-

What’s a Corporation to Do? Raise Prices Only on Tariffed Goods—or Across the Board?

Corporations typically focus on maintaining profitability, so while they can raise just the prices on tariff-impacted goods, they often take a broader approach. Here’s how it usually breaks down:

- Direct Tariff Pass-Through: Companies may increase prices only on products directly affected by tariffs, especially if those items are clearly traceable to specific materials or imports (e.g., a particular electronics part or imported steel).

- Blended Price Increases: Many businesses choose to spread the cost of tariffs across a broader range of products. This avoids sharp spikes on a few items and softens the blow to consumer demand—basically, hiding the increase across a wider product line.

- Strategic Price Hikes: Some corporations take advantage of tariff news to raise prices on unrelated items under the cover of “inflationary pressures” or “supply chain disruptions.” This can quietly boost margins.

So, while they could limit price increases to just tariffed goods, in practice, companies often raise prices more broadly—especially if the market will bear it.

The Feds meet this afternoon to talk rates. The challenge is uncertainty with regards to inflation.

http://www.YourApplicationOnline.com Soft Credit Pull

-

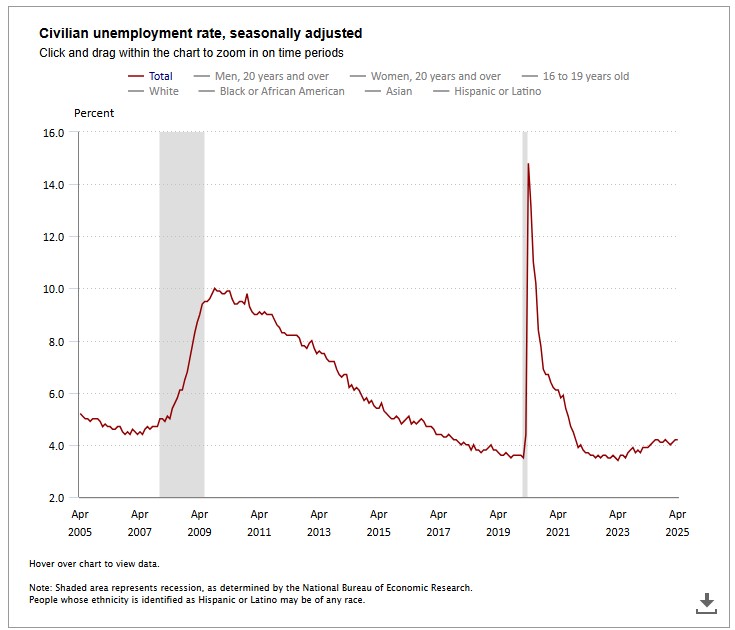

The Relationship of time Unemployed and the Unemployment Rate.

Unemployment benefits currently extend up to 26 weeks. The share of individuals unemployed for 27 weeks or more has increased from 21.3% to 23.5%—the highest level in three years. This means nearly one in four unemployed workers are no longer eligible for benefits, adding further strain to the economy.

Additionally, the median duration of unemployment rose to 10.4 weeks, up from 9.8 weeks, indicating a broader slowdown in job recovery.

Current Unemployment rate remains at 4.2% but we see a reasonable scenario where the rate rises to 4.4 to 4.5%. The Feds cannot ignore the obvious signs of a slowing economy.

Translation; Mortgage Rates will drop.

Website http://www.YourApplicationOnline.com soft credit pull.

-

It’s like Opening a Can with no Label. You don’t know what you’re going to Find.

Imagine reaching into your pantry and pulling out a food can with no label. No ingredients, no expiry date, no clue what’s inside. It could be soup, peaches, or dog food — you just don’t know until you open it. That’s what tariffs can feel like in the economy.

When tariffs are imposed, especially suddenly or unpredictably, businesses and consumers are left guessing. Will prices go up? Will supply chains break down? What country will retaliate next? It’s like opening that mystery can: you’re not sure what you’re going to get, but you know it might not be good.

Tariffs are meant to protect domestic industries, but they often come with unintended consequences — higher costs, limited choices, and economic uncertainty. For small businesses and everyday families, that uncertainty can make budgeting, planning, and even grocery shopping feel like a gamble.

In the end, whether it’s dinner or a policy decision, people like to know what they’re getting into. With tariffs, as with unlabeled cans, a little transparency could go a long way.

Rates are holding steady. OPEC+ is increasing their production by 411,000 barrels per day roughly 1% of total production. Potentially lowering gas prices and helping inflation.

Lets get you or your clients pre-approved. http://www.YourApplicationOnline.com Soft Credit pull.

-

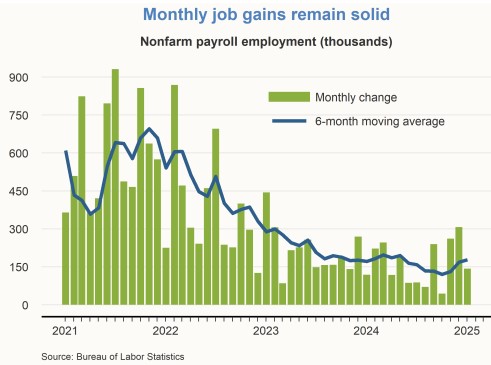

Jobs Reports but Revisions ensue. Why is it so difficult to get this number right and why is it always revised lower?

BLS Jobs reported 177,000 jobs created in April expectation was 130,000, but March and February revies down over 58,000. Aprils report will have the same revision next month.

The market understands this and is why the stock and bond markets did not reacted as you might expect.

Sample Survey: The Bureau of Labor Statistics (BLS) uses a sample survey to estimate job growth, which means the initial numbers are based on a subset of businesses and may not perfectly reflect the entire economy.

Incomplete Reporting:The initial report relies on data from businesses that respond quickly, but some businesses may not report in time for the initial release.

Annual Benchmark Revisions:Once a year, the BLS revises the monthly data to align with more comprehensive administrative data from Unemployment Insurance programs, which provides a more complete picture of employment.

Revised Estimates:When businesses not initially included in the sample provide data, the initial estimate may be adjusted downward if the change in employment for those businesses is different from what was initially reported.

Bottom line: take it with a grain of salt. Rates remain persistently in the 6% range on average. While that marks progress compared to last year—when rates were in the 7% range—it’s simply not improving as quickly as we’d like.

http://www.YourApplicationOnline.com Soft Credit Pull

-

American Economic $8T Export Colonization you are not aware of.

While trade data provides valuable insights, it does not capture the full scope of the U.S. economic footprint abroad. U.S. exports combined with affiliated sales from American companies operating internationally amount to over $8 trillion.

The United States leads the world in what can be described as economic export-driven influence. Consider the global presence of companies like Starbucks, major fast-food chains, and U.S.-based manufacturers with local operations overseas. Firms such as Ford, Intel, Apple, and Nike exemplify this expansive reach.

Although there is a desire to bring more manufacturing back to the U.S., tariff structures often hinder such efforts. As a result, many companies strategically establish production facilities in foreign markets—particularly in Europe—to mitigate the impact of trade barriers.

Moreover, American software giants like Microsoft continue to drive international economic influence through widespread software licensing and services.

Global trade is highly complex, and focusing solely on a $1 trillion trade deficit oversimplifies the situation. U.S. companies excel at leveraging global markets, showcasing a powerful model of economic engagement that extends well beyond traditional trade statistics.

http://www.YourApplicationOnline.com soft credit pull no harm

-

The Dust needs to settle before we can see what the numbers really mean.

A Mixed Bag of Economic Data Leaves Markets Guessing

The latest Personal Consumption Expenditures (PCE) data surprised to the upside, with headline PCE rising 0.7% in March—beating the 0.5% forecast. Incomes also rose more than expected, up 0.5% versus the 0.4% estimate, signaling continued consumer strength. Encouragingly, the Core PCE, the Fed’s preferred inflation gauge, eased to 2.3% year-over-year, down from 2.7%, offering a glimmer of hope on the inflation front.

However, the broader economic picture remains cloudy. Q1 GDP came in at -0.3%, marking the second consecutive quarter of negative growth—technically meeting the definition of a recession. Meanwhile, headline PCE inflation for the year jumped 3.7%, above the 3.1% forecast, keeping inflation concerns alive.

On the labor front, the ADP Employment Report showed just 62,000 jobs created in April—well below the 120,000 expected—adding to the uncertainty.

So, what does all this mean? It’s hard to say. Q1 data was likely distorted by pre-tariff stockpiling and global hedging strategies, making it difficult to read true underlying trends.

The bond market is caught in the crossfire of mixed signals. On one hand, softer job numbers and cooling core inflation support lower rates. On the other, rising headline inflation and whispers of foreign central banks, like China, reassessing their U.S. bond holdings could push yields higher. It’s a tug-of-war with no clear winner—at least for now.

http://www.YourApplicationOnline.com soft credit pull

-

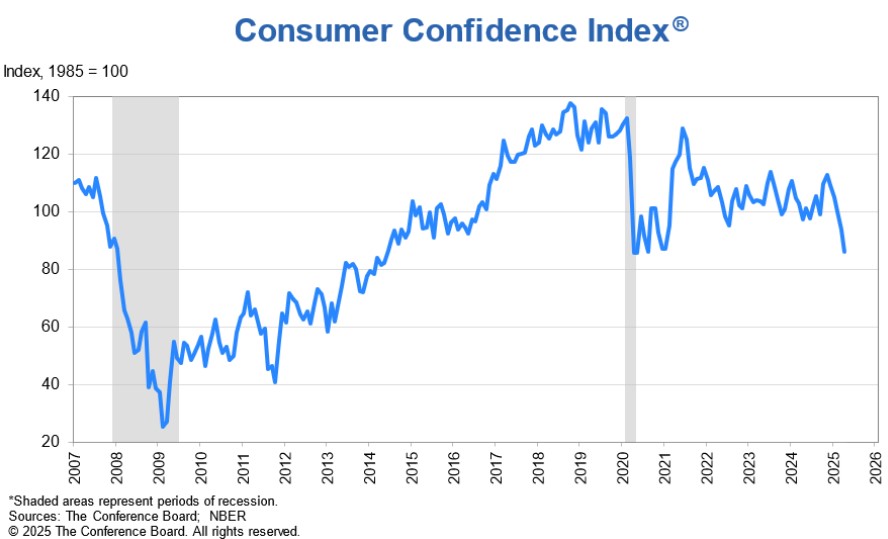

Consumer Confidence fell from 92.9 to 86. But lets look historically.

But what does this really mean? The last time we saw this level was between 2020 and 2022. This figure is heavily influenced by business conditions, employment prospects, and expectations for future income.

Historically, recessions are typically marked by readings below 80.

The March JOLTS report shows job openings declined from 7.49 million to 7.19 million, indicating clear signs of weakness in the labor market. Additionally, the quits rate — which reflects the number of people voluntarily changing jobs — remains at its lowest level since 2015.

Year-over-year, home prices have increased by 3.9%. While some regions have experienced slight declines, the overall housing market remains strong and resilient.

We anticipate continued improvement in interest rates, making this an excellent opportunity for buyers to enter the market before conditions shift.

http://www.YourApplicationOnline.com soft credit pull Nation wide.

-

How long does it take for a Ship to travel from China to the US? 60 days…

When will the impact of tariffs start to show? Mother’s Day (happy early Mother’s Day this Sunday!) marks the 60-day point.

It wasn’t that long ago that we began stockpiling toilet paper and paper towels. Why those two items resonated so strongly with consumers isn’t entirely clear — perhaps because they are some of the most personal essentials we use daily.

While the supply chain impact likely won’t be as severe as it was during COVID, it could still affect container unloading, transportation, and manufacturing. This disruption could also lead to a rise in the unemployment rate.

The Federal Reserve remains focused on inflation, and this situation adds to their concerns. However, on the other hand, lower rents are starting to be reflected in both the CPI and PCE reports, providing some balance.

lets get you or your clients pre-approved, Soft credit pull

http://www.YourApplicationOnline.com

-

When Negative is Positive (But Not for Everyone) A Poem for Your Friday Morning

Let’s Talk Q1 GDP

The street says growth, but just a trace,

Point four percent—a sluggish pace.

Atlanta Fed? A different view,

Negative four—they say it’s true.

A downturn looms, the signs align,

We’ll know for sure come Wednesday’s time.PCE Arrives Next Week

March numbers land, but here’s the twist,

No tariffs yet in this data list.

Inflation’s pace is set to slide,

To two-point-two on the headline side.Jobs in Focus: A Labor Round

JOLTS and ADP come around.

The BLS report will also show

If jobless trends begin to grow.

April’s the frame, with DOGE in play,

And tariffs felt in the laborway.

Unemployment may hold the line,

At four-point-two—or worse this time.What’s bad for him may good things do,

A downturn comes—what’s that to you?

Recession stirs a fearful flight,

To bonds where money sleeps at night.When markets shake and yields are sought,

The bond world warms, the rates grow not.

So while the storm may cloud the skies,

For buyers now, low rates arise.http://www.YourApplicationOnline.com

-

Lets talk Homes. Not Holmes who was a great boxer. Inventory, Median sales price…

- Existing home Sales fell 5.9% Expectation 3.3%

- Median Home Price rose 1.7% to $403,700

- Inventory rose 8.1% to 1.33M up 20% from last year.

- 4-months supply. 3.5% higher than February.

- Home on market 36 days on average down from 42 days.

- First time home buyers 32%, Cash buyers 26% investors 15%

With that out of the way, it’s a mixed bag of solid and slightly surprising numbers. Home prices remain strong, largely due to historically low inventory levels.

In fact, inventory is still hovering near its lowest point in 26 years—below even the pre-pandemic norms from 2015 to 2020.

So get out there and buy a home—strike while the iron’s hot!

http://www.YourApplicationOnline.com soft credit pull nationwide

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.