-

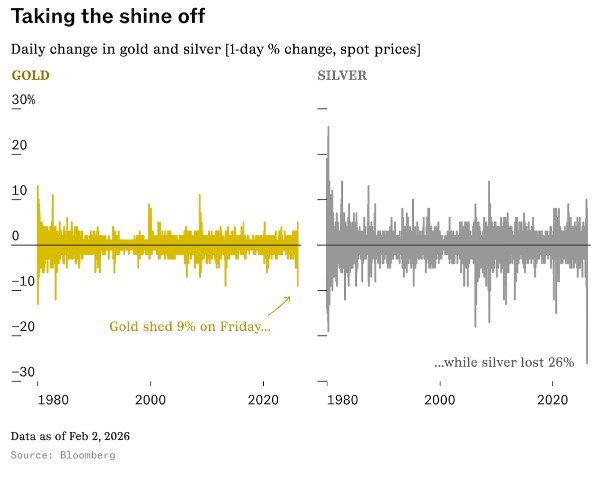

Job numbers Gold and Silver some shine is coming off.

The stock market is up, bonds are down… and mortgage rates are doing that thing where they look at good news and say, “Cool story, still not helping.” So yes, Wall Street is partying, but rates didn’t get the invite and actually lost a little ground today.

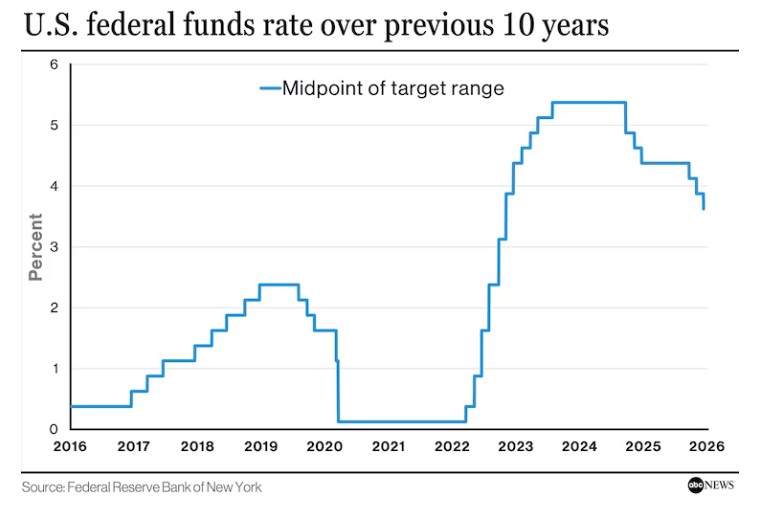

With Kevin Warsh stepping in as the new Fed Chair, the perceived separation between the Oval Office and the Federal Reserve suddenly feels very real. Markets liked that. Stocks reacted in a friendly, high-five-each-other kind of way. Bonds? Not so much. And when bonds sulk, rates follow.

Now let’s talk jobs, because this is where the magic trick happens.

Continuing unemployment claims are down, which sounds great… until you realize they stop counting you after roughly 21 to 26 weeks, depending on the state. Translation: the number can go down not because people found jobs, but because the clock ran out. That’s not job growth, that’s the data saying, “You’re no longer our problem.”

So if the job market feels strong on paper but weird in real life, that’s because both things can be true at the same time.

Bottom line:

What you think you’re seeing isn’t always what’s actually happening. Markets love headlines. Rates care about details. And right now, the details are doing all the talking.let’s get you pre-qualified http://www.YourApplicaitonOnline.com

-

New Fed Chair Kevin Warsh. Was a Dove now a bit of a Hawk. what that actually means.

In Federal Reserve policy, a hawk prioritizes fighting inflation, typically supporting higher interest rates and tighter monetary policy to keep prices stable.

A dove, on the other hand, focuses on economic growth and maximum employment, often favoring lower interest rates and a more accommodative, expansionary policy.

In short: hawks worry about inflation; doves worry about jobs.

I spent a good part of the morning watching coverage on Kevin Warsh, and the takeaway feels a bit mixed, though it’s clear he’s been openly critical of the current Fed and its approach to monetary policy.

Our view is that Warsh would be more forward-looking, with a greater willingness to look through the lagging inflation data and question potential overstatements in jobs numbers. That kind of perspective matters, especially when policy decisions are being made using data that often reflects where the economy was, not where it’s headed.

let’s get you pre-qualified http://www.YourApplicationOnline.com

-

Markets react to Potential Shut-Down. a bit of Deja Vu.

The stock and bond markets love stability. They like routine. Predictability. A nice, boring schedule.

Unfortunately, this year has been anything but boring.

Between budget drama and the very real possibility of a partial government shutdown, the markets are doing what they always do when uncertainty shows up—they get nervous. And nervous markets tend to overreact first and ask questions later.

When the markets start pacing the room and checking their phones every five minutes, we pay attention. Because jittery markets don’t just affect headlines they show up in rates, pricing, and timing.

For now, rates are flat, and the Fed’s decision not to cut rates did not negatively impact mortgage rates.

Whew.

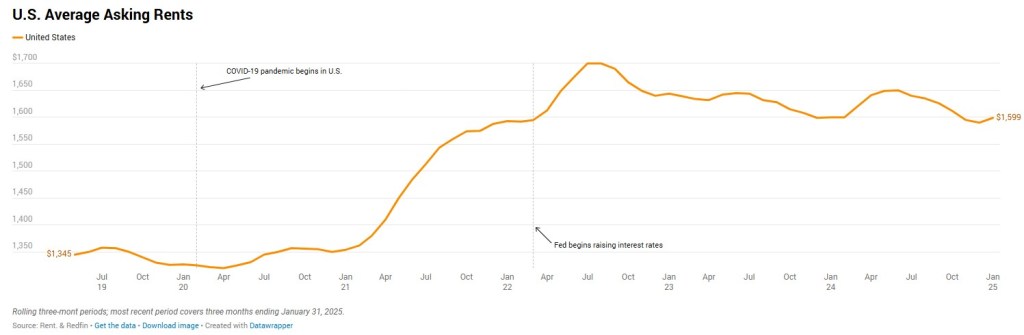

On the inflation front, there’s more good news: rents continue to decline on average, which is helping bring overall inflation numbers down. That trend matters, and it’s one of the quieter tailwinds working in favor of lower rates over time.

Time to get pre-qualified http://www.YourApplicationOnline.com

-

The Feds are Blind, Deliberately. Just need a bit more data…. UPS and Amazon cutting jobs.

There’s a better and more accurate inflation gauge from Truflation, which analyzes 10 million data points yes, 10 million, compared to roughly 80,000 used in CPI and PCE.

And the numbers don’t lie. PCE is at 1.39% and CPI at 1.16%.

The jobs data may appear stable, but that stability is misleading. Consumers certainly don’t feel it, and major employers like UPS and Amazon are signaling job cuts in the tens of thousands.

Jerome, take your hand away from your face and look at the real numbers. There is plenty of room to cut rates.

let’s get pre-qualified today http://www.YourApplicationOnline.com

-

Fannie & Freddie Are Buying More MBS, Ignore the Talking Heads on TV saying don’t drop rates.

Good news: Fannie Mae and Freddie Mac are buying more mortgage-backed securities, which should help put downward pressure on rates.

With the Fed meeting next week, the talking heads on financial shows are out in force, warning that if rates don’t hold, home values might increase and “erase the rate benefit.”

Sure, that’s a point worth considering. But what about the millions of borrowers currently stuck with high interest rates who would gladly trade a slight home value bump for a meaningfully lower monthly payment?

And what about homeowners who locked in ultra-low rates in 2020? Many would like to move, but only if the rate change is reasonable. Mobility matters too.

Lower rates don’t just move markets, they move people.

-

Might have a New Fed Chair Announcement next week. or the week after, or the week after.

OMG you would NOT believe what happened… I’ll tell you next week.

That is exactly the vibe coming out of the White House right now.

New Fed Chair announcement coming next week we hope.

Rate cut this month? Maybe. Maybe not. Inflation is behaving, the job market seems… fine-ish, but as always, perception is doing most of the heavy lifting.The timing of teasing a new Fed Chair while Powell is also hinting at possible rate cuts next week has not gone unnoticed. Feels a lot like, “Big news coming… but let’s circle back.”

The NAR Realtor Confidence Index show more confident first quarter 2026 than in 2025. This is true for most or our industry. we are gearing up for the turn around that has already started.

Start by getting pre-approved. http://www.YourApplicationOnline.com

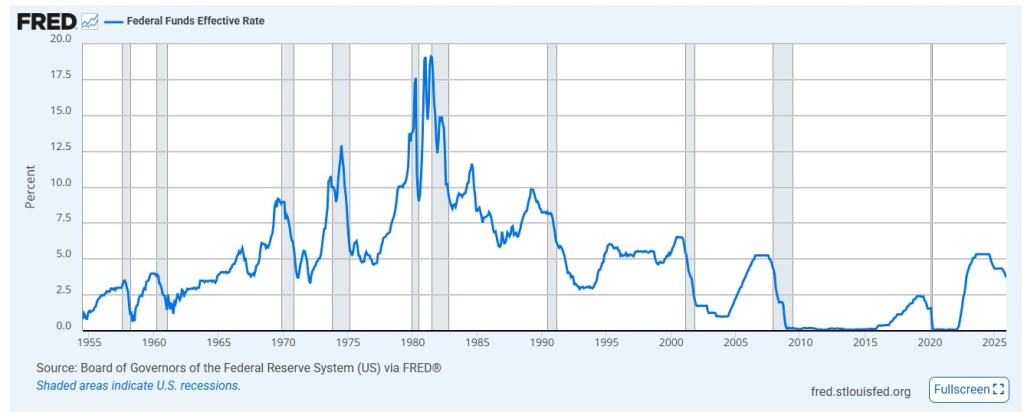

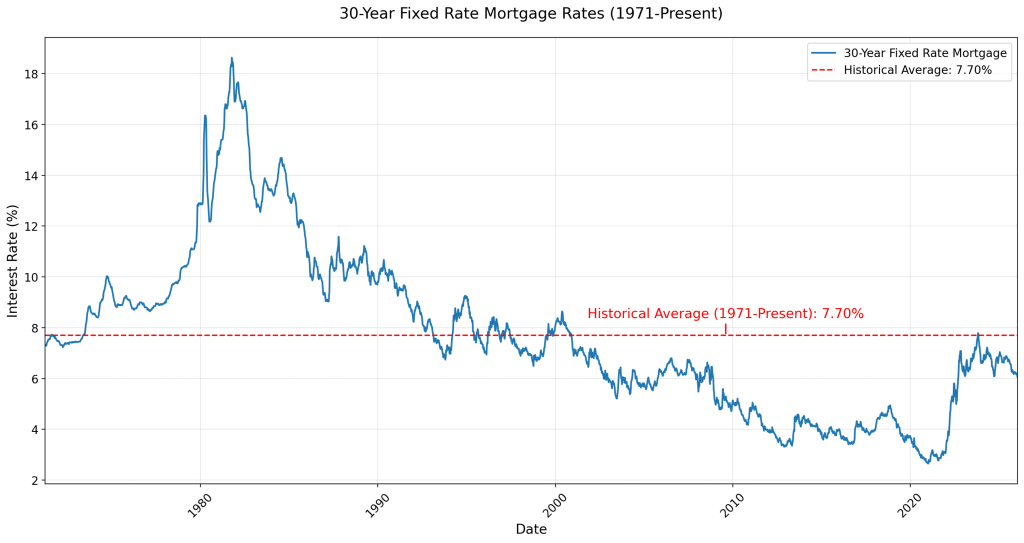

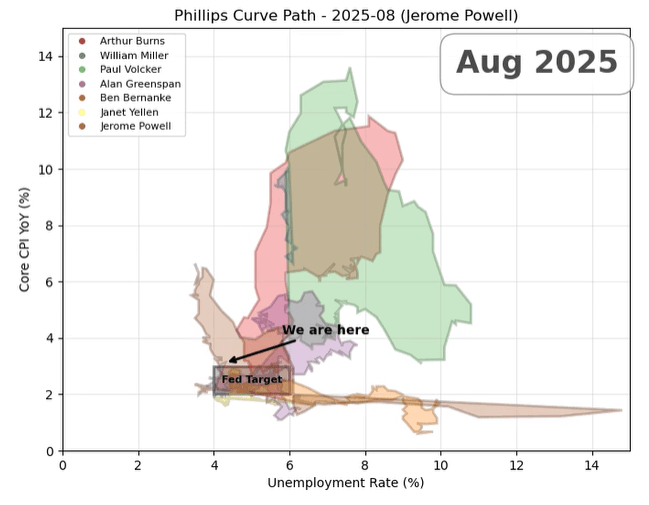

This is a great image of the struggle the Feds over time have been facing regarding Fed Target inflation rate and the Fed rate. Click it has a hyperlink showing progression over time.

-

Inflation is Stalling and Slipping, Fed let’s Get to Getting.

The President backed off tariff threats toward the EU, and Greenland is effectively off the table. That reduction in geopolitical noise matters, uncertainty and instability hurt everyone, particularly stocks and bonds.

On the data front, Q3 GDP growth came in stronger than prior estimates at 4.3%, reinforcing the case that the economy can withstand rate cuts without reigniting inflation. Jobless claims remain stable at 200,000, while continuing claims fell by 26,000, signaling ongoing labor market resilience.

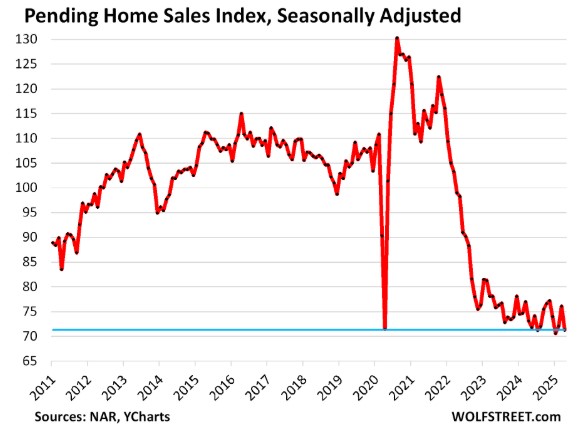

The outlier was Pending Home Sales, which declined 9.3% in December and are now down 3% year over year. That said, we expect this to turn in Q1, as early indicators show buyer activity picking up alongside improved rate stability.

Rates continue to fluctuate, but within a relatively tight range. All in all, the backdrop is constructive, let’s get 2026 rolling.

Online Application http://www.YourApplicationOnline.com

-

Why Refinance your 6.5% rate to 5.875%. Because you will save $72,954.

Current Loan

6.50% | 30-Year

- Monthly P&I: $3,160

- Total interest: $637,722

Refinance at 5.875%

30-Year

- Monthly P&I: $2,958

- Total interest: $564,768

- Interest saved: $72,954

- Cash-flow improvement of ≈ $202/month

20-Year

- Monthly P&I: $3,546

- Total interest: $351,086

- Interest saved: $286,636

- Much faster equity buildup with a moderate payment increase

15-Year

- Monthly P&I: $4,186

- Total interest: $253,407

- Interest saved: $384,315

- Maximum long-term savings, fastest payoff

Takeaway

- 30Y: Best for monthly savings

- 20Y: Strong balance of payment + wealth building

- 15Y: Massive interest savings if cash flow allows

Soft Credit pull, let’s find out. http://www.YourApplicationOnline.com

-

Why Stocks and Bonds Fell Together: When the “Safe Haven” Isn’t Safe

Risk-on assets are those favored when investors are optimistic about economic growth and willing to take on greater risk in pursuit of higher returns.

These typically include equities, commodities, high-yield (junk) bonds, real estate, and certain higher-beta currencies.

Conversely, when investors perceive rising uncertainty or economic stress, capital usually flows into traditionally safer assets such as bonds.

In the current environment, however, U.S. Treasuries are being viewed with more caution than usual, as tariff threats and broader global instability have introduced an added layer of risk to what is normally considered a safe haven.

Rates moved slightly higher today but not as bad as I anticipated.

Let’s get you qualified http://www.YourApplicationOnline.com

-

Lower rates and boy what a difference in home sales. Get Ready and get Pre-Qualified

Yesterday’s New Home Sales data was released, which measures signed contracts on new construction. We’re seeing a 19% year-over-year increase, running at an annualized pace of 737,000 homes, the highest level in three years.

This morning, Existing Home Sales were released and significantly exceeded expectations. Forecasts called for a 2% increase, but the actual number came in at 5.1%.

When rates move lower, buyers pay attention. They also pay attention to home values and in some regions, more favorable pricing. Eventually, that combination creates a tipping point where buyers decide to act.

We may be approaching that moment.

As always, I’ll continue to monitor the data and keep you updated as conditions evolve.

Pre-Qualification Soft Credit http://www.YourApplicationOnline.com

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.