-

52% of Home buyers are over 46 years old. Don’t forget about us.

An interesting nugget from the National Association of Realtors trends report:

Over 50% of home purchases are coming from buyers age 46 and up.

Most of the marketing world is out here chasing first-time buyers like it’s a Black Friday doorbuster… when the real action is happening with the “I’ve been through a few rate cycles and survived” crowd.

Makes sense though, this group typically has more equity, more savings, and a better feel for timing the market. They’re not just buying homes, they’re making strategic moves.

Moral of the story: don’t sleep on the seasoned buyers… they’ve got the experience and the down payment.

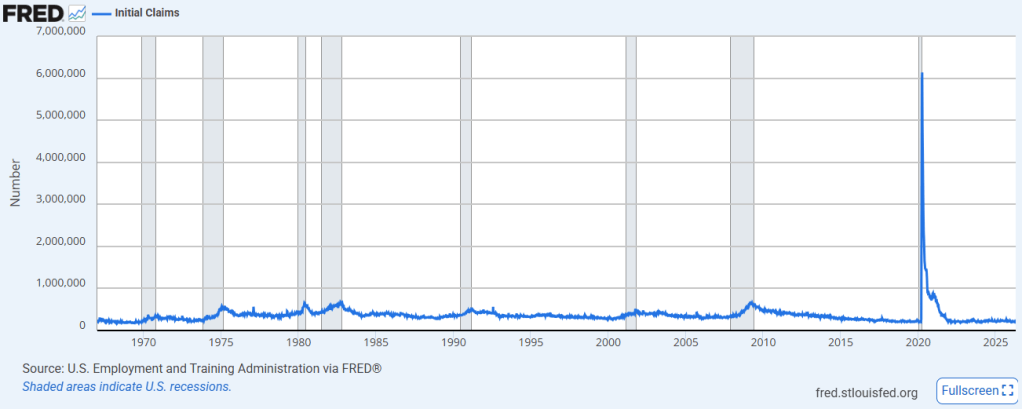

Oil prices continue to inch higher, keeping some pressure on inflation expectations. Jobless Claims and Continuing Claims both ticked up slightly, giving the bond market a reason to react, but the response has been fairly muted.

Translation for rates: a bit of push and pull. Higher oil leans rates up, softer labor data leans them down, and for now they’re mostly offsetting each other.

Let’s get you pre-approved http://www.YourApplicationOnline.com

-

Indefinite ceasefire extended. Oil lower as rates start to follow

Oil prices are moving lower this morning, stocks are pushing higher, and mortgage rates are seeing some modest improvement as markets react to a more stable tone.

On the geopolitical front, Pakistan has requested that the current ceasefire be extended indefinitely while negotiations continue. That development is helping ease some of the recent uncertainty, giving markets a bit of breathing room and supporting the slight improvement we’re seeing in rates.

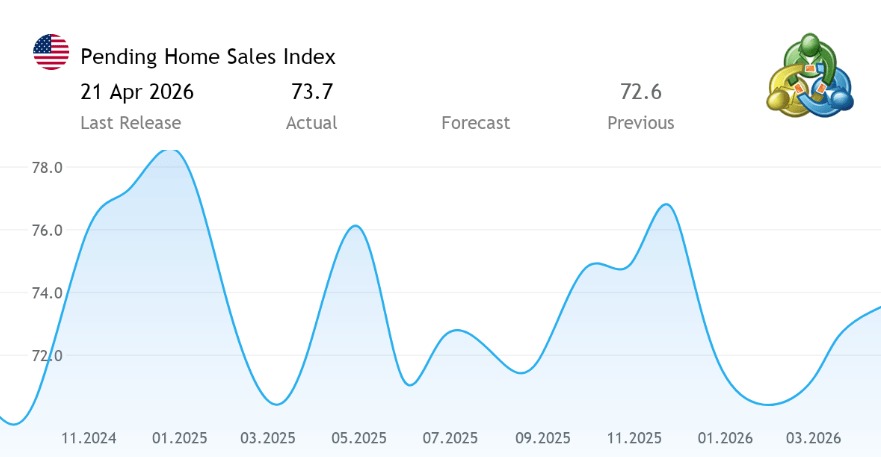

Pending Home Sales rose 1.5% in March, stronger than the expected 0.5%. This is encouraging news to see two consecutive months of higher than expected sales.

Kevin Warsh held his own at the Senate confirmation hearing for the new Fed President. Warsh sounded smart, polished and ready to lead the Fed.

Its a new day, lets get to getting.

http://www.YourApplicationOnline.com

-

Strait Opens, Oil Dropping, Bonds Rally. Please be sticky…

WTI Crude is hanging out around $85 a barrel, but for now, markets seem to be taking what they can get. Stocks are pushing higher, bonds are finding a little footing, and rates… well, they’re starting to move in the right direction.

This all comes on the heels of a 10-day ceasefire between Israel and Lebanon that kicked in last night. Anytime the headlines cool off, markets tend to exhale, and we’re seeing a bit of that relief today.

Now the big question: does this momentum stick, or was this just a quick coffee break before volatility clocks back in?

Either way, I’m officially sending positive vibes into next week’s news cycle, hoping for calmer headlines, cooler oil, and mortgage rates that continue to trend in the right direction.

http://www.YourApplicationOnline.com

-

Peace Talks? Maybe, Markets wait. Powell may stay longer.

As Mike Tyson once said, “Everyone has a plan until you get punched in the face.”

Right now, the market feels like it just took one.

Next week, we should get more clarity on the ongoing U.S., Iran peace talks. The outcome matters, because it directly impacts oil, inflation, and ultimately interest rates.

If tensions ease, we could see oil prices settle, inflation cool, and consumer confidence start to recover. Markets have already shown signs of optimism when talks progress, with equities rebounding on potential resolution headlines.

But if things drag out, the opposite happens, higher energy costs, more uncertainty, and continued pressure on rates and affordability. Businesses are already in “wait and see” mode due to rising costs tied to the conflict.

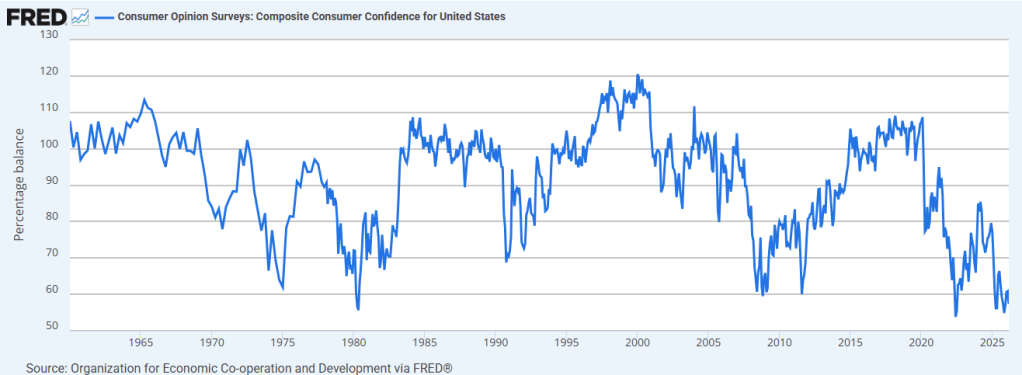

Consumer confidence is the wild card here. It has dropped sharply amid rising gas prices and economic uncertainty tied to the conflict, with sentiment hitting historically weak levels in recent readings.

And just to clarify, while it feels like a 70-year low, what we’re actually seeing is sentiment near or at record lows in the history of the survey, which goes back to the 1950s.

Bottom line:

We’re in a headline-driven market right now. Peace talks = relief. Escalation = volatility.But, the Spring activity is real. People move on, move out , move in. life continues forward and its starting to become a busy spring buying season.

http://www.YourApplicationOnline.com

-

Is it or Is it not a ceasefire? Markets are confused and nervous.

The ceasefire is already looking shaky this morning, and markets feel it.

Traders in both stocks and bonds are stuck in limbo and add in the Fed signaling potential rate hikes if inflation doesn’t come under control.

At the center of it all? Oil.

Oil prices don’t just impact what you pay at the pump, they ripple through manufacturing, transportation, and inventory costs, touching nearly every part of the economy.

When oil moves higher, inflation pressure follows.

And when inflation sticks around, rates stay higher for longer.Uncertainty fuels volatility.

Oil fuels inflation.

And right now, we’ve got both.On a side note, we’re seeing a noticeable uptick in purchase activity.

Yes, it’s spring, but this feels like more than just seasonality.

There’s a broader shift happening. People are moving, relocating, downsizing, upsizing, life events are starting to outweigh rate hesitation.

Families grow. Jobs change. Priorities shift.

And when that happens, decisions get made.http://www.YourApplicationOnline.com

-

As tensions wane demand for 10-year Bond sores as Yield pressure mounts.

When yields begin to fall, demand for higher-yielding bonds increases significantly. Investors would rather lock in stronger returns today than sit on the sidelines and risk watching yields drop further.

That shift in behavior creates increased buying pressure in the bond market, which pushes bond prices higher and yields even lower.

This dynamic directly benefits mortgage rates.

Mortgage rates are closely tied to bond yields (especially the 10-year Treasury) and are also influenced by broader inflation drivers like oil prices. As yields decline and inflation pressures ease, mortgage rates typically follow in the same direction.

In short:

Lower yields → more bond buying → lower rates.It’s a chain reaction, and when it gains momentum, rate improvements can happen quickly.

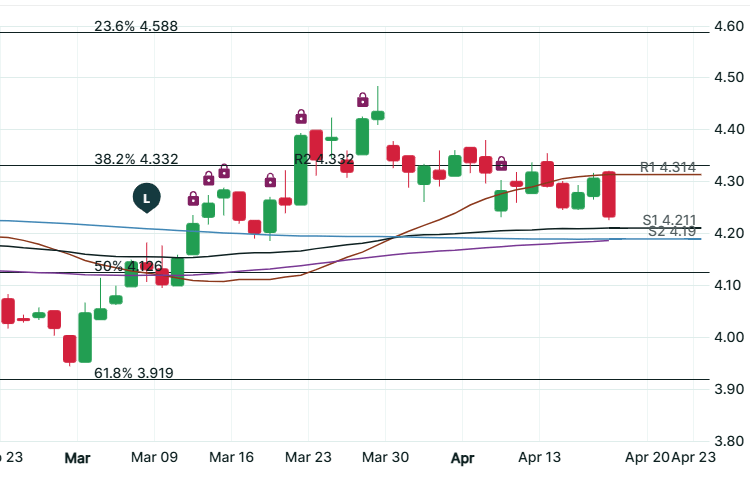

A two-week ceasefire and the reopening of the Strait of Hormuz, if it holds, should help push oil prices back toward the $65/barrel range and bring the 10-year Treasury yield below 4.00%.

That’s the key level.

If you’re considering a refinance, sub-4% on the 10-year is the “magic number” where we typically see meaningful improvement in mortgage rates.

Stability drives confidence.

Confidence drives lower rates.http://www.YourApplication online.com

-

8:00pm ET Tomorrow, the Bond Market Waits.

The last four weeks have been more than a rollercoaster they’ve been full-on whiplash.

Oil prices are closely tied to mortgage rates because of their direct and indirect impact on inflation. When energy costs rise, they ripple through transportation, manufacturing, and ultimately consumer prices keeping inflation elevated and putting upward pressure on rates.

And that’s the key point:

Inflation is the enemy of value over time.

It erodes purchasing power, drives borrowing costs higher, and makes it harder for rates to improve in a meaningful way.

Control inflation, and rates follow.

Let inflation run, and everything gets more expensive including money.Will the U.S. and Iran reach an agreement on the Strait of Hormuz before tomorrow’s deadline… or just move the goalpost again?

Given the recent pattern of extensions and shifting timelines, another deadline wouldn’t be a surprise.

That uncertainty is exactly what markets hate.

When there’s no clear path forward, fear takes over stocks get hit, bonds sell off, and rates stay elevated. Oil becomes the pressure point, and inflation concerns follow right behind it.

But here’s the flip side:

The moment clarity shows up whether it’s a deal, de-escalation, or just a defined path markets can pivot quickly.

And when uncertainty drops…

rates can drop fast. http://www.YourApplicationOnline.com

-

BLS Jobs report 178,000 Jobs Created, Really are you sure about that?

The Bureau of Labor Statistics (BLS) released the March jobs report, and collectively, the market just kind of… stared at it.

The volatility isn’t just confusing, it’s borderline nonsensical.

February’s report originally showed 82,000 jobs lost, and was then revised even lower to 133,000 jobs lost. That’s not a tweak, that’s a trend shift.

Looking at March, most of the “job gains” came from Healthcare and Social Assistance. But here’s the catch: a large portion of those were simply workers returning from strike, not new job creation.

So what are we really seeing?

The Household Survey tells a different story, showing 64,000 jobs lost in March.

Meanwhile, the unemployment rate ticked down from 4.4% to 4.3%, but not because of strong hiring, more likely due to attrition and workers leaving the labor force, not finding jobs.

In short:

The headline says one thing.

The underlying data says something very different.And that’s where the real story is.

-

Clarity, That’s all

Oil prices are sharply higher this morning, while stocks and bonds are both under pressure following last night’s address to the nation.

Markets were looking for clarity, and didn’t get it.

Instead, the takeaway appears to be prolonged conflict with no clear plan to reopen the Strait, which is pushing oil prices higher and adding to inflation concerns.

On the labor front, data was mixed:

- Jobless Claims fell by 9,000 to 202,000

- Continuing Claims rose by 25,000 to 1.84 million

Meanwhile, the Challenger Job Cuts Report showed 61,000 layoffs in March, with roughly 25% attributed to AI-related reductions, bringing the Q1 total to 217,000 cuts.

The theme is becoming clearer:

Rising energy costs + softening labor trends = a more complicated outlook for rates and the broader economy.Look at it this way, if the unemployment rate is at 4.4% and expected to go to 4.5%, that means 95.5% employment.

Get out there and lets get you approved for a mortgage. http://www.YourApplicationOnline.com

-

Consumer Sentiment Sours, Rate Hike Unlikely even with Oil rising. I will explain.

When oil prices rise and stay elevated, the impact goes far beyond the gas pump. Energy is a core input across the global economy, and work their way into manufacturing costs, transportation, shipping, and ultimately consumer goods.

At first, consumers absorb the increase. But over time, behavior changes.

People don’t just keep paying more indefinitely, they adjust. They delay purchases, trade down, or substitute entirely. That’s where demand starts to shift.

“Do you want the steak… or is chicken okay?”

Multiply that decision across millions of households, and you begin to see the broader effect. Slowing demand puts pressure on businesses, which can lead to price reductions, margin compression, and eventually disinflation or even deflation in certain sectors.

If sustained long enough, this demand slowdown can ripple through the economy, impacting growth, hiring, and ultimately increasing the risk of a broader economic slowdown or recession.

Higher prices don’t just raise inflation, they can eventually kill demand.

Bottom line is the FEDs will not be raising rates and may cut sooner than later. Its a balancing act.

http://www.YourApplicationOnline.com

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.