-

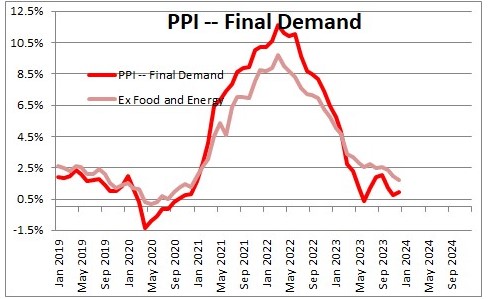

It’s getting Chilly, PPI numbers in and cooler than expected.

The Producer Price Index (PPI) report indicates a decrease in wholesale or producer inflation, contrary to market expectations. Here’s a breakdown of the key points:

- December PPI Movement:

- Actual: -0.1%

- Expected: +0.1%

- This means that prices at the wholesale level fell by 0.1% in December, against the market’s anticipation of a 0.1% increase.

- Year Over Year (YoY) Rise:

- Actual: +1%

- Expected: +1.3%

- The YoY rise is only 1%, falling short of the market’s expected 1.3% increase.

- Core Rate (Excluding Food and Energy Prices):

- Actual: 0%

- Expected: +0.2%

- The Core Rate, which excludes volatile items like food and energy, remained unchanged at 0%, while the market expected a 0.2% rise.

Implications:

- Lower inflation: The decline in producer prices suggests lower inflation, which can benefit consumers as cost savings may be passed on to them.

- Mortgage rates: Lower inflation often translates to lower mortgage rates, which could spur the housing market.

Future Outlook:

- The data might increase the likelihood of the Federal Reserve (FED) lowering interest rates in March. Lower inflation and the potential for economic stimulus are factors that could influence the FED’s decisions.

Conclusion: The PPI report indicates a trend of lower inflation, potentially leading to benefits for consumers and impacting financial markets. Keep an eye on how these trends evolve, especially with regard to FED decisions. Have a great weekend, and see you on Tuesday!

- December PPI Movement:

-

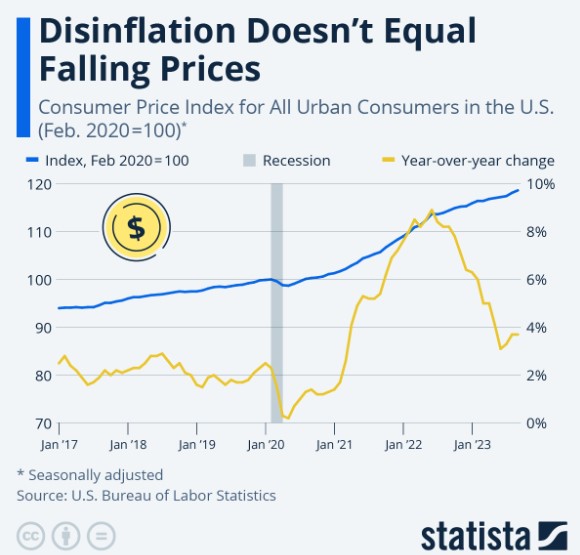

Deflation or Disinflation What’s the difference? CPI numbers in.

Consumer Price Index (CPI) numbers are in, with inflation rising by 0.3%, slightly higher than expected. We are now at 3.4%.

Taking a closer look, these are year-over-year comparisons, so as we move forward, the previous year’s inflation data comparison becomes tougher to surpass.

You may hear that the last mile is the toughest. The Fed wants a 2% inflation rate.

One reason consumers are dissatisfied, even though the unemployment rate is at historic lows, inflation has dropped significantly and new and used car sales have dropped over 37%, is because what you purchased a year ago is over 7% more expensive today.

If inflation were 0%, that loaf of bread would still cost 7% more than last year.

Disinflation is the slowing of inflation, which is what has happened over the past year.

Deflation occurs when the inflation rate is negative, and prices are falling.

We are in the Disinflation period not Deflation.

-

Refinance? Yes and the applications tell a larger story.

The Mortgage Bankers Association (MBA) measured a 19% volume increase from the previous week and up 30% from the same week a year ago. This is also true for Purchase applications but not quite as dramatic.

The buyers and sellers are coming out of the woodwork and testing the waters. When refinances are up, it’s a strong indication the Home Owners have noticed the rate drop.

The flood gates are going to open so be financially prepared and get pre-approved for a mortgage.

-

Inflation Data over the past six months Indicate…. -Fed Gov Bowman

What a difference a day makes. Fed Governor and voting member Michelle Bowman stated that the Fed’s actions are bringing down inflation.

Why this is important is that she was one of the more hawkish members, indicating two more rate hikes just last month.

Thursday is the day the CPI – Consumer Price Index inflation report comes out for the month of December. We may see a slight rise in inflation from 3.1% to 3.2% or it might remain flat.

The Core inflation, which strips out food and energy, is expected to drop, which the bond market will likely favor.

-

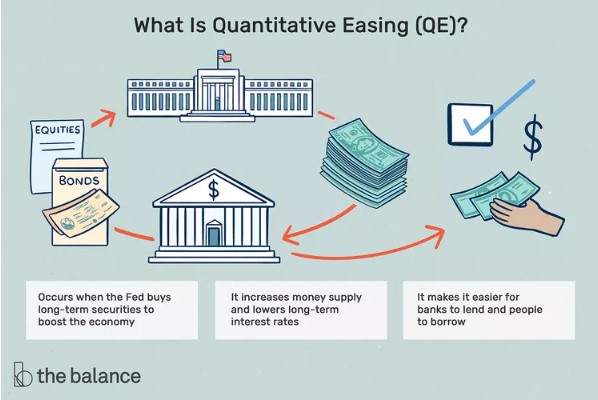

What Happens when the FED starts buying Treasuries again?

For the past two years, the Fed has been selling off its balance sheet of Treasuries or Bonds. The impact is the reduction of the money supply, making it more difficult and expensive to borrow money, in turn, slowing the economy and raising interest rates.

On the flip side is Quantitative Easing or QE. This is what the Fed had been doing starting as far back as the 2008 financial crisis and ending two years ago. The effect of all this purchasing has been lower interest rates and arguably, artificially low interest rates.

QE is used when the Fed wants to stimulate the economy and reduce interest rates on long-term securities.

Dallas Fed President Lorie Logan said she feels it’s appropriate to consider reducing QT or their sell-off of the balance sheet.

This is another data point when the question comes up: ‘When will interest rates drop?’”

-

Is the BLS Jobs Report correct?

BLS – Bureau of Labor and Statistics has revised their prior numbers lower every month on average by 40k, totaling almost 500,000 job revisions since January 2023.

October was revised lower by 45,000 to 105,000, and November from 199,000 to 173,000.

The market relies on these data points, but if you can’t trust the data, who can you trust?

This morning, the market reacted negatively to the better-than-expected jobs numbers but then remembered two things: it’s December’s numbers, which are always strange, and the anticipated revised numbers surely to come out next month.

The 10-year bond yield is lower but started off the morning up.

Average Hourly Earnings rose 0.4%, hotter than estimates. This puts pressure on inflation and the Fed’s pending rate cuts.

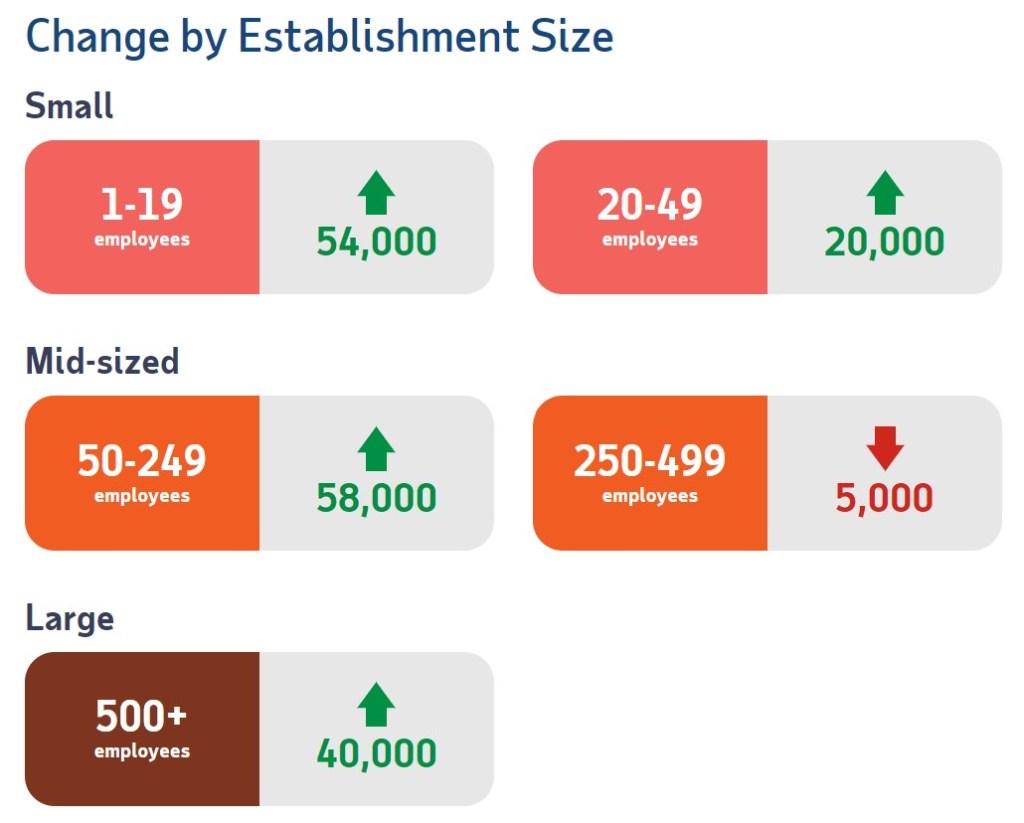

But as we look under the covers, the actual job creations to job losses paint a weakening picture with more part-time jobs. This is why the bond market shifted gears to our positive, i.e., lower rates.

It takes a bit to read and digest the vast amount of data that came in this morning, so we forgive the market for initially overreacting.

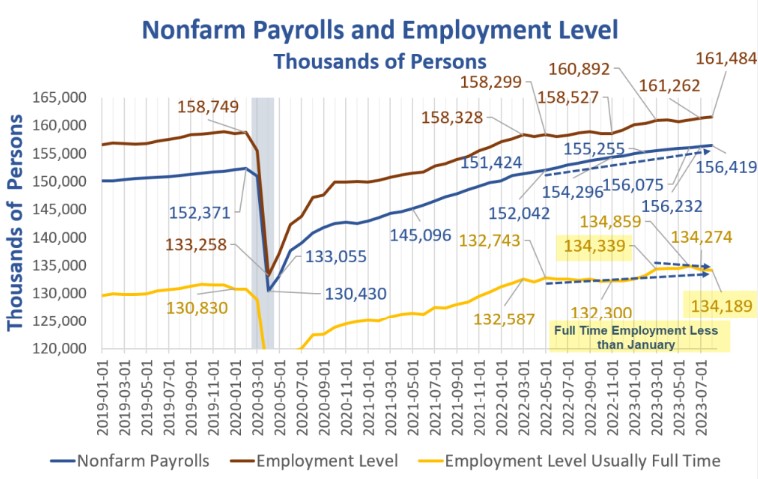

Slightly dated graph, but it still gives me a headache just looking at it.

-

ADP Numbers, Construction leads the way. Changers still benefit over Stayers.

ADP Employment report is out and was slightly stronger than expected at 164,000 jobs compared to the 130,000 estimated.

October and November numbers were 100,000.

Another aspect of the ADP report is the Stayers vs the Job Changers. Both these numbers or % are on the decline. The job stayers had a pay increase of 5.4% slightly down from 5.6%, the job changers averaged an increase of 8.0% down from 8.3%.

To put this in context, last year the Stayers saw an increase of 7.6% and a 15.1% increase for the Job Changers.

What this means is we are settling in. The benefit of changing your job is less attractive and the employers know it but still want to retain their employees.

-

The Fed is making Real Progress on Inflation – Richmond Fed President

That is always a good sign.

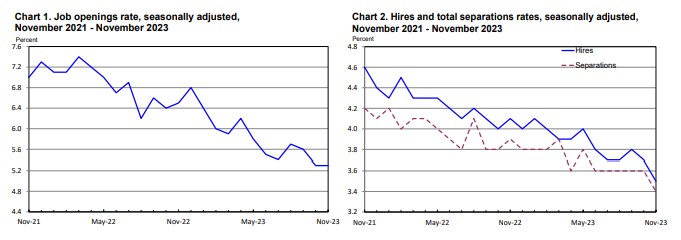

The JOLTS report had a decline from 8.85M to 8.79M slightly below market expectations.

JOLTS is the Job Openings and Labor Turnover survey. This is one of those leading indicators of future employment and employer retention.

Instead of just looking at the Unemployment rate, it covers everything from Vacancies, separations, voluntarily quitting, layoffs and Discharge. The report also looks at deaths and retirements.

For reference the Job Openings at 8.8M is down from the high of 12.0M March 2022.

This is a survey of more than 20,000 businesses and government offices. The takeaway is a strong labor market with employers holding on to their employees.

-

Good morning 2024, the Sun is shining.

The Jobs reports are coming out on Thursday and Friday. These include the ADP, JOLTS, and BLS Reports.

We will also be receiving the Fed Minutes from the December 13th meeting. What is important is that this is when Powell pivoted. We anticipate the Fed cutting rates in March but not sooner.

I am optimistic about 2024 and look forward to the challenges and successes.

“Homebuying Demand Shows Early Signs of Rebound. Declining mortgage rates and a double-digit increase in new listings are bringing house hunters off the sidelines.” – Dana Anderson – Data Journalist

-

It was nice knowing you 2023

In 2023, the Lenders, Realtors and Consumers has demonstrated remarkable resilience and adaptability. Despite various economic challenges, our industry has shown a positive trajectory with lower mortgage rates, encouraging both potential homebuyers and existing homeowners to explore opportunities.

Overall, the positive trends are poised to continue in 2024.

I am looking forward to 2024 and beyond. Be safe this weekend and I will see you on the other side.

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.