-

Supply and Demand, the Global Bond Market — one big happy family… and a Where’s Waldo picture.

Japan’s weak Treasury bond auction is casting a shadow over upcoming debt sales next week. Lower demand typically means higher yields — and that pushes rates up.

Meanwhile, the UK surprised markets with hotter-than-expected inflation. Investors were expecting a drop, but instead, the 10-year gilt yield moved higher.

Since we’re all part of a globally connected bond market, U.S. yields are rising in sympathy — though the reaction here has been relatively muted.

As for the nine Fed members who spoke yesterday, they focused on rising unemployment, persistent inflation, and ongoing uncertainty around tariffs.

No indication of a Fed rate drop just yet.

http://www.YourApplicationOnline.com soft credit pull

-

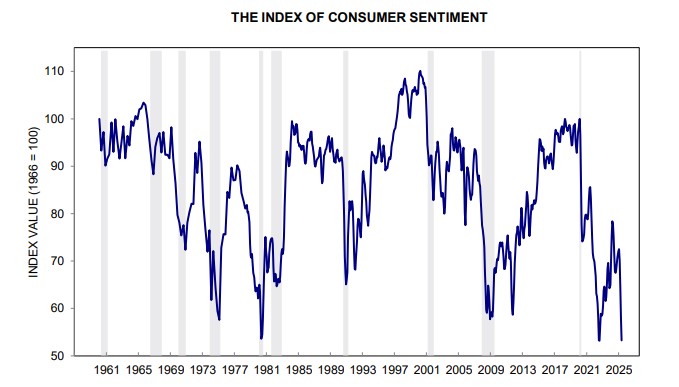

Let’s pull the Band-Aid off and pull up our bootstraps.

The University of Michigan reported that Consumer Sentiment fell to 50.8% in May, the second lowest reading since 1952 hen the tracking metric started.

Consumers expect inflation to rise to 7.3% over he next year.

Over 60% of respondents are expecting more unemployment over the next year.

To note: the survey was done prior to OK and China trade talks.

There will be 7 Fed speakers throughout the day. lets see what tomorrow brings.

http://www.YourApplicaitonOnline.com

-

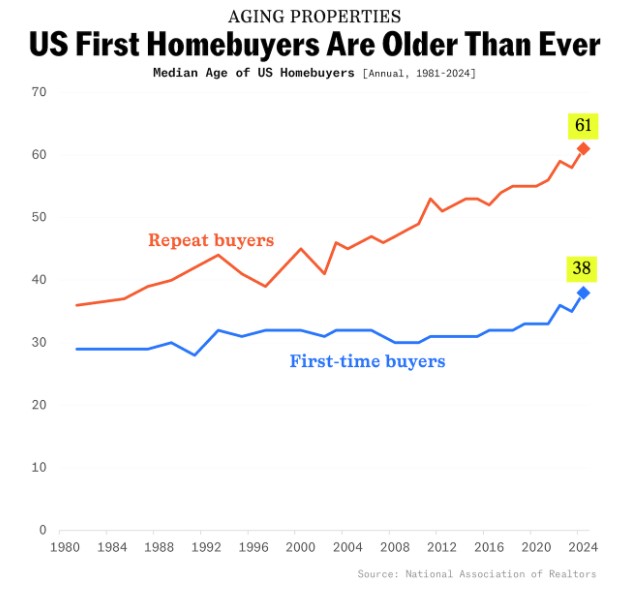

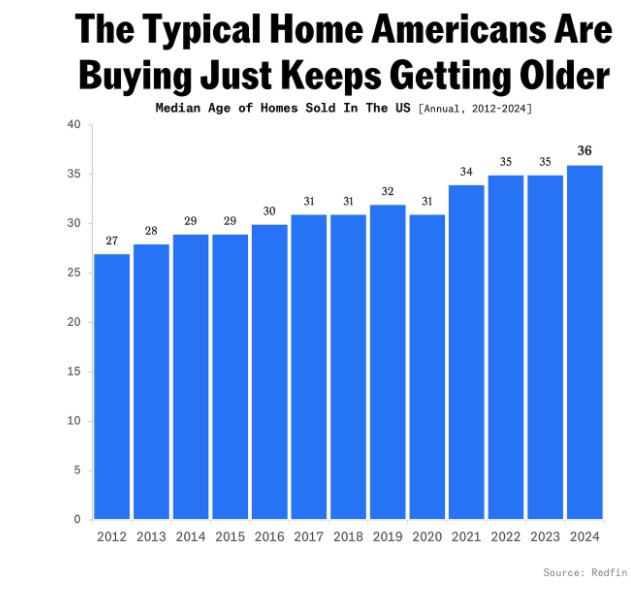

Moody’s put me in a bad Mood, but good news it’s Picture day…

Stocks and Bonds are both lower following news that US was downgraded by Moody’s Ratings this weekend due to US debt. The debt is 123% of GDP which is high compared to most other nations.

Rates are slightly higher this morning.

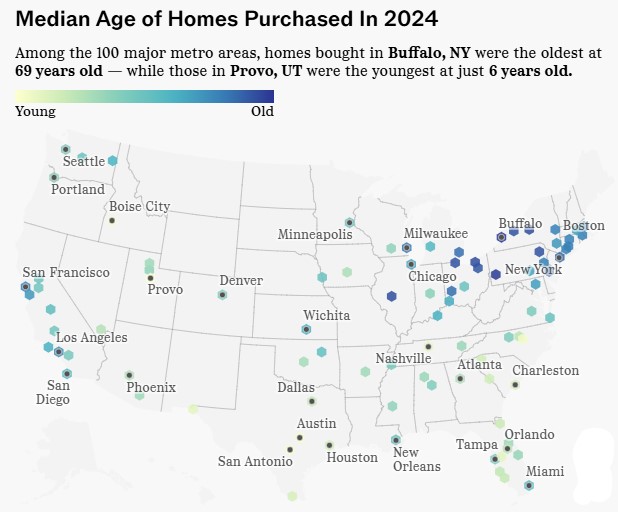

Interesting set of graphs below regarding age of buyers and homes across the US. Have a great week. http://www.YourApplicationOnline.com

-

What the Heck is a Bearish Engulfing Pattern, you may ask your self… Thanks Barry

In trading terms, a Bearish Engulfing Pattern signals the start of a downtrend, which often indicates lower interest rates. To visualize it, think of a “V” shape: you slide down to the bottom, then quickly swing back up.

The image shows it best. We see this all the time but what is different is it comes off the heals of the PPI report yesterday and Japan’s GDP more negative than expected.

The global yields were lower in sympathy. Rates dropped.

Housing Starts and Permits

Housing Permits are forward looking indicator and its been trending lower. permits down 5%. Tariffs create uncertainty and builders are already on edge.

Housing Starts are a better read. They are relatively flat in April an annualized down 2%. Not a big drop.

Have a fantastic weekend and if any questions come up, feel free to reach out.

online mortgage application http://www.YourApplicationOnline.com

-

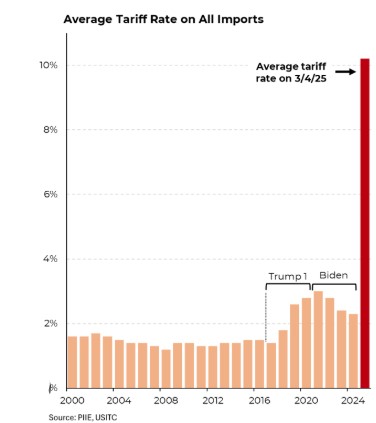

A Sponge can only hold so much Tariffs… I mean Water.

Walmart made a noteworthy observation, and the latest Producer Price Index (PPI) report backs it up.

While prices have remained relatively stable so far, Walmart pointed out that the full impact of the tariffs has yet to be felt at the consumer level.

The PPI data suggests that businesses are currently absorbing much of the cost, resulting in tighter margins. But that can’t last forever—eventually, those costs are likely to be passed on.

So even if inflation appears subdued for now, it’s clear that not all the pieces are in place. We haven’t herded all the cats into the barn just yet.

PPI came in at a negative 0.5% much cooler than the positive 0.2% expected.

Fed Chair Powell’s spoke this morning regarding reviewing their framework. Hum, not exactly sure what that means.

Inflation, Inflation, Inflation. the cure is worse than the disease. Lets drop the rates, restructure debt and let everyone take a deep breath. Just my opinion.

Let’s get you pre-qualified or your clients. http://www.YourApplicationOnline.com

-

Why do we keep pointing to the 10y Treasury Bond when talking rates? Trust me this is interesting.

The 10-year Treasury bond and mortgage rates are closely linked because:

- Both represent long-term borrowing costs.

- Both compete for the same pool of investors.

When the 10-year Treasury yield rises, mortgage rates typically increase as well. This is because:

- Lenders must keep mortgages attractive compared to Treasury notes, which are seen as low-risk investments.

- Higher Treasury yields signal that borrowing is becoming more expensive overall.

In response, lenders raise mortgage rates to:

- Stay competitive with Treasury investments.

- Ensure they offer returns high enough to attract investors.

In a nutshell:

Lenders add a “spread” (a percentage point difference) on top of the yield to account for the higher risk of mortgages compared to Treasuries.

The 10-year Treasury yield acts as a benchmark for mortgage rates.

Online Mortgage application http://www.YourApplicationOnline.com

-

CPI is like stepping on the scale after vacation—you’re hoping for good news, but deep down, you know that extra guac is about to show up in the numbers.

The April Consumer Price Index (CPI) showed overall inflation rising 0.2%, slightly below the expected 0.3%. Year-over-year, inflation edged down from 2.4% to 2.3%.

However, it appears the impact of recent tariffs hasn’t been fully reflected yet. Overall, inflation remains in a relatively flat range.

So what’s a Federal Reserve to do? Well do what they do best. Wait, and wait some more.

Here’s the problem: a huge chunk of homeowners are sitting pretty with sub-3.25% mortgage rates. And really, who wants to trade their cozy low-rate castle for an identical one at double the cost? Not many. Meanwhile, builders are grinning ear to ear—they’ve got brand-new homes with no rate baggage, and they know they’re the only game in town!

Ok, off my soap box and back to work. Lets get you or your clients pre-approved, soft credit pull http://www.YourApplicationOnline.com

-

Elvis was Abducted by Aliens. I found an old article.

This week’s key economic news includes the Consumer Price Index (CPI) and Producer Price Index (PPI), both set to be released Tuesday and Thursday respectively.

Expectations are for moderate readings, with tariff impacts only beginning to appear. A clearer economic picture has yet to emerge.

Stocks are higher with Mortgage Bonds lower after the US and China 90 day agreement.

Rates remain relatively flat, with the mid-6% range likely to be the norm for the foreseeable future. If you’re holding out for a drop in both home prices and interest rates, you may be waiting a long time.

Home prices continue to climb, with the exception of some more volatile markets—particularly in Texas and the Florida condo sector.

We’ll get more insight on Friday when the Housing Starts and Building Permits reports are released.

Online application http://www.YourApplicationOnline.com

-

Stocks and Bonds are like Siblings on a Road Trip

How a Trade War Can Hurt Bonds

A trade war can cause trouble for the bond market, mostly by pushing bond yields up and prices down. Here’s how that happens:

- Prices Go Up: Tariffs make imported goods more expensive, which can lead to higher inflation.

- Interest Rates Rise: To fight inflation, central banks may raise interest rates. Higher rates make borrowing more expensive and can hurt bond values.

- Less Foreign Buying: Trade tensions can scare off foreign investors, leading to lower demand for government bonds and even higher yields.

- Bonds Feel Less Safe: Normally, government bonds are considered safe during uncertain times. But in a trade war, confidence may drop, and investors might sell off bonds.

- Warning Sign of Recession: Trade wars can also lead to an “inverted yield curve,” where short-term bonds pay more than long-term ones—often a red flag for a coming recession.

-

70% of the US GDP is Consumer Spending. Spending is up but Consumers are scared.

The economy appears to be on stable ground—job growth remains steady, unemployment is near historic lows, and inflation is tracking at 2.4%.

But how is the average American consumer really feeling?

To answer that, we look at both hard data—like unemployment and inflation—and soft data, such as consumer surveys and sentiment polls. One widely used measure is the Consumer Confidence Index, which captures both current conditions and future expectations.

As of the end of April, the Present Situation Index stood at 133, significantly above the historical average of 103, indicating consumers feel confident about the current economy. However, the Expectations Index—which reflects outlook over the next six months—fell to just 54, marking its lowest level since 2011.

This stark contrast suggests that while consumers recognize today’s relative strength, uncertainty about the future is growing.

Mortgage rates holding steady. Lets get you pre-approved, soft credit pull.

http://www.YourApplicationOnline.com

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.