-

There is a crack in the Armor and it’s good news.

CPI Consumer Price Index is the measure of change over time and is the prices paid by consumers for a market basket of good and services.

Why this number is important is it reflects inflation which is the value of money over time. The lower the inflation the less erosion of value.

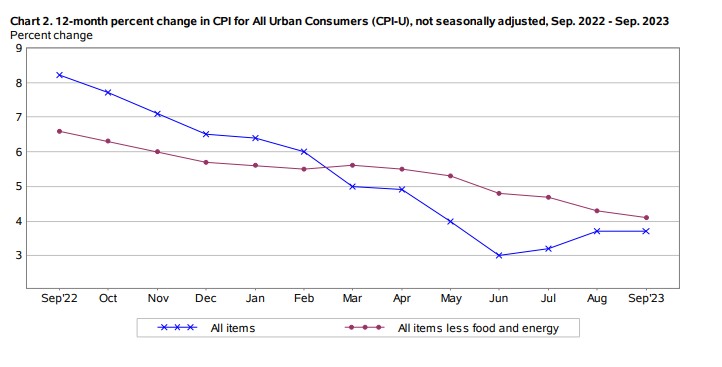

October’s CPI number was unchanged and seasonally adjusted only rose 3.2 percent over the last 12 months compared to September’s numbers at 3.7%.

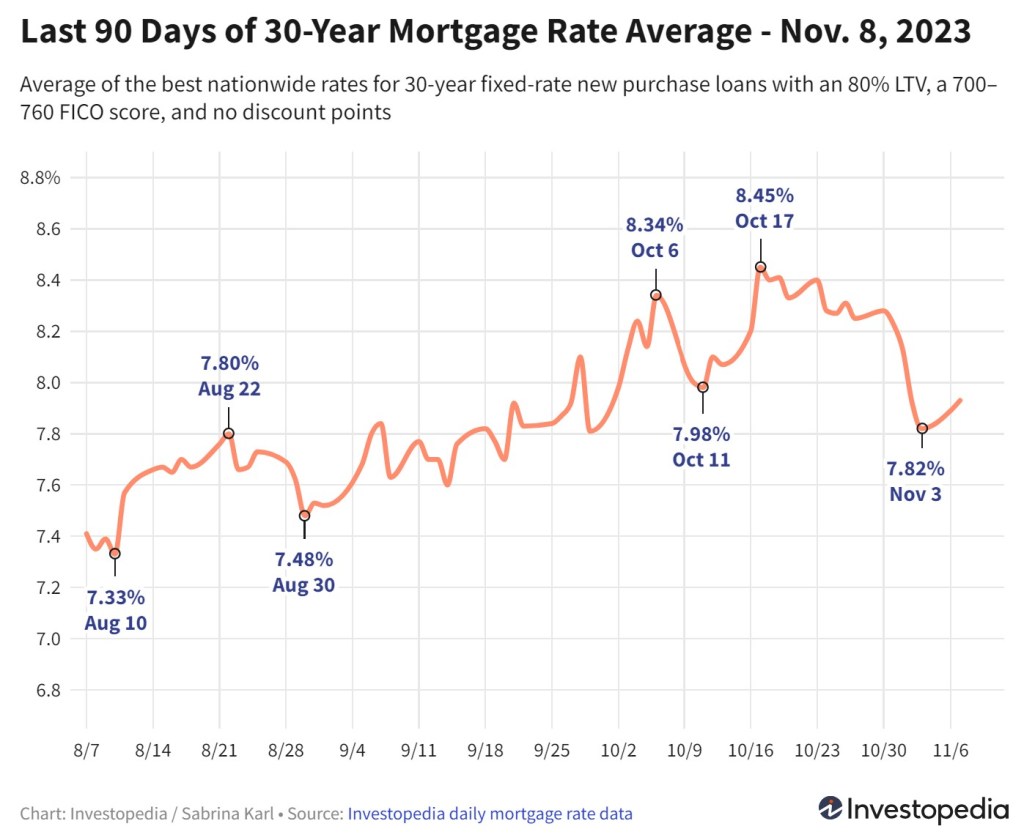

The graph below is the daily change in Mortgage interest rates. Up is lower rates. October 16th was 8.0% interest in the news. As you can see we have slowly and steadily moved off those high rates.

Get out there and get pre-approved. I keep harping on this for a good reason. We do Soft Pull Credit on all of our pre and conditional fully underwritten approvals. No harm to your credit.

We can already see it getting busier, so don’t be caught off guard when the rates really drop.

-

You can Use Logic to justify almost Anything, that’s its Power and its Flaw.

We look at numbers all day long and this week is no different. As I parse out the data, its easy to justify a conclusion.

The Consumer Price Index Report will be released tomorrow morning with a consensus that inflation will drop from 3.7% to 3.3%. This is partially due to decline in oil prices.

The Core inflation that strips out energy and food prices should stay flat. Shelter costs have been on the decline and are now 1.2% lower year/year.

We are holding onto rate gains like a 2 year old and their blanket.

As more data comes in this week, we hope to see continued drop in rates. Lets all be ready for 2024. Remember we do all Soft Pull credit for pre-approvals and fully underwritten pre-approvals. No harm in being proactive.

-

Triple Whammy but we recovered

Mortgage bonds were impacted by comments from Fed Governor Bowman, a weak 30-year bond auction, and remarks from Fed Chair Powell. However, we managed to recover.

Bowman continues to advocate for more hikes, despite being a lawyer rather than an economist. She highlights higher energy costs (down 17% in the last month), questionable job and wage growth.

The 30-year bond Auction did not meet expectations. China reported a system hack, preventing them from buying bonds, and there has been a noticeable decrease in foreign demand. In 2010, 50% of Treasuries were foreign-owned, whereas now it stands at 30%.

Powell’s recent statements caused a spike, and he appeared more hawkish than in his previous statement.

The good news is the market and rates are holding steady.

-

Don’t Worry Be Happy

Average, Normal, predictable all good words the market loves. Initial Jobless Claims came out remaining at a relatively low 217,000. Continuing Claims rose 22,000. Employers are holding onto their workers.

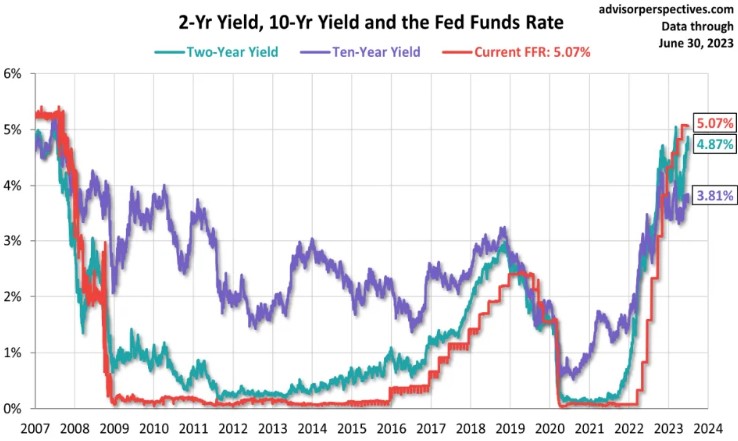

Interest rates are holding their gains over the past week. We are advising our clients to Float any existing pre-locks as we watch the 10-year Mortgage50-day moving Average.

There are floors and ceilings in the stock and bond market. These are imaginary barriers but turn out to be real resistance levels. Right now the 10-year bond broke beneath that 50-day average at 4.57and has created a new ceiling. The floor is 4.42% and if we can fall through we will continue to see rate improvement.

Looking at the graph below, Normal for the 10y bond is arguably around 3.00%. we are at 4.57%. I want my cake and eat it too but that’s not realistically in the cards.

2024 will be an amazing year, I see it coming. Feds will lower their Fed Funds Rate, Bonds will be back to normal and Mortgage rates should be more palatable.

-

People choose their path out of fear disguised as practicality

Mortgage applications up in responds to lower rates.

Oil Prices now below $77/barrel. Manheim Used Car Index fell 2% last month down 4% for the year and slower job growth. These are all strong participants in the inflation calculation giving a positive impact to rates.

“Last week’s decrease in rates was driven by the U.S. Treasury’s issuance update, the Fed striking a dovish tone in the November FOMC statement, and data indicating a slower job market,” said Joel Kan, vice president and deputy chief economist at the MBA.

We could be headed for a perfect storm. The adage the early bird gets the worm may be right.

We might think we are being practical and smart by waiting, but I believe it’s hiding our fear of commitment. Go get your worm…

-

“Two things define you: Your patience when you have nothing and your attitude when you have everything.” –George Bernard Shaw.

In the upcoming two quarters, we could witness a significant decrease in inflation rates. Energy prices have fallen, rental data indicates a decline, and the trend of decreasing prices for used cars has persisted.

Maersk, one of the largest shipping companies responsible for 18% of worldwide capacity, reported their earnings and indicated a subdued demand.

Think of the last two years playing the musical chairs game. The problem is we have been walking in circles so long hearing the same song, we forgot what we were doing.

The music is going to stop and you need to be ready for the drop in rates, increase in housing inventory and be ready to pounce.

All of our loan applications for pre-approvals and full underwrites are SoftPull credit. Get pre-approved and be ready.

-

Rates Holding onto gains

This week and the next two months will be the Tell. Will the interest rates and Bond Yields continue to drop?

Now is the perfect time to take the proactive step of getting pre-qualified with a complete underwrite. The market can fluctuate rapidly, and being prepared is crucial. All our loans involve Soft Credit Pull, allowing us to fully underwrite your file without the need for a hard credit inquiry. Once you are in contract, then we will do a hard credit pull.

Pre-qualification offers you peace of mind by giving you a clear understanding of what you can afford. Stay ahead of the game and make informed decisions about your financial future.

-

Life is like riding a bicycle. To keep your balance, you must keep moving. -Albert Einstein

This is a tough post. I am going to share numbers that sound harsh and depressing but it’s the pill we have to take in order to get to the other side.

BLS Bureau of Labor and Statistics reported 150,000 jobs created in October below the estimated 180,000 expected. September and August job numbers were also revised down.

Unemployment rate now at 3.9% up from 3.8%. Hourly earnings rose 0.2% but lower than estimates and average weekly hours worked fell slightly from 34.4% to 34.3%.

Multiple job holders, increased 205,000 indicating people are having to pick up extra work to get by.

The economy is slowing down giving the Feds the green light to continue pausing the Fed Fund Rate and start looking at lowering next year. Rates are expected to drop, housing inventory will rise and we will be back on our feet.

Remember if the Unemployment rate is 3.9% that means that 96.10% are employed.

-

What is Quantitative Tightening?

Read the blurb below and I will talk on the other side.

Quantitative tightening (QT) refers to monetary policies that contract, or reduce, the Federal Reserve System (Fed) balance sheet. This process is also known as balance sheet normalization. In other words, the Fed (or any central bank) shrinks its monetary reserves by either selling Treasurys (government bonds) or letting them mature and removing them from its cash balances. This removes liquidity, or money, from financial markets.

The Feds paused on raising the Fed Fund Rate. His keyword in Yesterday’s statement was “Financial”. This is what Quantitative Tightening means. They are selling Treasurys (bonds) and those that mature are being removed from its cash balances.

The Fed has a high likelihood of not raising the Fed Fund Rate. In fact with (QT) they could start talking about cut in rates.

-

There is a Wild Card in the deck and Rate projections 2024

What will the Fed statement be at 2pm ET and Powell’s comments at 2:30pm ET. We entirely expect a pause but Powell stirs the pot.

JOLTS report – Job Openings and Labor Turnover Survey, shows job openings in September, rose 9.5M to 9.55M. Job openings rose but hiring rate stayed the same at 3.7%. This is a low number. Also the quit rate is 2.4%, another low number.

Now let’s look at the ADP Employment Report. 113,000 jobs created in September, expectations 150,000. Let’s put this into perspective.

3-month average: 127,000

6-month average: 236,000

12-month average: 225,000

2022 average: 306,000

Another interesting data point is the annual pay for job stayers (increased 5.7%) and job lookers (increased 8.4%). You might think these are high numbers but when you take a closer look you see they have cooled considerably from the highs of 8% and stayers 16%. This can be equated to the big post pandemic pay increases that seem to be behind us.

The Mortgage Applications report from MBA shows both purchase and refinance applications down. If you are looking for a home, now might be the time. less competition.

Projected interest rates for the next 12 months.

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.