-

The Housing Market Contraction is coming to an end.

Pending home sales rose for the third month in a tow via the National Association of Realtors.

“After nearly a year, the housing sector’s contraction is coming to an end,” NAR top economist said. Pending home sales rose for the third month in a row in February, adding to other signs that the housing market’s retreat is nearly over per the National Association of Realtors.

We do expect rates to trend downward over the next six months, though we don’t have a Crystal ball, we do have strong indications.

Thursday Morning and woke up to Rain in the desert. Have a fantastic rest of your week.

-

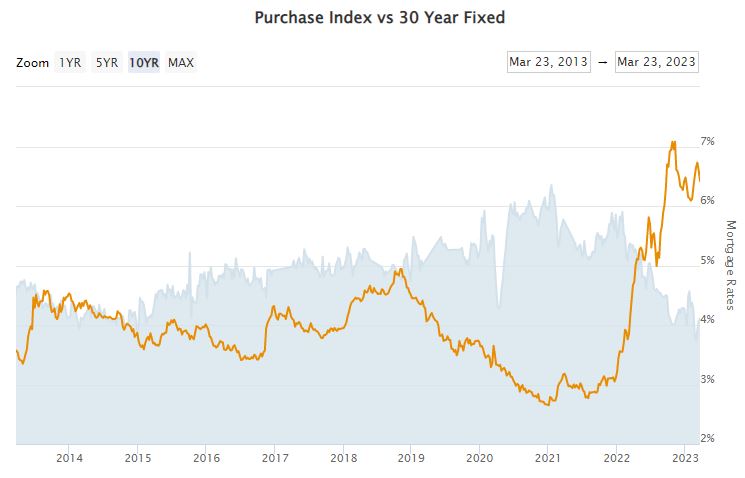

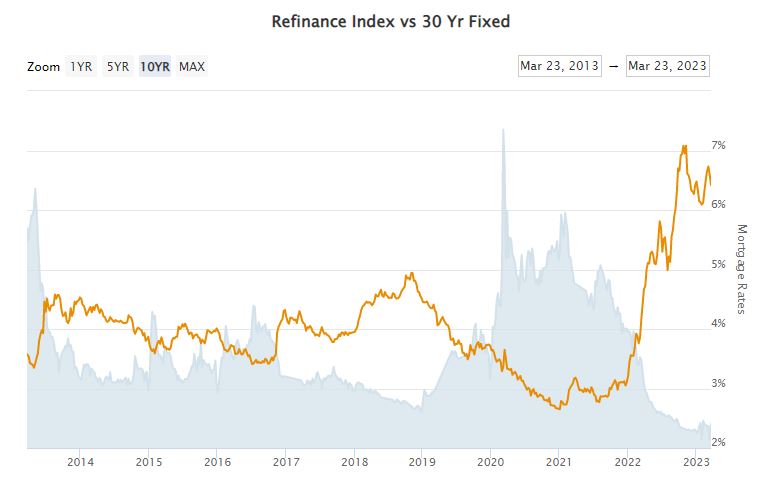

A picture says a thousand words.

Two charts below. Orange line is rates, gray area are applications. First chart is Purchase applications, second chart is Refinance applications. Both up for the fourth week in a row.

Interesting how the applications go up as the rates go down.

Have a fantastic rest of your week and always feel free to reach out with any questions.

-

It takes curiosity to learn. It takes courage to unlearn.

The Media always seems to get it wrong. The FHFA Housing Price Index that measures home price appreciation on single-family homes within the conforming loan limit rose 0.2% in January. Year over year home prices are up 5.3%.

We have a lack of inventory. Rates are still below their peak and it’s spring time. Another silver lining is apartment rents rose 0.5% in March and up 2.6% year over year but down from 3%.

Learning is how you evolve. Unlearning is how you keep up as the world evolves.

-

Interest is the birth of money from money and its the most unnatural way to accumulate wealth. – Aristotle

Interest on money counters the degradation of value over time.

Let’s look at an example: 5% inflation, hum not bad what the harm. But if I told you in 14 years your money would be worth half its value you would be concerned. Systemic inflation has consequences. Controlling inflation is necessary and why we keep hearing the Feds talk about lowering inflation.

On the banking news, First Citizens bank agrees to buy assets of Silicon Valley Bank. Banking stocks are up sharply this morning.

It’s Monday and the sun is out. Go SDSU

-

The Feds Balance Sheet and what it means.

Last night I had a dream that I was a Teepee and a Wigwam, My doctor said I was too tense.

The Fed released their balance sheet figures showing it has risen by almost $400Billion in the last two weeks. This is the money banks are borrowing.

The banks are borrowing on their 2% bond collateral at 100% value but borrowing at about a 4 3/8% interest rate. Why would you do that?

Are the banks doing this for safety or do they really need it?

We continue to watch and see what happens next week. Have a great weekend and always reach out.

-

What goes up Must come down

The Federal Reserve said yesterday it would raise interest rates (fed rate not mortgage rate) by a quarter point to a range of 4.75-5.0%. We are still fighting inflation at over 6% every month since October 2021. The target is around 2%.

There is a strong indication that the Feds will pause as the availability of funds for banks to lend to businesses has tightened. This has the equivalent of a quarter point rise.

Think of it this way, if it’s harder for a business to borrow money to purchase new equipment to expand their business, they may not hire additional employees. This has a ripple effect in the broader economy.

It seems strange to slow down a robust economy with low unemployment and consumers continuing to spend but there is a larger reason. If inflation is not controlled, the money you have today will be worth far less in the future.

We continue to see rate improvement this week. call or email with any questions and have a great Thursday.

-

Don’t be Laggin out of fear

Lack of action is its own action. MBA released their Mortgage Application data for last week showing purchases rose 2% after rising 7% in the previous report. Plenty of buyers getting back into the market.

Today is the second day for the Fed meeting with a press conference at 2pm ET. Will the Feds hike, cut or pause. Most smart people in the room think hike .25% but we are looking for indications there will be a pause moving forward.

Disinflation as I had mentioned in earlier posts is real and coming.

Have a great rest of your week.

-

Is it safe to go back in the water?

Stock market is higher, Bond market a bit lower. The Feds Kick off their 2-day meeting with a statement and press conference at 2:00om ET.

Existing Home Sales, which is a measurement of existing homes sold were up almost 15% in February. This is much stronger than the estimated 5% gain. Sales were down 37% Y/Y in January but February is 22% Y/Y. We are making progress.

Inventory Inventory Inventory is very low at 980,000 but up 15% over last year. There is a 2.6 months’ Supply of homes currently. 4.6 months is considered normal. Active listings are only 578,000 or 1.5 months of inventory. It’s a very tight market.

First Time Home Buyers account for 27% of sales down from 31%. Cash buyers account for 28% of sales down from 29%. Investors made up 18% up from 16%. Investors are seeing the opportunity.

Check back in tomorrow to see what the Feds have to say.

Have a great rest of your week.

-

How can I miss you if you won’t go away?

What’s happening in the banking industry today is far different than 2008. The banks have taken duration risk meaning the assets in the long run are very strong.

Think back to 2008, the word I kept hearing was Derivatives.

Derivatives are financial contracts, set between two or more parties, that derive their value from an underlying asset, group of assets, or benchmark.

There were bad loans with lipstick, cobbled together with A paper loans wrapped in Adjustable Rate Mortgages. Nothing good was going to come of that.

What we have today is an artifact of eased regulations, Fed hikes and Executive greed. The foundation of the Banking system is strong.

Rates continue to improve, get out there and show them who’s Boss.

-

Nowhere to run to, Nowhere to hide….

One of the challenges for money managers is where to put their money. Do you buy stocks or flight to safety, securities. If both these markets are getting beat-up, what’s a money manager to do?

Diversification is key but if all your options have challenges you have to look elsewhere. I’m not sure what the answer is but historically real estate may be a valid option.

Inventory is low, very low. Demand is high and the rates continue to drop.

Have a fantastic weekend. I updated a few of my YouTube videos. Enjoy

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.