-

How Did the Iranian Conflict affect stocks and bonds? Not much.

I was surprised to wake up this morning and see little movement in the stock or bond markets. Sure, bonds improved—but most of that happened last week. And stocks? They’re up, not down.

Oil prices, nope. started out higher but settled back were it was.

So what’s going on?

Iran has responded so maybe that is what the market is waiting for. But still no real change in the stock or bond market this late morning.

How many times have the Strait of Hormuz closed?

Never, even during the Gulf War. It cost more to ship but that was represented in gas prices.

Existing Home Sales rose 0.8% in May to 4.03M. Homes on the market 27 days down from 36 days in April.

http://www.YourApplicationOnline.com

-

Powell Holds the Bat but won’t swing. Who actually gets hurt by high sustained rates?

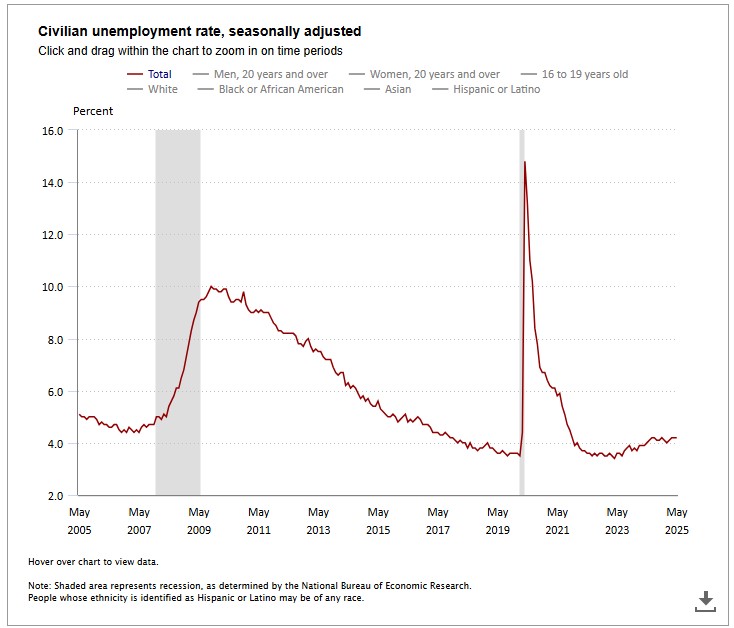

As the Fed wraps up, even Powell concedes: GDP growth downgraded to 1.4% (from 1.7%) and unemployment ticking up to 4.5%.

Clinging to a 2% inflation target is now hurting everyday Americans and small businesses—while giants like Walmart weather it just fine.

Remember Dune? “He who controls the spice controls the world.” Same game, different players.

My take:

The Fed can’t wait forever—rates must come down. There comes a point when the pursuit of control turns into a stubborn battle of egos, and while power struggles play out at the top, the rest of us bear the cost in silence.

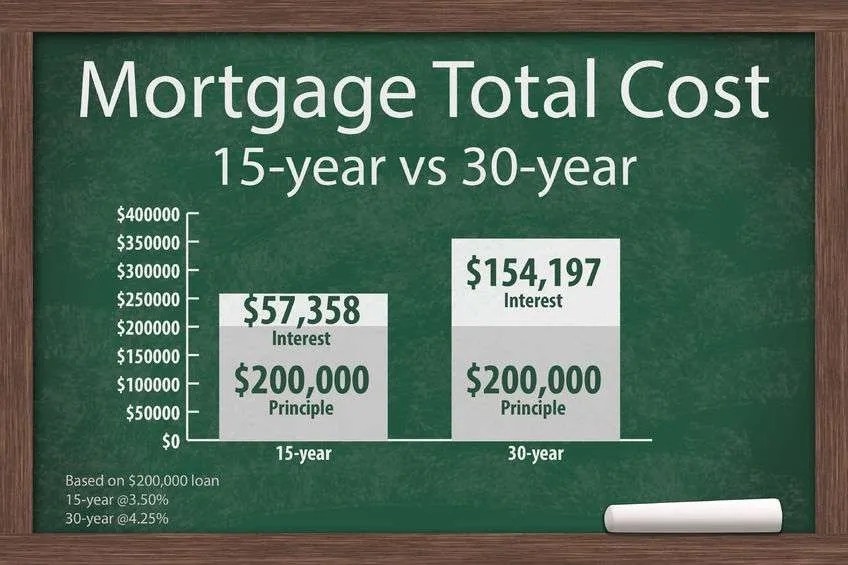

New YouTube Video: 30-Year to 15-Year Refi — Nearly Same Payment, Mortgage Gone 14 Years Sooner!

http://www.YourApplicationOnline.com

-

The Writing is on the Wall. Problem is Powell can’t read.

The Federal Reserve concludes its two-day policy meeting today, with a statement scheduled for release at 2:00 PM ET.

Alongside the announcement, they will also publish the latest Summary of Economic Projections (SEP), which includes updated forecasts for inflation, unemployment, GDP growth, and the federal funds rate.

Recent economic indicators suggest clear signs of a slowdown. Both retail sales and industrial production—highlighted in yesterday’s data—posted declines.

Additionally, manufacturing has been in a prolonged period of weakness, reinforcing the broader narrative of decelerating economic momentum.

My take: I don’t get it. The Fed seems to have strayed beyond its mandate—so afraid of making a misstep, they don’t realize that hesitation is the misstep.

Side note: I just ran numbers for a client who purchased last year with a rate in the mid-7s. We’re now refinancing into a 15-year loan in the high-5s. Their monthly payment is nearly identical—but we’ve eliminated 14 years off their mortgage.

http://www.YourApplicationOnline.com

-

Capacity Utilization. What we can do and what we are capable of doing. What’s Up FEDs.

There’s a distinction between overall capacity and capacity utilization. The chart is particularly insightful, with the gray vertical bars indicating periods of recession.

In May, we saw a slight pullback in capacity utilization—a development that isn’t surprising, considering the impact of tariffs and the surge in purchasing activity during March and April in anticipation of those changes.

Retail Sales in May were -0.9% expected -0.7%. It was a weak report showing consumers spending less.

It was the big ticket items like Autos and building materials showing the largest declines.

Feds meet this week with a zero chance of rate cuts.

http://www.YourApplicationOnline.com

-

Market Reaction and how it affects Rates short and long term.

In most global conflicts, stocks drop and investors rush to the safety of bonds. This time, the stock selloff happened — but the bond rally didn’t show up like it usually does.

Oil prices surged 8% overnight and are up 16% over the past week.

Since oil is a major input in both the Consumer Price Index (CPI) and the Producer Price Index (PPI), this sharp increase has put inflation fears back in the spotlight.Rising energy costs can ripple through the economy — from transportation to goods and services — making inflation harder to contain.

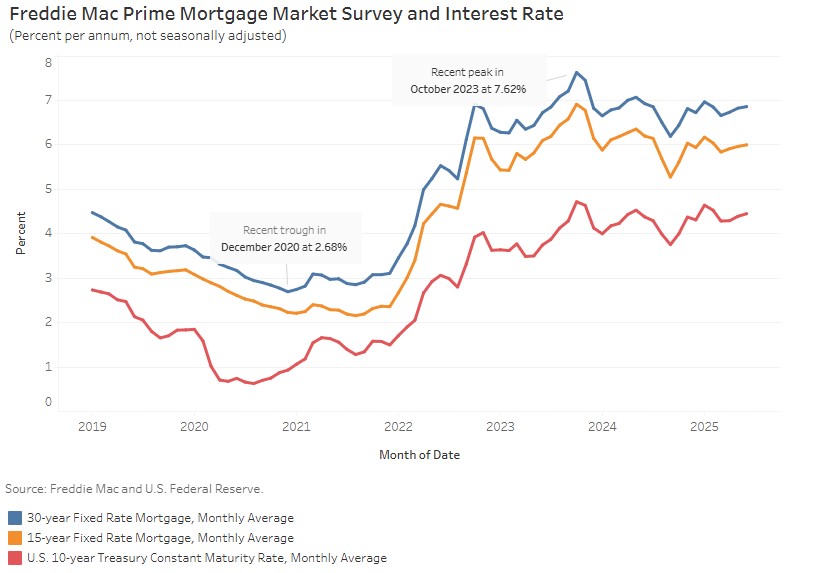

We saw a 30-year Treasury bond auction yesterday, following a strong 10-year auction earlier in the week. Both were met with solid demand, particularly from foreign investors — a sharp contrast to recent media narratives suggesting a global move away from the U.S. dollar and Treasuries.

The takeaway? Stocks took a hit, but the bond market didn’t respond the way we’d expect.

Rates are flat today, though we’re expecting a more favorable shift as early as next week.http://www.YourApplicationOnline.com Soft Credit Pull.

-

What happens if the Fed just drops rates by 2 points. Slower Labor Market impact on rates.

Recession concerns haven’t gone away — they’re just not showing up in May’s PPI report… yet. For now, we’re all in wait-and-see mode, watching to see how inflation really shakes out in the coming months.

What if the Feds dropped rates before inflation goes down?

If the Fed drops rates before inflation comes down, it’s a bit like trying to cool down soup while turning up the stove — here’s what could happen:

Inflation could heat up again

Lower interest rates make borrowing cheaper — whether it’s mortgages, car loans, or credit cards. That encourages people to spend more, which can drive prices up and make inflation worse, not better.It’s classic supply and demand: more buyers chasing the same goods = higher prices.

And just like the scorpion and the frog — it’s in our nature to spend. So when borrowing gets easier, wallets open up, demand rises, and so do prices.

The Fed risks losing credibility

The Fed’s main job is price stability. If they cut rates too soon, markets might think they’re caving to political or market pressure, not economic fundamentals. That can shake investor confidence.Short-term gains, long-term pain?

Yes, rate cuts could give a short-term boost to housing and stocks, but if inflation spikes again, the Fed may have to reverse course and hike rates even more aggressively later — which hurts consumers and markets.Real Estate Angle:

If you’re in real estate or mortgage, a premature rate cut could briefly fuel demand, but if inflation rebounds, rates may spike again — and with it, uncertainty in the market. Timing becomes everything.http://www.YourApplicationOnline.com Soft credit pull.

-

Trade deal behind us, Inflation Down, Powell are you awake or still sleeping?

It’s still unclear whether the full effect of the tariffs has hit the market yet.

Tomorrows Producer Price Index will probably tell us more in the next round of data since it tracks what businesses are paying for goods — which often shows inflation trends before they hit consumers.

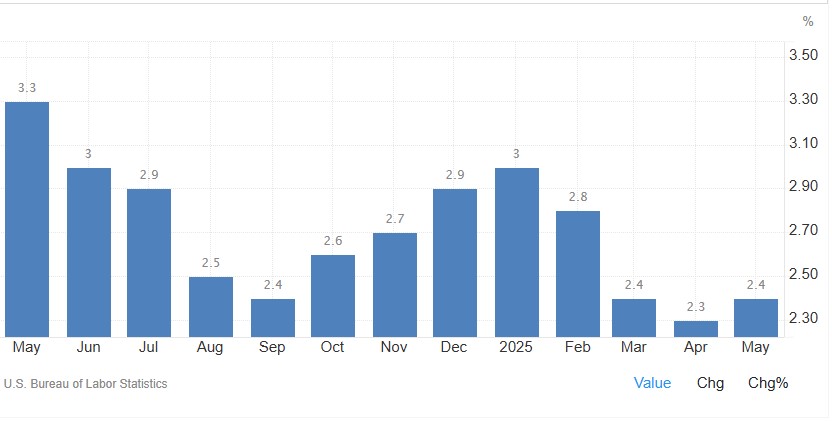

The Consumer Price Index (CPI) came in at just 0.1% — well below expectations. However, on a year-over-year basis, inflation still edged up slightly from 2.3% to 2.4%, just under the street’s forecast of 2.5%.

The World Bank lowered its global growth outlook from 2.7% to 2.3%, and cut U.S. growth projections from 2.3% to 1.4% — yet another sign of economic retraction.

Taken together with the softer-than-expected inflation numbers, this could give the Fed additional incentive to move toward rate cuts sooner rather than later.

Let’s get you financially tuned up and ready to buy, sell or refinance. http://www.YourApplicationOnline.com

-

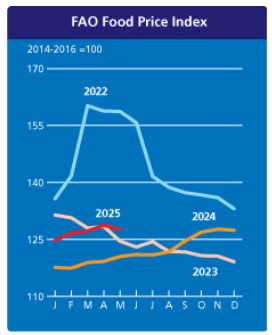

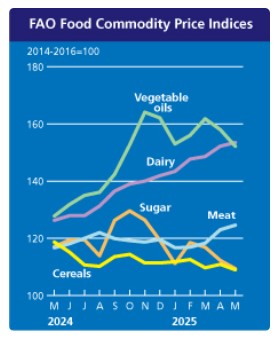

Tomorrow’s CPI inflation Report. Food Price Index from a different perspective. (Graphs, Yay graphs)

These two graphs highlight the commodity price of goods. An interesting data point.

Bonds remain on edge as trade negotiations between the US and China continue. Positive developments have sparked a rally in stocks, which is coming at the expense of bonds.

The CPI report is scheduled for release tomorrow. This marks the first month potentially affected by tariffs, though the market expects only a minimal impact.

A key point in the deregulation debate centers on the required capital ratios banks need to uphold. Treasuries are not expected to affect these ratios. Market consensus anticipates a potential drop in rates of 50 to 70 basis points—roughly equivalent to a 3/8 to 1/2 percent decline.

Almost Wednesday… YourApplicationOnline.com soft credit pull.

-

Why Inflation Numbers are so Impactful to Bonds and Mortgage Rates.

The Consumer Price Index (CPI) report is set to be released this Wednesday. This release is especially important because it will be the first month reflecting the early impact of the new tariffs.

Let’s talk impact of Inflation bonds and mortgage rates.

Inflation reduces the purchasing power of money over time — meaning a dollar today buys less in the future.

How this affects the bond market:

- Bond yields rise with inflation:

Investors want to be compensated for the loss of purchasing power. If inflation is rising, they’ll demand higher yields (interest rates) on bonds to make up for it. - Bond prices fall:

When yields go up, existing bond prices drop. This is because older bonds with lower fixed rates become less attractive compared to newer ones offering higher returns. - Longer-term bonds are hit harder:

The further out the maturity, the more inflation can eat away at returns. So long-term bonds typically drop more in price when inflation expectations rise.

In short:

Inflation = higher yields = lower bond prices.

And since mortgage rates are closely tied to the bond market (especially the 10-year Treasury), inflation often means higher mortgage rates too.http://www.YourApplicationOnline.com

- Bond yields rise with inflation:

-

The Bureau of Labor Statistics (BLS) reported that 139,000 jobs were created in May, above the 125,000 expected.

However, the challenge with these reports is that they are consistently revised downward after the initial release.

- March was revised down by 65,000, bringing the total to 120,000.

- April was revised down by 30,000 to 147,000.

Despite the pattern, the initial headlines do the damage, while the quieter revisions often go unnoticed — or perhaps bond traders just have short memories.

Let’s dig into the details for a moment.

The Quarterly Census of Employment and Wages (QCEW) for Q1 revealed that the Bureau of Labor Statistics (BLS) overstated job growth by 500,000 jobs.

Yes — half a million jobs. Let that sink in.

This raises real questions about the accuracy of headline employment numbers and their impact on markets.

Bond market did not like this report but rates are holding onto gains this last week. http://www.YourApplicationOnline.com

The top photo captures my wife’s shoes catching the morning sun — a quiet, golden moment.

Have a fantastic weekend!

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.