-

We just need to break free

The graph displays the 30-year interest rates for a fixed term, spanning over 1 year. Despite reaching a peak in November and experiencing another smaller peak in March, we have been unable to surpass (drop below) the range of 6-7%.

As previously discussed in a recent post about payment disparities and interest rates, there is only a 30% increase in payment when going from a 3.5% to 6.5% loan, not double. Similarly, a shift from 3.5% to 5.125% results in approximately a 15% difference in payment.

These findings are crucial to inspire sellers to place their properties on the market.

I am off to three meetings this morning and just finished my second cup of coffee. Have a fantastic day, Friday is tomorrow.

-

What is Fannie Mae and Freddie Mac Up to. Low Credit better Rates???

Are you feeling confused about Fannie and Freddie’s actions with rates and credit scores?

This Video will provide clarity on the matter, revealing what’s really happening. Take just five minutes out of your day to gain a true understanding of loan pricing and credit risk mechanics.

We’ve reached the midweek mark and the sun is shining bright. Wishing you a fantastic rest of the week!

-

10% rise in Signed Contracts

Spring has Sprung and buyers are out in force. We have the strongest new homes sales data in 13 months. The median home price also rose 3.8% last month to $449,800. This is the forth strong report in a row.

Below is the YouTube Video with a deep dive regarding Fannie Mae and Freddie Mac Low Credit score Risk pricing change and its real impact.

Have a great rest of your week.

-

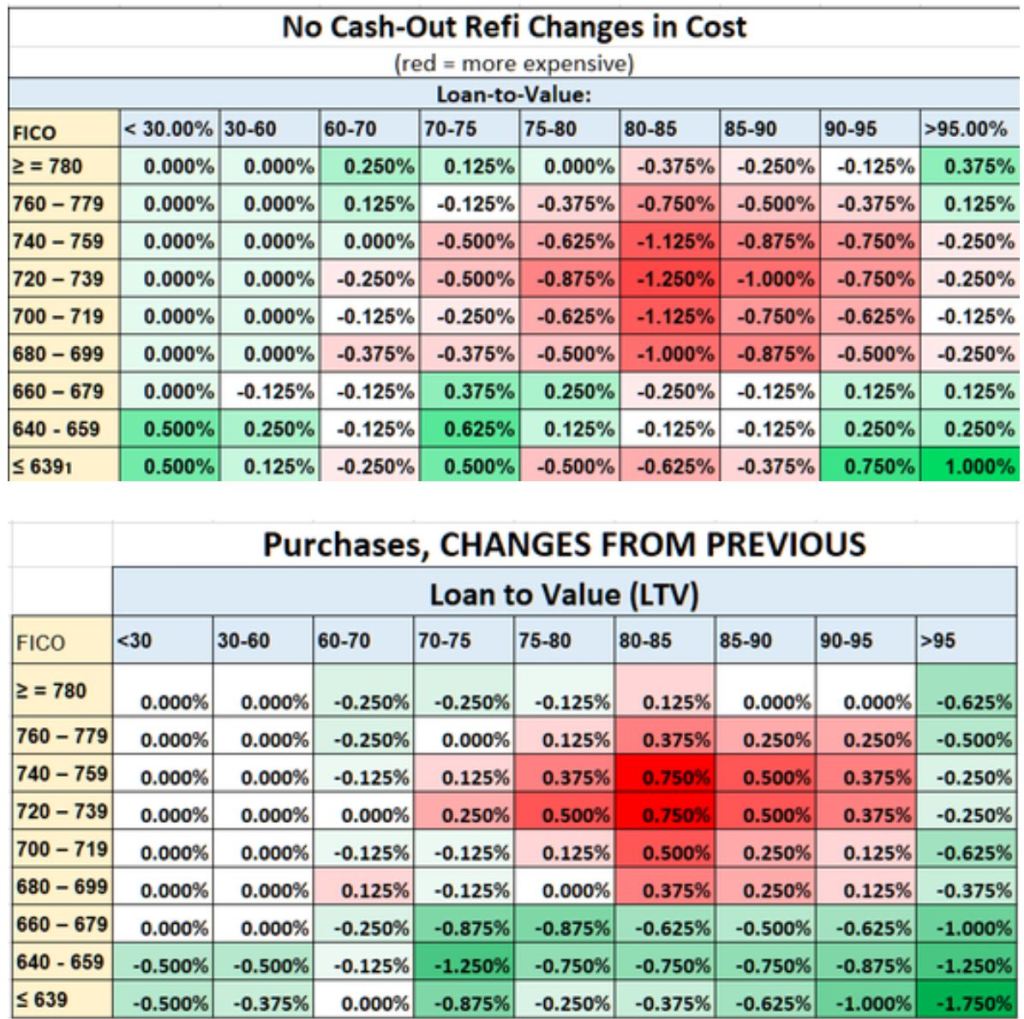

Is There Really a New Unfair Mortgage Tax on those with High Credit?

In the last week my inbox and on the internet has been flooded with this “new” unfair tax on mortgage borrowers with higher credit scores.

Before you Stop paying your bills to cash in on better pricing, let’s separate fact from fiction.

- You will absolutely NOT get a better deal on a mortgage rate if your credit score is lower.

- Low credit borrowers are not paying less than a high credit borrower.

Let’s look at some charts. Red = rising costs. Green= Falling costs.

If you saw the first two charts or it’s your first time seeing them, you can be forgiven to think a low credit borrower is paying less than a high credit borrower.

*LLP is Loan Level Pricing , % cost of the loan amount. That is the % reference in the charts below.

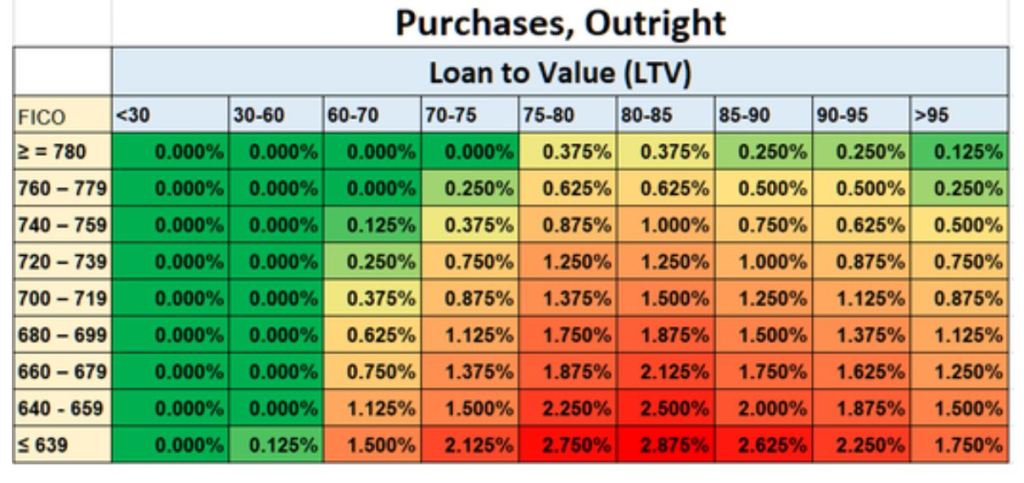

Let’s now look at the ACTUAL cost not the CHANGE.

If you have a 640 credit score, You’ll be paying significantly more than if you had a 740 score.

Freddie and Fannie have a “mission” to promote affordable home ownership. Their comments in the link below.

https://www.fhfa.gov/Mhttps://www.fhfa.gov/Media/PublicAffairs/Pages/FHFA-Announces-Updates-to-Enterprises-SF-Pricing-

Its earnings week so be ready for a bit of a volatile week.

-

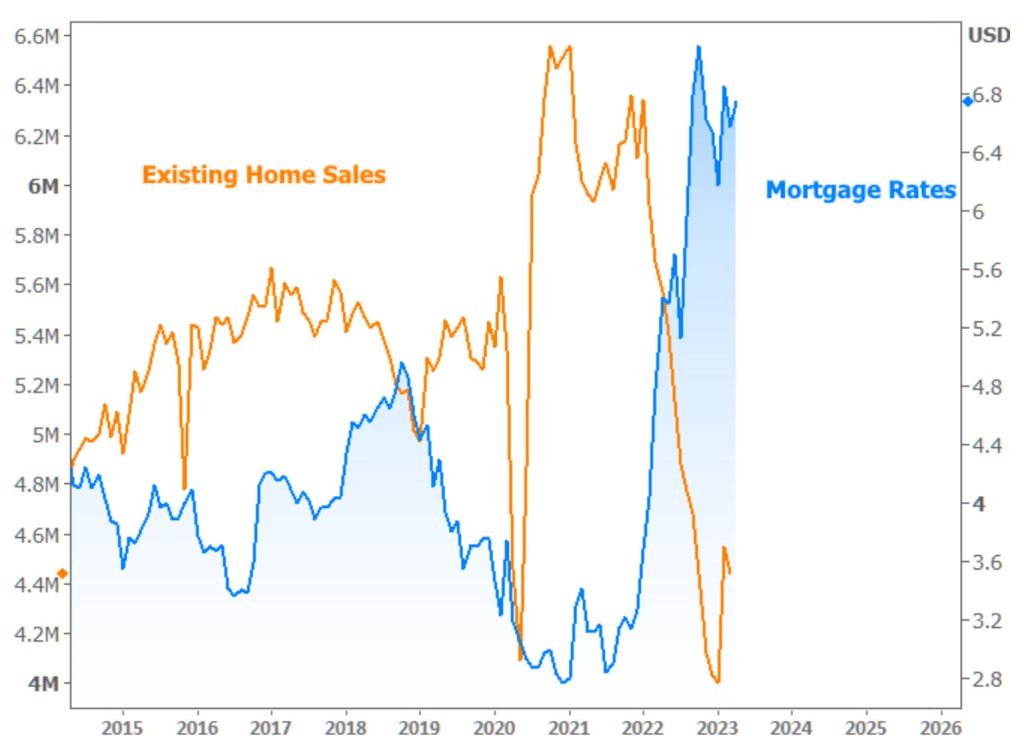

We are just Muddling along

The National Association of Realtors (NAR) Reported the sales of previously owned homes which accounts for a vast majority of all home sales in the US.

Existing sales bottomed out in January at 4.00 million units annually. March numbers came in at 4.44 Million though nice, which was slightly lower than February at 4.55.

Looking at the chart below, it’s hard to overlook the correlation between rates and home sales. This chart helps clarify my 5.0% rate comment yesterday to help motivate potential sellers.

Its Friday enjoy your weekend and I will see you right here Monday.

-

Homeowners have Velvet Handcuffs

90% of Homeowners have interest rates below 5.0% and 70% of those Homeowners have rates below 4.0%. – CNBC News

Interest Rates have to move lower before we can begin to sway these Homeowners in bulk. Lets look at a $500k purchase 20% down just Principle and Interest:

3.5% rate $1,796 6.5% rate $2,528

Our gut tells us it must be twice the payment but it’s actually only about 30% higher. What this tells us is once we are closer to 5.0% interest rate the payment shock will be far lower at only15% higher payment.

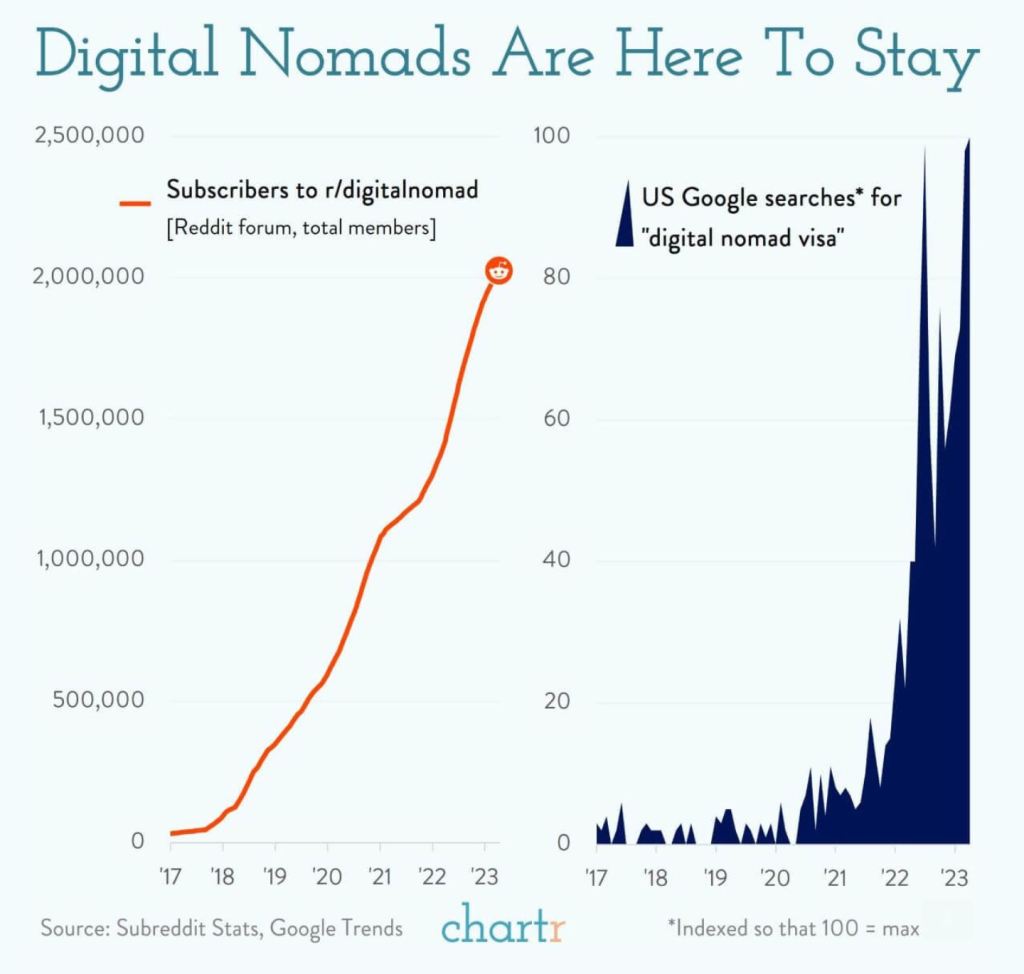

Interesting group below. These are digital nomads that can work anywhere, not just in the United States but the World. COVID has changed our working landscape far more than we may realize.

Have a fantastic Thursday.

-

The Flat Earth Society has members all around the globe.

Good Morning, headed to a Realtor conference so this one will be short. See link to my video regarding Inflation vs Mortgage rates .

Have a fantastic rest of your week.

-

It’s all about housing starts

Housing Starts in March were down by almost 1%, 17% from last year. But single family starts rose almost 3% last month.

Housing Permits i.e. future supply, down 9% from last month and 25% from last year.

We are still undersupplied.

Have a great rest of your week.

-

Don’t be a problem solver, Stop it from being a problem in the first place

We sweat the small stuff because that’s the flame that starts the fire.

This is more of a personal note about our process and how we avoid problems from showing up. Our team is dedicated to ask the hard questions and document what might be an issue before it becomes an issue.

We don’t want to be your friend because friends will tell you what you want to hear, not what you need to hear. If I see something off with the income, I am going to ask. if there are unusual deposits, let’s find out what they are today not at closing.

Mortgage Bonds are having a tough time of it today. We have NAHB Housing Market Index, Housing Starts and Permits and Jobless claims this week.

-

I’ve fallen and I don’t want to get up

Consumer inflation dropped from 9.1% to 5%, Producer inflation dropped from 11.7% to 2.7%.

Retail Sales in march fell 1.0% more than the expected 0.4%. Core Retail Sales which strips out automobile sales and gas, fell .03%. The expected drop was 0.5%.

Industrial production or output increased 0.4% in March was double the estimates of 0.2%. This shows that factories are at greater capacity than expected and could be inflationary.

This is putting some pressure on the bond market i.e. slightly higher rates.

Its Friday, what a week. Below is a Gallup Poll from 2000 Americans’ Cell phone Ownership and intentions.

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.