-

Is BLS BS? Garbage in Garbage out.

Speaking from my Engineering days, If the data collected is inaccurate, incomplete, or low quality (“garbage in”), any analysis, insights, or decisions made using that data will also be flawed or misleading (“garbage out”).

The Wall Street Journal article spoke to the staffing shortages at the Bureau of Labor and Statistics -BLS a U.S. Government agency hit by staffing cuts.

The BLS Report is utilized to calculate the inflation rate. These are actual people or statisticians going out and physically checking prices on groceries and other commodities. With less staff they have to guess or substitute.

Other Headlines:

- Challenger Job Cuts: Announced layoffs are up 80% compared to this time last year.

- Beige Book: Reports declining economic activity across several regions.

- Initial Jobless Claims: Increased by 8,000 to a total of 247,000.

My Take:

While these headlines may seem negative at first glance, they actually signal positive movement for interest rates. Slower job growth and economic softening tend to ease inflation concerns — a key focus for rate policy.With the BLS report due tomorrow, expectations are for a cooling labor market, marked by slower hiring and a potential uptick in unemployment.

If that plays out, we could see rates begin to trend downward — possibly meaningfully — as we move into summer.

http://www.YourApplicationOnline.com soft credit pull.

-

What does Deflation look like in real time. And Only 37,000 jobs created.

Those of us who’ve been around the block a few times — say, 12 years ago — remember what deflation looked like.

It was a magical time when:

- Steak night turned into “Hey, chicken’s great too!”

- That snack your kids love? Suddenly it was, “Let’s try something similar… and half the price.”

- Craving a soda? Congratulations! You’ve discovered the kitchen faucet — nature’s original soft drink, now with 100% fewer bubbles and all the hydration.

Deflation wasn’t just economic — it was a lifestyle.

The May ADP Jobs Report came in well below expectations, with just 37,000 jobs created versus the 115,000 forecasted. The sharpest weakness was seen among small businesses (1–49 employees).

In a notable detail, goods-producing businesses lost 2,000 jobs — a potential canary in the coal mine for broader economic trends.

My take:

If job growth continues to decline, we’re likely to see bond yields fall, which in turn puts downward pressure on interest rates. A softer labor market typically supports rate relief.Have a fantastic rest of your week and always feel free to reach out to our team. http://www.YourApplicationOnline.com.

-

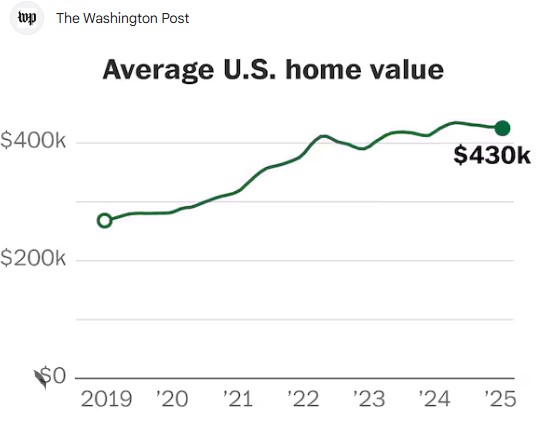

Just one year of 4% appreciation turns a $500,000 home into a $520,000 asset.

Your home (or future home) is a solid, appreciating asset.

- Home prices rose 0.6% in March.

- April data projects a 5.3% growth in home values over the next 12 months.

Job market highlights:

The Leisure and Hospitality sector saw a decline for the third consecutive month, removing 92,000 job openings in April alone.

Job openings increased by 191,000, reaching 7.39 million — well above estimates.

The quits rate fell to 2%, a historic low — indicating fewer people are confident enough to leave their current jobs.

Most new job openings came from the Professional and Business Services sector.

While the bond market moved in a rate-friendly direction, it’s clearly staying measured and reserved.

http://www.YourApplicationOnline.com

-

The Wealth Effect Cuts Both Ways: It’s Impact on Today’s Market and what’s up Redfin?

Not one to shy away from a clicky headline myself, but I think Redfin might be playing fast and loose with their math — or borrowing a calculator from a toddler.

They claim there are 1.94 million sellers and 1.45 million buyers… which sounds impressive until you remember that current inventory is 1.45 million, and about 500,000 of those are already under contract. That leaves just 960,000 active listings.

So unless we’ve entered a parallel universe where sellers are cloning homes or buyers are invisible, something doesn’t quite add up.

Front-Running and the GDP

There’s an old adage: “History is written by the winners.” In this case, we saw a spike in inventory driven by front-running — companies buying ahead of the anticipated tariffs.It’s a reminder that information is often presented by those in control, not necessarily those most affected. The GDP data may show a temporary boost, but it’s not always the full story — sometimes it’s just the version told by the ones holding the pen.

My Take

Tariffs impact more than just the cost of goods — they also weigh heavily on consumer confidence. The unpredictable, on-again/off-again nature of tariff policies creates uncertainty, which is never good for anyone — whether you’re a business owner or a consumer. Stability and clarity are key to sustained economic confidence.

http://www.YourApplicationOnline.com Soft Credit pull get qualified.

-

Inflation drops to 2.1%. Powell are you listening or still looking in the rearview mirror? Just asking.

A face-to-face meeting between Fed Chair Powell and the President — described as cordial at best.

We’re all hoping for mortgage rates to come down. Elevated rates are putting pressure on the housing market, keeping millions of homeowners locked into sub-3.25% mortgages and discouraging them from selling. This dynamic contributes to historically low inventory and, in turn, continues to push home prices higher.

At some point the cure is worse than the disease.

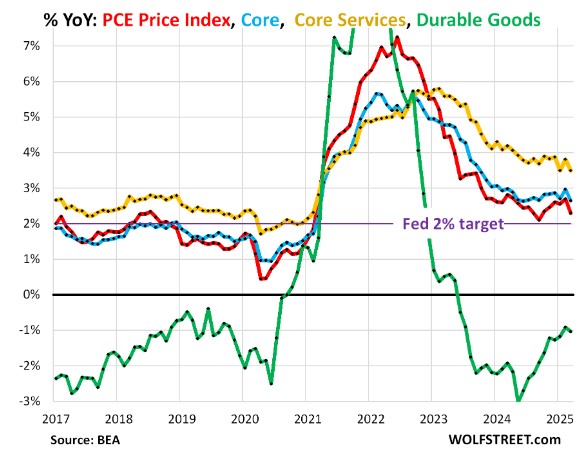

Personal Consumption Expenditures (PCE) rose 0.2% as expected

- Personal Consumption Expenditures (PCE) rose 0.2% as expected

- Incomes rose 0.8% expected as 0.3%

- Social Security payments rose 6.9%

- Trend for PCE continues to move down. Good News.

Have a fantastic weekend. we feel the tide shifting in the right direction.

http://www.YourApplicationOnline.com

-

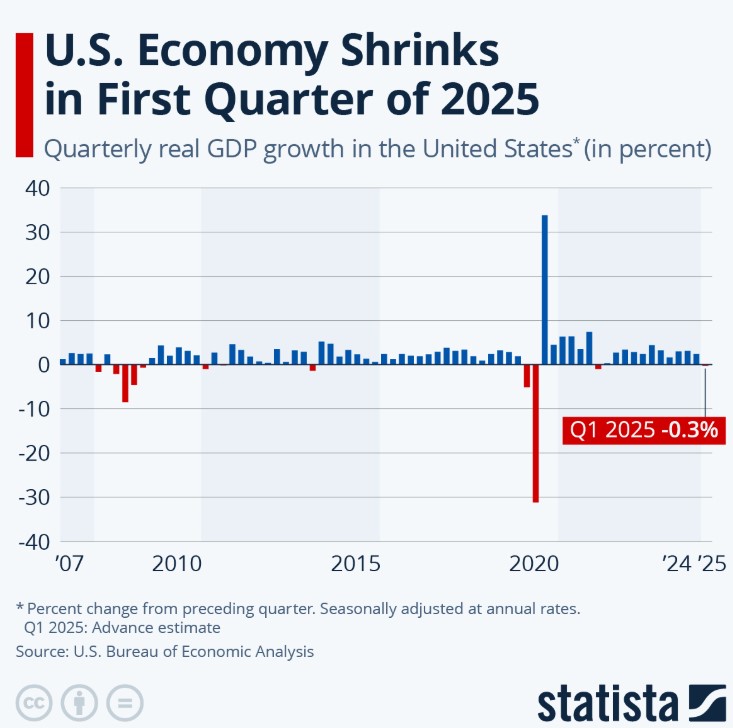

An interesting thing happened on the way to the Forum – grocery store. And Tariff reprieve

Q1 GDP came in at -0.2%, slightly better than the expected -0.3%, but still reflects a slowdown—particularly in personal spending, which rose just 1.3% compared to the 1.8% estimate.

This points to weaker consumer demand, which in turn eases pricing pressure. With fewer buyers in the market, retailers are often forced to lower prices to attract spending—ultimately helping to bring inflation down.

The power of the consumer at work.

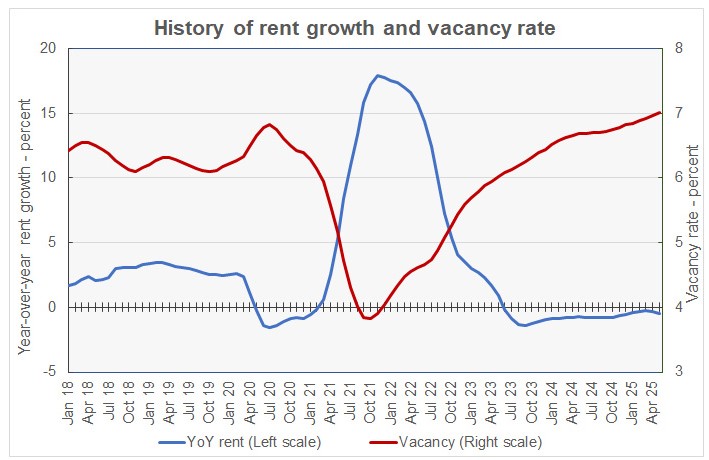

Another sign of slower consumer spending comes from the latest Apartment List Rent Report, which showed new rents rose just 0.4% in May, while rents are actually down 0.5% year-over-year.

This is especially notable because May is typically a peak season for rentals, when demand — and prices — usually trend higher.

Also worth noting: the national vacancy rate is holding at a historically low 7%, a key factor we haven’t touched on before.

The halt on Tariffs has had a positive impact not only to the stock market but the bond market as well.

http://www.YourApplicaitonOnline.com

-

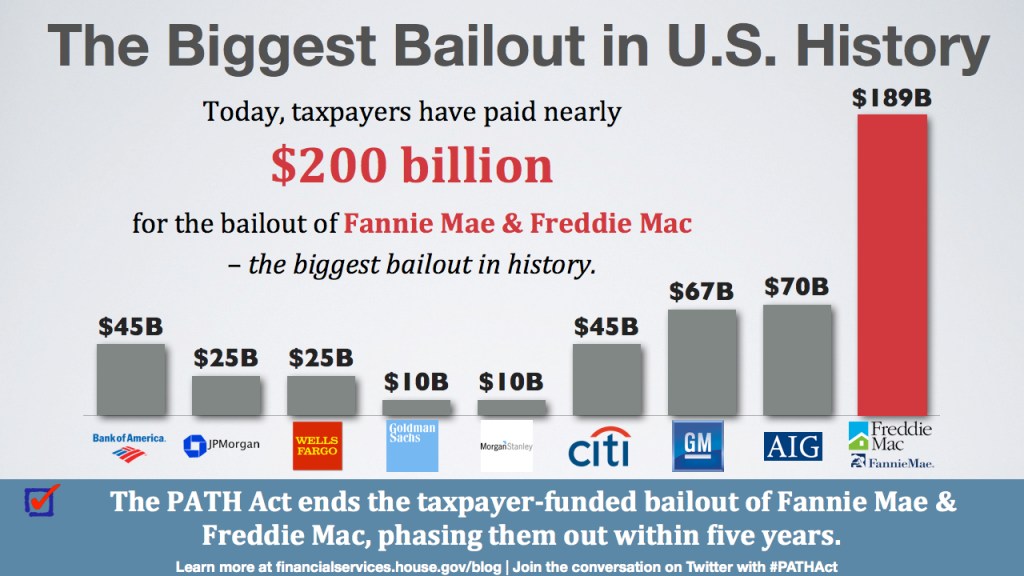

What Happens when Fannie and Freddie go Public? And my take.

With a new prospect of Fannie Mae and Freddie Mac exiting conservatorship and potentially going public has sparked both fear and excitement.

Lets do a quick breakdown:

Positive Impacts:

- Windfall for U.S. Government – recoup bailout funds from 2008.

- Increased Market Efficiency – market driven decision making, competition and innovation.

- Reduced Government Risk – shifting losses to private investors.

- Capital Market Benefits – raise capital and enhance their financial stability.

Negative Impacts:

- Increase in Mortgage Rates – Privatization to higher returns and higher rates.

- Reduced Access to Credit – impacts to less qualified borrowers with higher credit standards.

- Market Disruption – Government to Private is complex and disruptive.

- Financial Instability – if mismanaged could destabilize housing market.

My Take:

I lived through the 2008 financial crisis and saw firsthand both the positives and the pitfalls when Fannie and Freddie began competing with subprime lenders for market share.

It was a fun ride — until it wasn’t.

Healthy competition is a good thing, and this move has the potential to spark innovation and open up the marketplace. That said, with the government still retaining a degree of control, the guardrails remain in place — and that’s reassuring.

Soft credit pull. YourApplicationOnline.com

-

FNMA ie Fannie Mae rate forecast end of year 2026 5.875%.

Fannie Mae lowered their rate forecast for 2025 to 6.2% to 6.1% and for end of year 2026 from 6% to 5.8%.

There are more than 4M borrowers with rates over 7% right now so this is welcome news. We can get you pre-qualified and ready to go when rates start dropping.

Soft credit pull http://www.YourApplicationOnline.com

Housing report Case-Shiller

Home prices rose 3.4% year over year. What’s interesting is the big cities 10-20 city indices were higher nationwide, showing that big cities are outperforming. the 10-city index is up 4.8% with the 20-city up 4.1%.

Durable Goods Orders

Fell 6.3% in April but less than the -7.8% expected. Tariffs are the Culprit.

With summer just around the corner, I thought I would share a Disneyland pic from last year.

-

Remember the “Flight to Safety” blog I did? lets recap. And to those who Sacrificed and serviced our Nation.

Tariffs, tariffs everywhere — but not a drop to drink.

Tensions escalated with more talk of a potential 50% tariff on the EU, as trade negotiations continue to stall.

The stock market didn’t take it well and responded with a selloff. As usual, when equities take a hit, bonds often benefit. It’s the classic flight to safety.

We’re seeing a bit of rate improvement this morning as a result.

Consumer debt and breakdown:

- Mortgage Debt $13T

- Autos $1.6T

- Student loans $1.6T

- Credit cards $1.2T

- Total Household Debt $18.2T

http://www.YourApplicationOnline.com

-

Just Sold my Homing Pigeon on eBay for the 22nd time. Seriously let’s talk Debt Ceiling.

Let’s jump right in!

Yesterday’s weak 20-year Treasury auction led to a selloff in the bond market, which pushed mortgage rates higher.

We’re also seeing upward pressure on global yields, and Moody’s recent credit rating downgrade for the U.S. certainly isn’t helping the situation.

On top of that, the House just passed a new budget—essentially a tax and spending bill—which is making bond markets nervous. Why? More spending means more debt, and that translates to more Treasury issuance. The market has to absorb all of that.

Looking ahead, August is shaping up to be critical. That’s when we’re projected to hit the X-date—the point at which the Treasury may no longer be able to fund the government or service our debt.

With all of that in play, the ripple effect showed up in April’s Existing Home Sales, which dipped 0.5% — coming in below expectations.

There’s clearly pent-up demand in the market, but with rates moving higher, many buyers are hitting pause and waiting for conditions to improve.

When rates drop, look-out it will get very busy very fast.

http://www.YourApplicationOnline.com

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.