufacturing, consumer costs — and markets hate uncertainty.

When headlines keep repeating phrases like “the clock is ticking,” investors react defensively. Stocks get volatile, bonds sell off, and mortgage rates move higher.

Bottom line: until oil prices stabilize and hostilities ease, rates may remain elevated longer than people expect.

Waiting for the “perfect” rate environment may not be the best strategy. Negotiating the right price on the right home while competition is thinner might matter far more in the long run.

http://www.YourApplicationOnline.com

-

Global 10-year Yields multi-year highs. What’s to blame – Oil and Inflation.

Oil prices are climbing globally while bond yields surge across the UK, Japan, Germany, and here in the U.S., with the 10-year Treasury hitting its highest level since May 2025.

That’s pushing mortgage rates higher.

As a simple example, the 10-year Treasury is trading around 4.567%. Add roughly 2 points, and you get a general idea of where average mortgage rates are landing: about 6.567%.

Now think back just a few months ago. The 10-year Treasury was sitting near 3.99%, and national average mortgage rates briefly touched 5.99% for the first time in years. Amazing how quickly markets can move.

Today also marked Kevin Warsh’s official first day, and the bond market wasted no time selling off. The challenge ahead? Cutting rates becomes extremely difficult while tensions with Iran continue and oil prices remain elevated. Inflation and energy costs still have the steering wheel.

But real estate doesn’t stop. People still get married, relocate, grow families, downsize, and buy homes.

Many buyers are sitting on the sidelines waiting for the “perfect” rate.

Translation: less competition for the buyers willing to move. While others wait… you pounce.

http://www.YourApplicationOnline.com

-

More Oil says IEA-Kevin Warsh in, Powell out. Inflation Scorching hot.

The Producer Price Index for April rose 1.4%, nearly triple the 0.5% expected. Year-over-year inflation moved from 4.3% to 6%. Let that sink in… 6% inflation.

A big chunk of the increase is tied to higher oil prices and tariffs working their way through the system.

There’s also another inflation component hiding in plain sight: the Fed printing money and buying short-term Treasury Bills. More dollars chasing fewer goods. That was a major driver behind the inflation spike we saw back in 2022, and markets are paying attention to whether history starts repeating itself.

But what does this mean for interest rates?

Mortgage rates are now riding shotgun with oil prices and geopolitical tension. If oil prices cool off, inflation pressure eases, bonds stabilize, and rates have room to improve. That’s the simple version.

But if the Strait stays closed or tensions escalate, oil climbs, inflation fears grow, and mortgage rates will likely keep drifting higher.

Right now, the bond market is trading less on optimism and more on the price of a barrel of oil.

http://www.YourApplicationOnline.com

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.