-

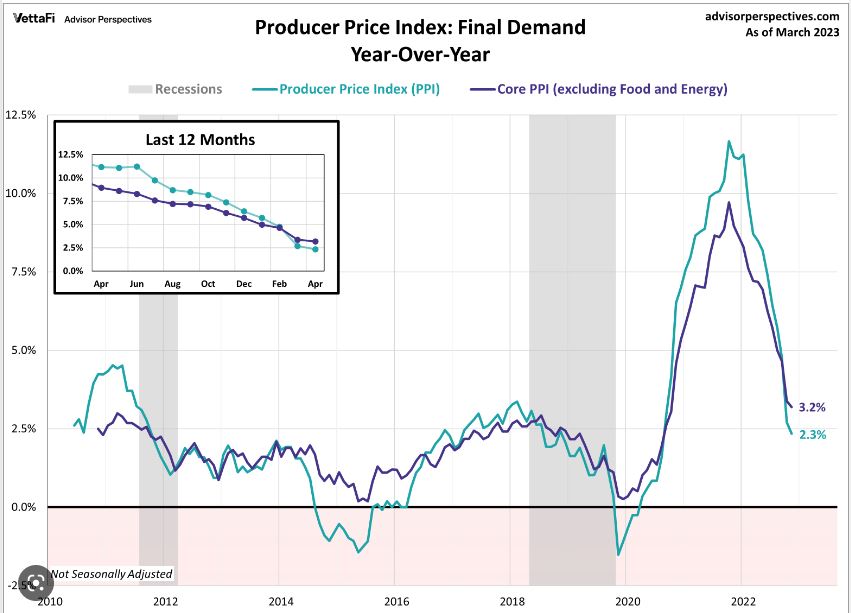

PPI what does it mean – hint good news

The April Producer Price Index or PPI is a measure of wholesale inflation, while the Consumer Price Index CPI measures the Price paid by consumers.

We are seeing a different take from the Producer or Manufacturer regarding inflation.

Overall producer inflation increased 0.2%, less than the expected 0.3%. Our year over year has declined from 2.7% to 2.3%. This is huge and very good news. The Peak was 11.7%.

We are seeing rate improvement as expected. Have a great rest of your week.

-

Tomorrow is here Today CPI 10th straight drop in inflation

The Consumer Price Index (CPI) Which measures inflation on the consumer level, reported at 0.4% inline with expectations and more importantly a decrease in inflation or 0.1% to 4.9% year over year.

I often get phone calls with the same question “what are rates today”

This is what we look at everyday. Green is rate improvement, Red the opposite. What is fascinating is how cyclical it is (UMBS 30yr 5.5% chart). Up is lower rates.

If I keep looking back, let’s say 6 months, I get this chart.

It’s not just what’s the rate, it’s when is the rate, when should I lock, or should I float for a few days. Ask your lender these hard questions, then ask me and let’s see what the difference is.

Its Wednesday, headed to a Real Estate weekly meeting this morning.

-

Our Friend CPI is back Tomorrow

Tomorrow Morning the highly anticipated April Consumer Price Index report will be released.

This could be the beginning of when we feel inflation would start to make additional progress and potentially a rate drop.

Year over Year inflation numbers means we are replacing last year’s April 2022 with this year’s April 2023 number. If this year’s inflation number is lower than last year’s April inflation number, the total inflation calculation will go down.

Sunday evening, JPM Chase and Goldman Sachs released their estimates and they felt inflation reading would not see much of a change.

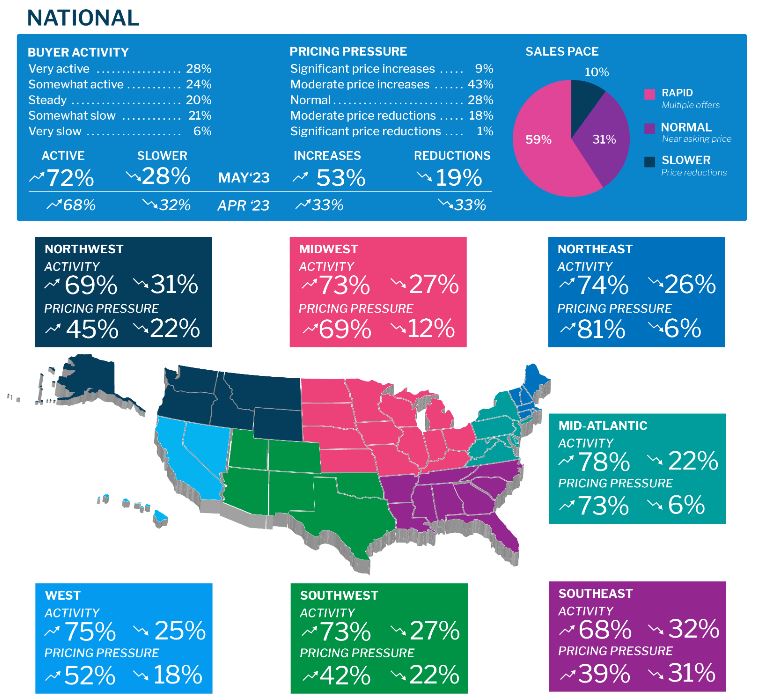

Below is the buyer activity survey.

Have a great rest of your week.

-

Necessary Luxury

Coco Chanel once described luxury as “a necessity that begins where necessity ends” — a maddening phrase for any old-school economists whose models can’t understand why people spend $30,000 on a timepiece that tells the same time as a $30 watch. The answer, of course, is a combination of two very human things: because they can, and because it feels good. -Chartr

Have a fantastic week and always feel free to reach out anytime.

-

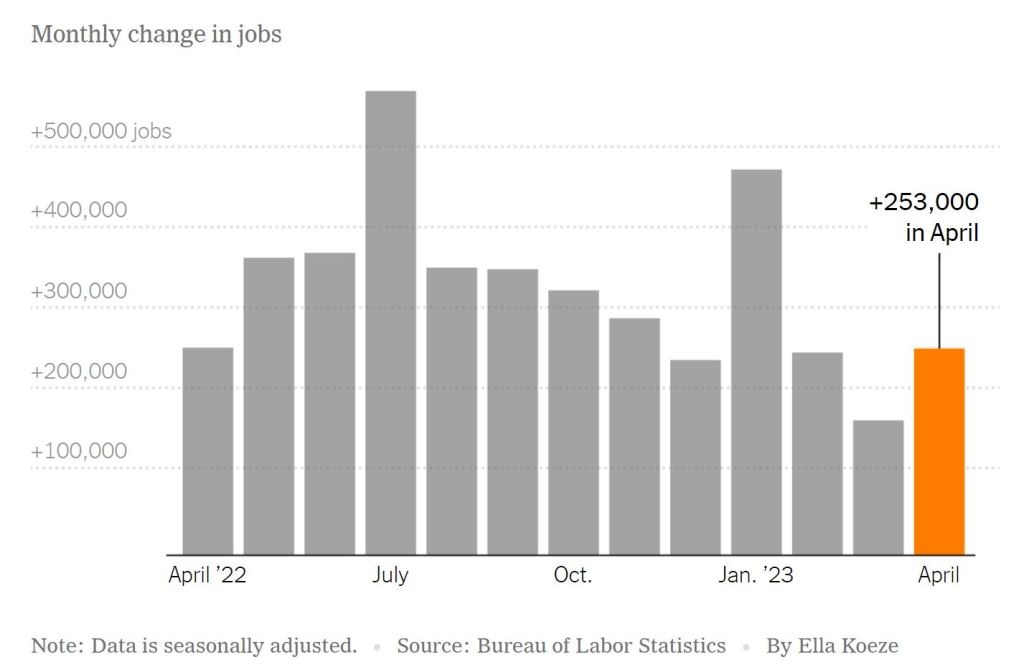

Jobs report remains strong

More Jobs were added in April than in previous months despite the Federal Reserve’s efforts. Unemployment rate drops to 3.4%

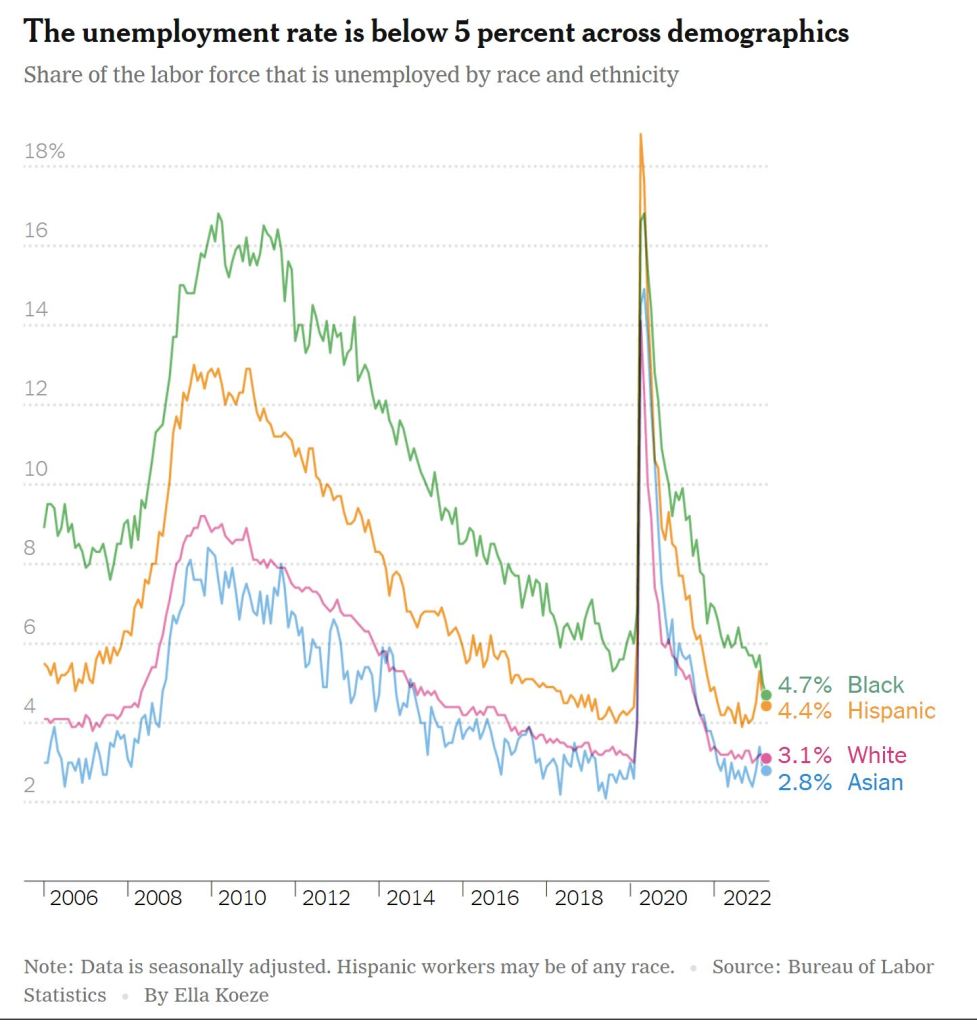

Another data point for the unemployment rate.

The economy is stubborn, this is a good thing, but the Feds are not happy this morning…..

-

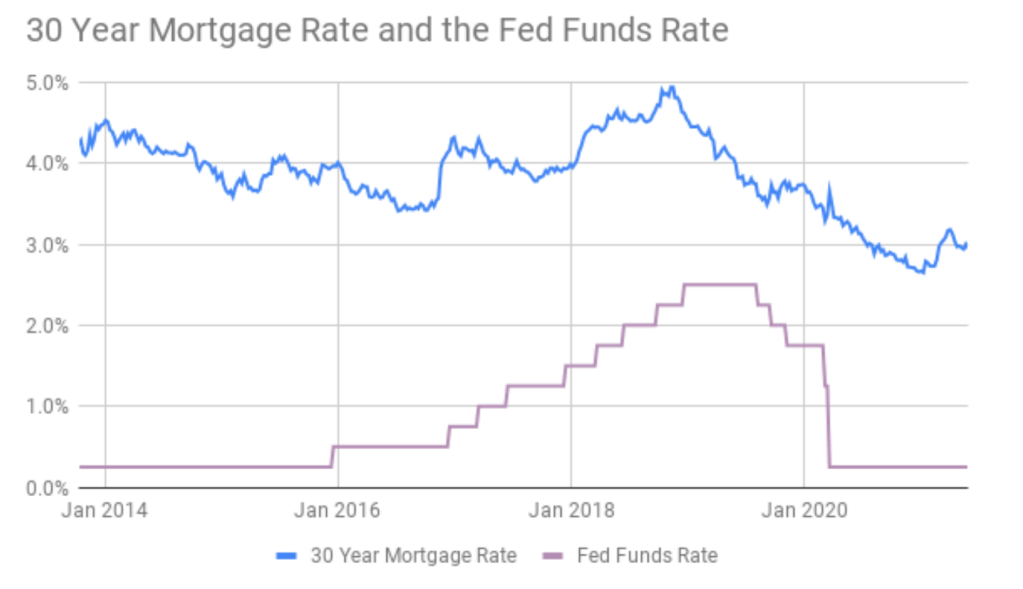

Fed Rate and Mortgage Rate aren’t Married to each other, they are not even dating….

I love graphs, they tell you so much with so few words. But first lets quickly understand the difference between the Fed Funds rate and the Mortgage Rate.

Fed Funds Rate is the rate banks borrow overnight to satisfy liquidity requirements set by regulators. Banks then pass that rate to its clients affecting short term lending:

- Car loans

- Credit cards

- HELOCs Home equity line of credit

- ARMs Adjustable Rate Mortgages

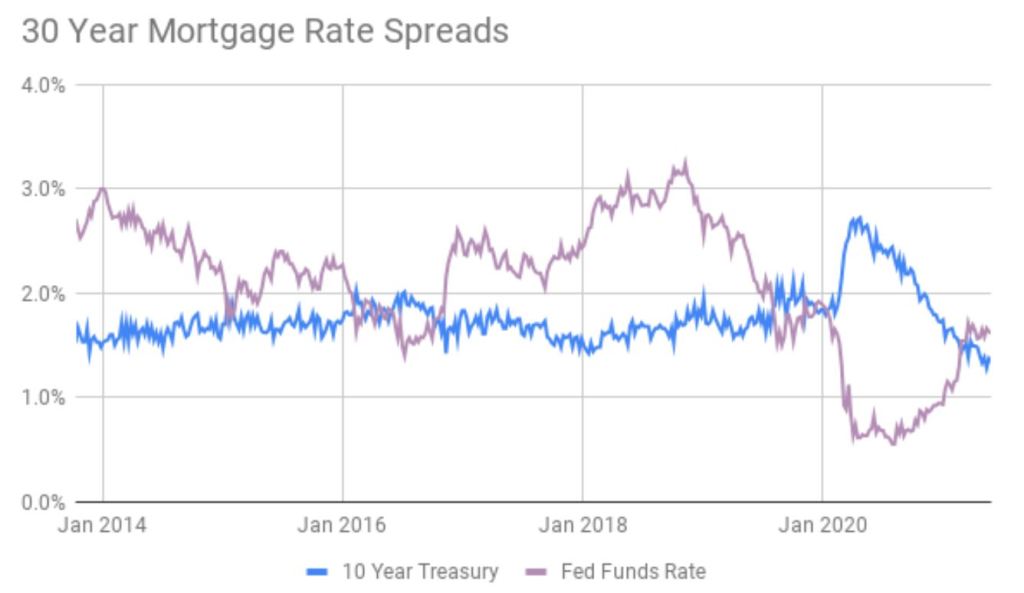

Mortgage Interest Rates reference the yield on the 10-year Treasury bonds.

When the Fed raises rates, Mortgage rates typically go down.

This is the 10 Year Treasury bond vs the Fed Rate.

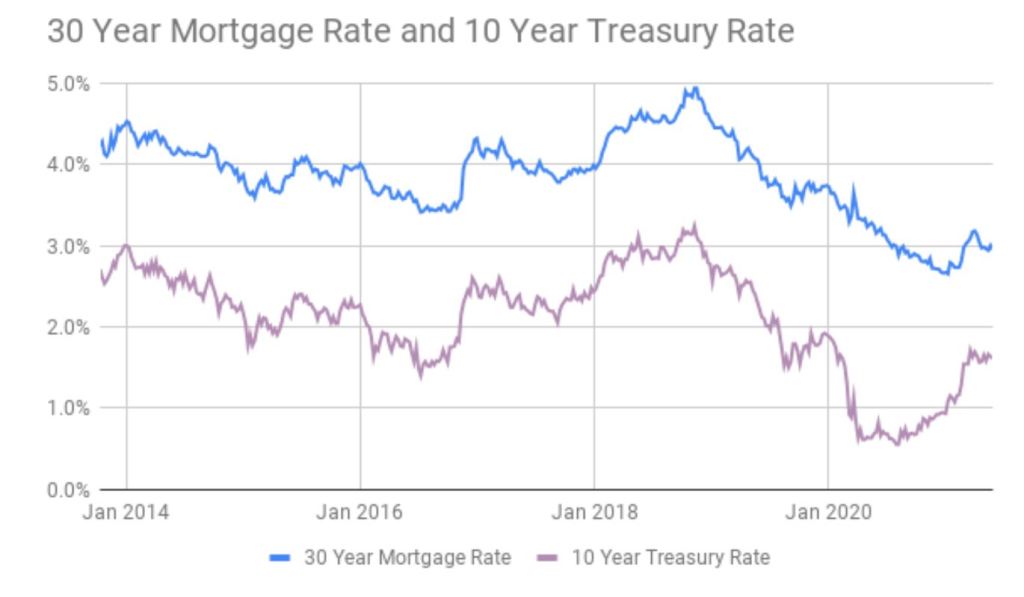

Let’s now look at the 30 Year Mortgage vs the 10 Year Treasury Rate

In conclusion…. When you hear the Feds are raising rates, run to your lender to get pre-qualified for a Mortgage or ask about refinancing your loan.

Have a great rest of your week and always feel free to reach out.

-

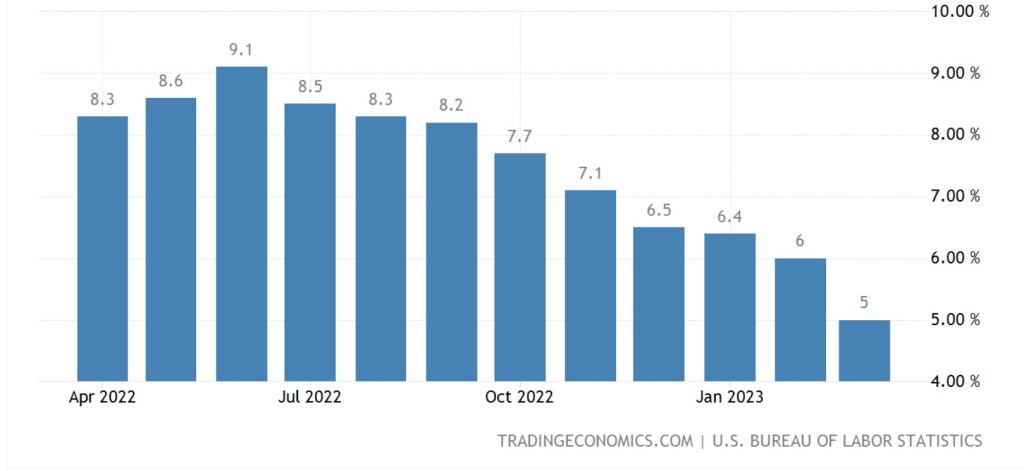

Inflation is coming down, Why the 25bp hike.

We just don’t know. Producer Price Index – PCE is down sharply from 11.7 to 2.7%. Inflation is down and the low and mid level regional bank issue that could create more strain and potential banking crisis. They make up 40% of all loans.

Rates have improved this week. I will hang onto that.

-

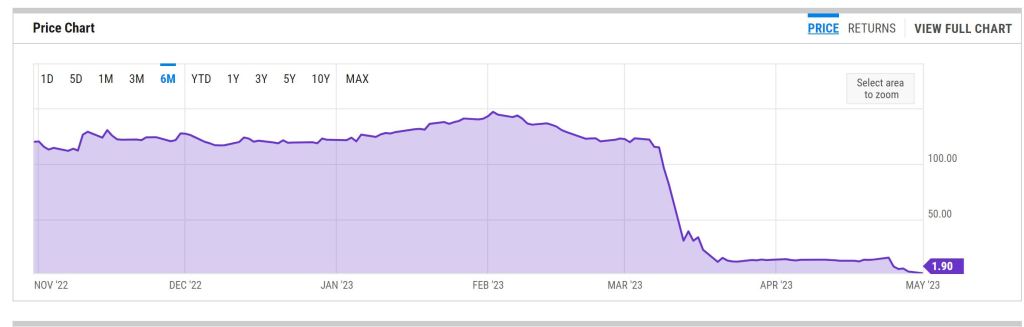

Is that a piece of Ice or an Iceberg in front of us?

With Sunday’s news of the downfall of First Republic Seized by regulators into FDIC receivership, my first thought was how is this going to affect the bond market.

Typically this type of disruption would mean bond prices drop as well as interest rates. This did not happen. We saw minimal change at best. The market is calling this a piece of Ice not an Iceberg.

The Feds are expected to raise the Fed rate by 0.25 basis points Wednesday.

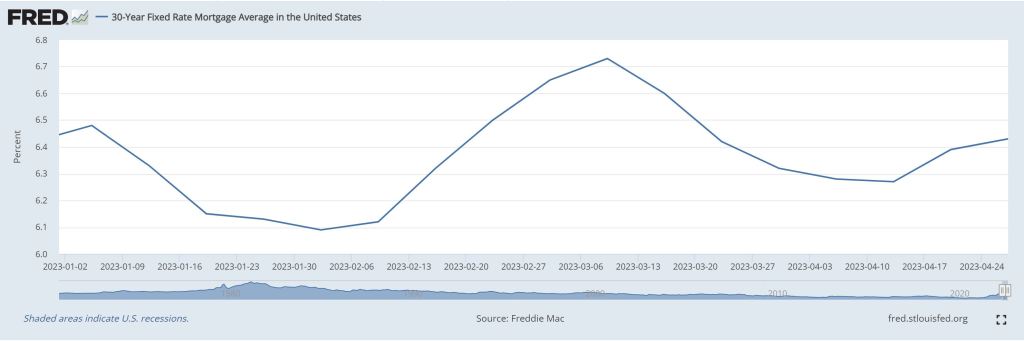

Rate average this year.

Headed into a meeting this morning, have a fantastic week.

-

Double Coincidence of Wants.

I want what you have and you want what I have. Money solves the challenge of barter.

First Republic was flying high borrowing money at very low interest rates and then turning around and lending to homeowners below market average rates. Tough to compete with a lender offering a half to a full point lower than the national average.

As the interest rates rose those mortgages at the low interest rates started to lose their value. This on top of Silicon Valley Bank collapse spooked depositors and we had another run on a bank. Fortunately JP Morgan stepped in last night after the Feds announced the seizure of the bank.

The FDIC believes this and the other smaller regional bank failures are Unique within the banking industry.

Have a fantastic Week.

-

What goes Up must come Down

Personal Consumption Expenditures (PCE) showed inflation rose .01% in March, less than the expected 0.3%. Year over Year we have a decline from 5.1% to 4.2%. Better than the Markets had expected.

We have already seen some rate improvement. Lets see if the Feds are still driving looking at the rear view mirror.

It’s Friday, what a week. enjoy the weekend and always feel free to reach out.

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.