-

PPI is up, Jobless Claims are Down So what’s a Bond to Do?

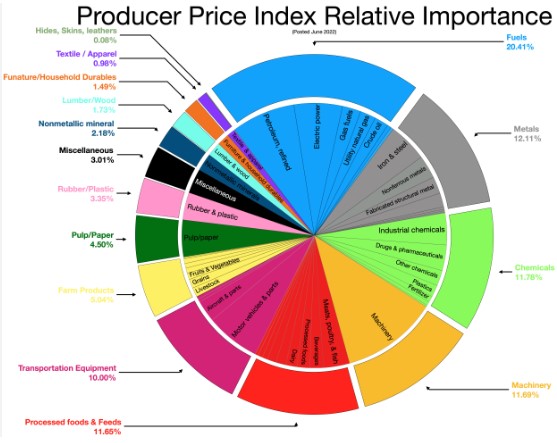

Producer Price Index was slightly hotter than expected. This is the cost of the producer to produce goods and services. A preamble to the Personal Consumption Expenditures (PCE) due out 27th of November.

Initial Jobless Claims are down for the first time as well as Continuing Claims.

The Bond Market is just not sure what to do with itself.

Rates increased the last two weeks and are not budging off those levels.

We will see how this all shakes out the next two months.

Check out this graph—it’s so detailed you’ll need a microscope just to find the title!

-

Inflation report came in As Expected. This is huge.

Mortgage rates have taken a beating in recent weeks, so this bit of good news—or at least no bad news—is welcome.

The October Consumer Price Index (CPI) report showed overall inflation rose by 0.24%, with the annual rate ticking up slightly from 2.4% to 2.6%. Two main factors driving this increase were a surprising 2.7% rise in used car prices and, as expected for the holiday season, higher airline fares.

Meanwhile, mortgage applications dropped 6.8% as rates climbed to an average of 6.84%. However, purchase applications specifically rose by 1%, which is encouraging news.

We do soft credit pulls for mortgage pre approvals.

-

Bonds are up, Nope their down, oh sorry up again….

The bond market, particularly mortgage-backed securities, has been on a wild ride over the past three weeks.

Take a look at the graph below: remember, an upward movement indicates lower rates. We’ve seen significant losses since September, and while there was a bit of a rebound last week, most of those gains slipped away this morning.

This chart represents about a 0.75% rate shift.

The economy, meanwhile, continues to perform exceptionally well, with unemployment holding at historic lows and inflation hovering close to the Fed’s target. Yet, mortgage rates remain stubbornly unpredictable.

-

It’s Fine, I’m Fine, Everything is Fine.

ADP Employment Report was double the expectations. It is seasonally adjusted but much higher than anyone expected.

Friday is tech BLS Report will have more detail and actual numbers.

Small Businesses with fewer than 50 employees are not seeing job growth. which is better than the decline the last four months.

GDP Q3 shows economy grew by 2.8%, we expected 3.0%. PCE numbers tomorrow.

Lots of acronyms today sorry about that, trying to keep this post short and sweet. Bottom line is the bond market is confused and the election is next week.

Next two days will dictate the direction of the market specifically the Bond market. My suggestion: Lock’em if the Got’em.

Art work by Brazilian cartoonist Henrique de Souza Filho

-

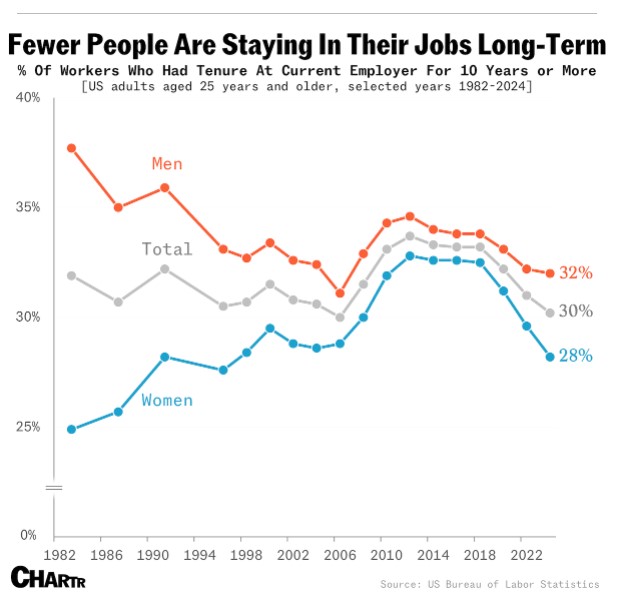

Quit Rate Remains at 1.9%. Very telling.

Understanding the Quit Rate and Economic Indicators

The quit rate is the rate at which employees voluntarily leave their jobs. When this rate remains low for an extended period, it often signals that fewer people feel confident about finding new employment opportunities.

The latest Job Openings and Labor Turnover Survey (JOLTS) showed that job openings fell by 557,000, 7% below the anticipated 8 million. This aligns with the low quit rate, indicating a potential cooling in labor market confidence.

In other economic news, oil prices have dropped to $67 per barrel. This decline is beneficial for inflation, as oil is a key input in both manufacturing and transportation.

Despite these developments, the bond market has shown strong reactions over the past two weeks, pushing interest rates to their highest level since July. This may seem counterintuitive given recent economic data, yet bond markets are influenced by complex factors, including inflation expectations and Federal Reserve policy.

Finally, the Conference Board’s Consumer Confidence report showed a rise from 99.2 to 108.7, the highest level since January, signaling improved consumer sentiment.

-

Durable Goods And a quick look at next week.

What’s interesting about Durable Goods Orders, yes I guess I just said that but seriously it’s a thing.

Durable Goods are items with a lifespan of over three years—think of dishwashers, ovens, stoves, and cars. Interestingly, there’s been a shift in demand since the pandemic, with many people investing in home remodels and repairs. The trend is clear in the graph below.

Part of the inflationary pressure we’re seeing is due to demand outpacing supply, shown by the red line in the chart.

In September, durable Goods Orders declined by 0.8%, largely because of slower auto sales. However, when excluding autos, core durable goods orders actually rose by 0.5%.

In short, despite the constant stream of negative news, the economy is still moving forward.

Next week its all about Jobs reports and our infamous Personal Consumption Expenditures (PCE).

Mortgage Rates are starting to take back some of the losses over the last week. We feel good about the direction and anticipate lower rates moving forward.

-

It feels like a Hurd of Turtles stampeding through peanut butter. And what’s a Beige Book?

“It feels like we’re just running in place,

More homes for sale, yet stuck in the race.

Rates in the sixes, a welcome descent,

Better than last year’s eight percent.But still we stand, no forward pace,

Caught in a cycle, in the same space.

The numbers shift, but the story’s the same,

Chasing a change that never quite came.“At 2:00pm ET the Federal Reserve will release their Beige Book. Think of it as an economic health update on each of the twelve districts.

This gives us an insight of what the Fed members are thinking beyond the BLS Jobs report. They will check on the strength against their business contacts and what they are saying.

-

If the Feds are cutting their rates, why are Mortgage rates higher?

Since the Fed has cut rates 50bp on September 18th, 30-year mortgage rates have risen by roughly 0.75%.

“But why? I thought the Mortgage rates were tied to the Fed rate”

When the Fed cuts rates it has specific impact on these and more:

- Money Market accounts

- Short term Treasuries

- Credit cards

- Car loans

- Personal loans

- Small Business loans

What you don’t see on the list is mortgage rates, which are tied to Mortgage-Backed Securities (MBS) or, more specifically, the 10-year Treasury bond.

The Federal Reserve’s actions encourage money managers to buy bonds now, anticipating future rate cuts. For instance, a bond purchased today might offer a 10-year Treasury yield of 4.18%, guaranteed, as opposed to waiting until next year when rates could be 1.50% lower due to the Fed’s reductions.

It’s a delicate balance, and historically, October tends to be a challenging month for mortgage rates.

I was considering adding a more technical bond chart, but then I thought, why not a picture of a cute cat instead? And after some more thought, I figured, why not go with something more personal—a bit of a self-portrait, in a way.

-

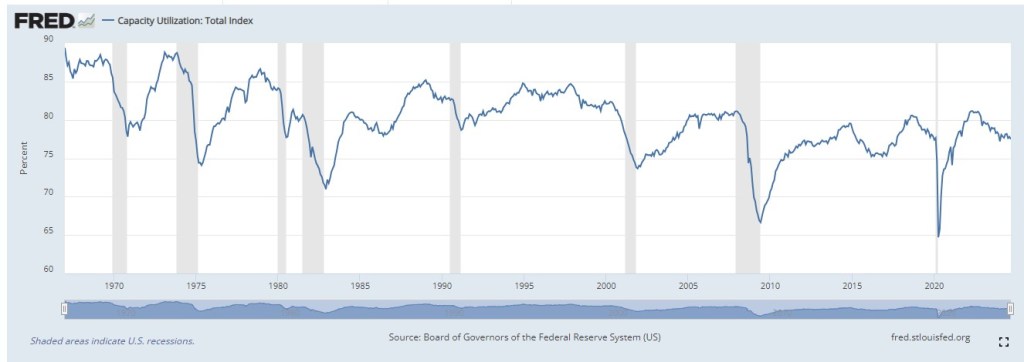

How Does Production Capacity Utilization give us insight… I bet you were thinking the same thing!

Production Capacity Utilization simply refers to how much a company or industry can produce versus how much they are actually producing.

When production is at full capacity (100%), prices tend to be higher because demand is strong. During the 2008 financial crisis, production utilization dropped to 60% due to weaker demand.

Currently, we are at 77.5%, the lowest since January. While it’s not a bad number, it suggests production is slowing down, and manufacturers are reducing prices to encourage sales.

As a result, prices are falling and are expected to continue dropping, which could bring inflation below 2% sooner, leading the Federal Reserve to lower interest rates.

Graph below shows the hills and valleys over the last 50 years.

-

Don’t Stop! Run through the Tape.

Fed Governor Waller has three possible projections with regards to the economy.

- Economy Stays strong, inflation nearing Fed’s target and unemployment only ticks up slightly. Fed continues with rate cuts.

- Inflation falls materially below 2% for some time. Labor market significantly deteriorates. Fed would suddenly be behind the curve and have to cur rates more aggressively.

- Inflation picks up again, labor market improves. The Fed can pause rate cuts.

The Feds next meeting in November 7th. At that point the Fed will have a lot of data to chew on including the October 31st Personal Consumption Expenditures (PCE).

What this means is the Feds will continue to cut rates unless something extraordinary happens. We have seen tremendous improvement with interest rates and expect that to continue.

If you are on the fence either buying or selling, lets keep pushing forward and run through the tape.

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.