-

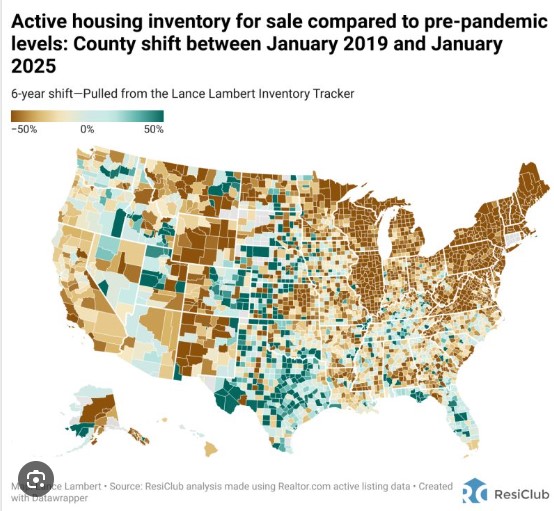

Supply is Not keeping up with Demand. Inventory up 16.8% but not good enough.

Let’s go to our way-back Machine, lets say back to 2022 when the inventory was below 500,000. Pre-Covid numbers averaged closer to 1.4M. currently we are at 1.18M.

We have a 3.5 months’ supply of homes up from 3.2 in December.

Median home price was $396,900 down slightly from December. 28% first time home buyers, 29% cash – down from 32%.

Housing market staying strong as inventory try’s to keep up.

Have a great weekend. ww.YourApplicaitonOnline.com

-

Fed at Net Neutral and QE, QT explained.

I’m sure that got your undivided attention – Not…

But its important and why the rates may actually start dropping.

Quantitative Easing (QE) is when a central bank injects new money into the economy by expanding the money supply. Think back to the 2008 financial crisis and the COVID-19 pandemic—during these periods, the Fed was aggressively pumping money into the system.

Quantitative Tightening (QT), on the other hand, is the process of reducing the money supply. The Fed has been shrinking its balance sheet for years, which has contributed to rising Fed rates and mortgage rates.

Net Neutral is exactly what it sounds like—neither QE nor QT. It’s a steady-state monetary policy where the Fed maintains the status quo without expanding or contracting the money supply.

This is a big deal. Net Neutral is the next step to QE and lower interest rates.

We’re starting to see a shift toward a buyer’s market, as evidenced by the increasing number of listings being pulled. After years of rapid home value appreciation, prices have leveled off and are beginning to normalize. Sellers are catching on, reassessing their pricing strategies, and either adjusting their listings or temporarily stepping back from the market.

http://www.YourApplicationOnline.com

-

FED Speak and they seem to be reading from the same playbook.

Fed Pres Harker, Fed Governor Waller and Fed Pres Bullard all seem to be reading from the same book.

They are all saying, January was not a surprise historically and not overly concerned with potential tariffs.

The NAHB Home Builder Sentiment Index dropped 5 points due to concerns over tariffs, mortgage rates, and rising housing costs—particularly with Canada, which supplies about 30% of our soft lumber.

Housing starts and permits have declined, but only relative to December’s numbers. The key factor in December? Lower mortgage rates. And it wasn’t even a significant drop—just the expectation of lower rates was enough to drive demand.

Now, imagine what will happen when rates actually decline in a more sustained and meaningful way.

-

Don’t play Chess on a Checkerboard.

Regardless of your skills, using the wrong strategy or approach for a given situation is dangerous.

Fed Governor Waller spoke yesterday with a dovish tone, downplaying the significance of January’s inflation data, attributing it to historical anomalies and seasonal factors despite its unusual magnitude.

He also expressed little concern about the impact of tariffs on inflation, characterizing them as a one-time price adjustment rather than a driver of sustained inflationary pressure.

I disagree. Waller is playing Checkers on a Chessboard not the other way around. Time will tell and I hope he is right.

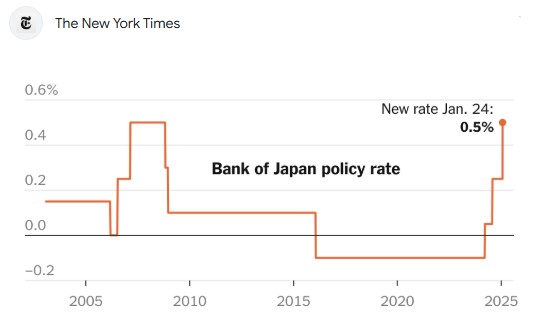

We are watching Japan and their unexpected kike of their central bank rate. Highest since 2009.

Rates are still holding onto gains the last week.

http://www.YourApplicationOnline.com

-

Knowledge is knowing that a tomato is a fruit, Wisdom is knowing not to put it in a fruit salad.

Stocks and Mortgage Bonds are trending higher today. As a reminder, bond prices and yields have an inverse relationship (consider that my Valentine’s plug)—when bond prices rise, yields fall, and interest rates follow suit.

January’s Retail Sales report came in weaker than expected, declining 0.9% versus the anticipated 0.1% drop. This suggests consumers may be reaching their spending limits. Historically, post-holiday spending slows, but this decline is more significant than usual.

Want to get big corporations’ attention? Use the most powerful tool you have—your wallet. Hold onto your money, and they’ll come running back with lower prices.

Lower Prices, lower Inflation, Lower Rates.

http://www.YourApplicationOnline.com

-

I feel like a Rubber Band being pulled in 5 different directions.

Bonds rebounded today after struggling in response to yesterday’s challenging CPI report. Meanwhile, the Producer Price Index (PPI) largely met expectations.

The PPI measures changes in the cost of goods and services at the production level in the U.S., reflecting what businesses pay to produce items. This contrasts with the Consumer Price Index (CPI), which tracks the prices consumers pay for those same goods and services.

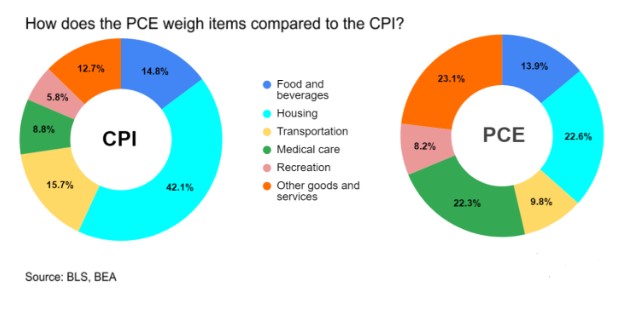

The big report coming at the end of the month is the Personal Consumption Expenditure (PCE) which is the measure of how much money households spend on goods and services.

PPI reflects the cost of producing a basket of goods and services, whereas PCE measures what consumers actually purchase from that basket.

Clear as mud, right?

The bottom line: We regained yesterday’s losses, but the ride remains anything but smooth.

http://www.YourApplicationOnline.com

-

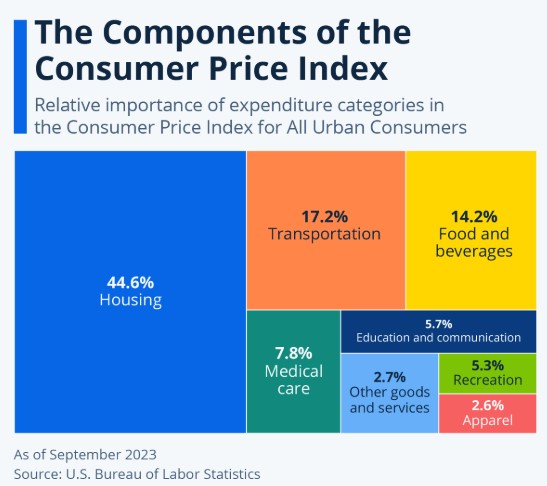

CPI why you do me dirty.

The January Consumer Price Index (CPI) increased by 0.5%, exceeding the 0.3% estimate. Overall inflation ticked up from 2.9% to 3.0%.

This is bad news for the bond market. Even the Core CPI, which excludes food and energy, rose by 0.4%—twice the expected increase.

At 1:00 p.m. ET, a 10-year Treasury Note auction will take place. Strong demand, given the higher yields this morning, could offer some relief.

For now, the damage is done—we just have to move forward.

http://www.YourApplicationOnline.com

-

Once you’re inside the cannon – There is only one way out!

Federal Reserve Chair Jerome Powell stated that the economy remains strong overall and has made significant progress toward the Fed’s 2% inflation target over the past two years.

Powell receives inflation data a day in advance, meaning he has already seen tomorrow’s report. His optimistic tone suggests encouraging news ahead.

In January, fewer small businesses reported raising prices, and even fewer plan to do so in the future.

Meanwhile, wage increases slowed to a four-month low, signaling easing inflationary pressure. With less extra cash in circulation, consumer spending may cool, giving businesses more reason to stabilize prices.

Stay patient—the path forward is becoming clearer, and the light at the end of the “Cannon” is coming into focus.

http://www.YourApplicationOnline.com

-

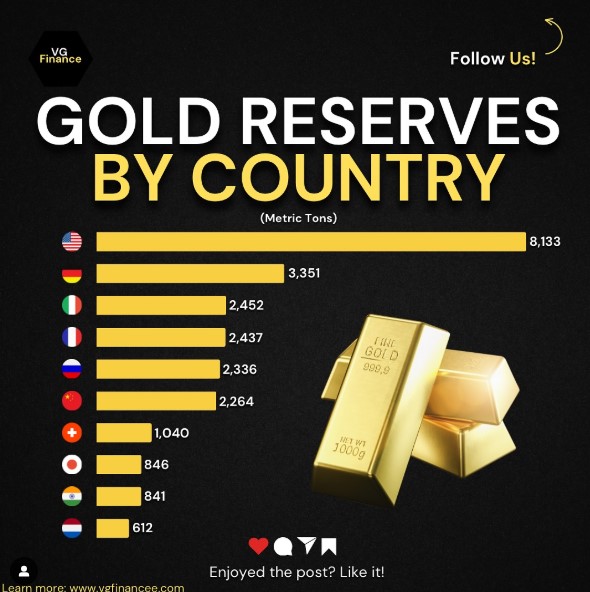

Instead of water, I put redbull in the back of my coffee maker. I was halfway to work before I realized I forgot my car.

Now that we’re all awake and recovering from the commercials—I mean, the football game—let’s talk about gold.

According to the U.S. Treasury Department, the book value of the gold held by the government is approximately $42.22 per troy ounce, while the market value stands at $2,900.

If the government were to revalue its gold reserves, it could reduce the need to issue Treasuries. And a lower Treasury supply? That’s good news for interest rates.

We expect rates to continue their slow ride down though bumpy. Get out their and start looking at homes. Contact your agent, contact us and lets get to getting.

http://www.YourApplicationOnline.com

-

I Offer you a Lifeboat and you picked up a Violin.

The BLS Jobs Report is a revisionist’s dream. January job estimates were originally 170,000, but the actual number came in at 143,000. However, revisions for November and December added 100,000 jobs, shifting the narrative.

Average hourly earnings rose 0.5% in January, triggering a strong reaction from the bond market— and not in a good way. Higher earnings mean more money to spend, which fuels inflation concerns.

But looking deeper, there’s a key detail being overlooked: average weekly hours worked declined from 34.3 to 34.1 in January.

What’s frustrating is that the headlines paint one picture, while the real story lies in the details— details the media and bond markets seem eager to ignore.

Rates have improved over the past few weeks and we think this BLS Blip is just a Blip and the bond market will adjust.

http://www.YourApplicationOnline.com

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.