-

New Push to Ban Trigger Leads Relief Could Be Coming Soon

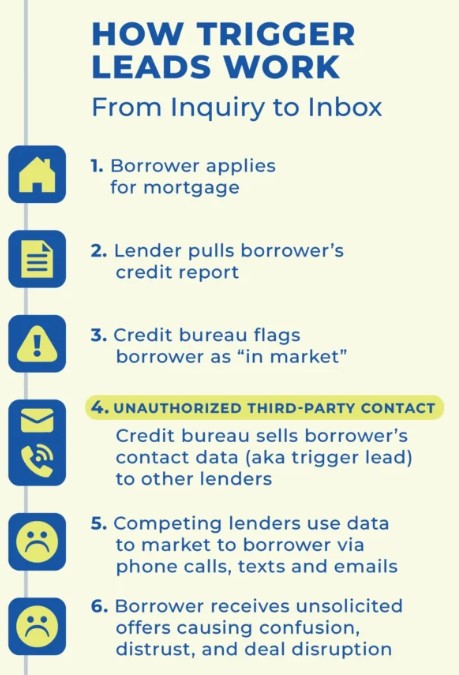

Have You Been Flooded With Calls After Applying for a Mortgage?

You might be the target of a Trigger Lead.Here’s what’s happening:

When you apply for a mortgage, the three credit bureaus (Experian, Equifax, TransUnion) can sell your basic contact info to other lenders. This happens after a hard credit pull.Some lenders buy these “trigger leads” and immediately flood you with calls, texts, and emails, sometimes within minutes.

A soft credit check helps avoid this, but eventually a hard pull is required to fully process your loan.

Why does this even exist?

It was originally meant to help consumers shop around for better loan options—but like many things, it’s now being misused.Trigger Leads Update: Legislation Is Back on the Table

Last year, Senate Amendment 2358, which aimed to ban the sale of trigger leads, was removed at the last minute from the final legislation.

But now it’s back.

The amendment has resurfaced, and there’s renewed momentum to protect consumer information and stop the flood of unwanted calls and solicitations that happen after a mortgage credit pull.

This could be a big win for borrowers and for lenders focused on doing business the right way.

I’ll keep you posted as this moves forward.

My YouTube video below.

-

Big Credit Score News: 5 Million New Borrowers May Now Qualify

The FHFA just announced a major shift:

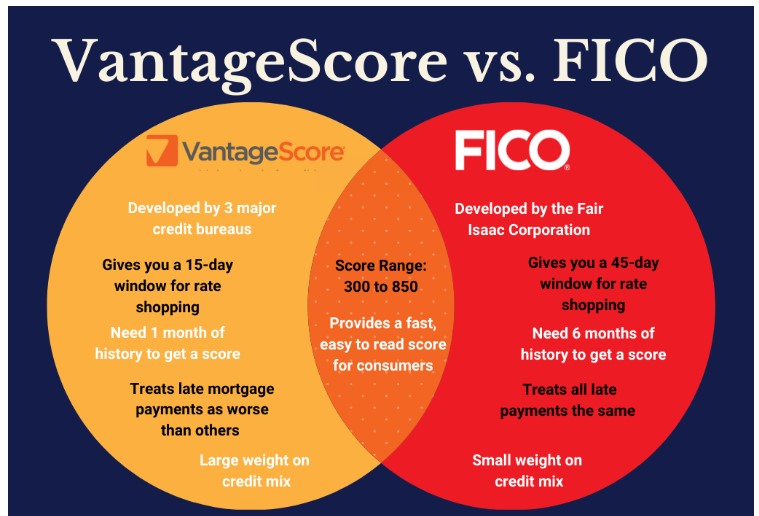

Fannie Mae and Freddie Mac will now accept VantageScore 4.0 for mortgage qualifications.Why does this matter?

Because an estimated 5 million new borrowers, many of them younger, new-to-credit, or underrepresented, could now enter the housing market.FICO vs. VantageScore 4.0: What’s the Difference?

The Similarities:

- Both use your credit report to generate a score.

- Both score on a 300–850 range.

- Both consider factors like credit utilization, payment history, and credit length, just with different weightings.

The Key Differences:

- Credit History Requirements:

- VantageScore: Needs just 1 month of history.

- FICO: Requires 6 months of history.

- Score Versions:

- FICO: Has industry-specific scores (Mortgage, Auto, Bankcard).

- VantageScore: Uses one universal score.

- Payment History Weighting:

- VantageScore places more emphasis on your payment history compared to FICO.

Why This Is a Big Deal

This change opens the door for:

- First-time buyers with limited credit history

- Renters with strong recent credit activity

- Borrowers shut out by traditional scoring models

Want to know if VantageScore could help your clients qualify, or re-qualify? I’m happy to run the numbers. Just reach out!

-

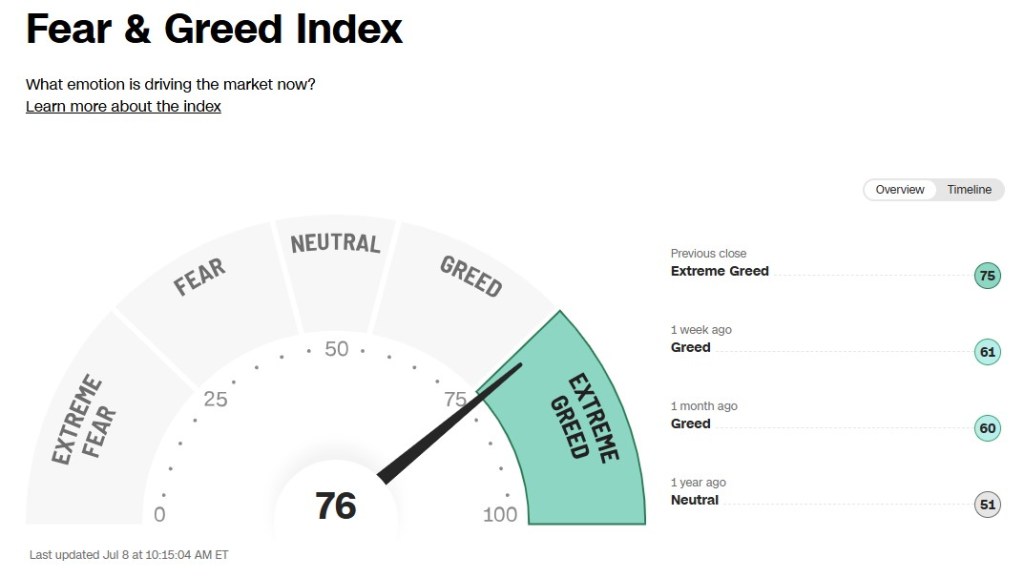

What is the Fear & Greed Index and why is it Extreme Greed.

Puts and Calls options, Selling or Buying. The higher the ratio the higher the Fear and Greed. No one wants to be left with the hot potato.

Quick Market Snapshot:

Inflation? Still calm for now. Stephen Miran, Economic Chair, appeared on CNBC this morning and said inflation and tariffs are “not a thing… yet.” Translation: No immediate threat, but worth watching as policy and election dynamics evolve.

Margin debt which is money borrowed by investors to amplify gains, is now at an all-time high. While this can fuel rallies, it also means any downturn could be sharper and faster as leveraged positions unwind.

The Reserve Bank of Australia surprised markets by pausing a rate cut that had a 95% probability priced in. The signal? Central banks may not be as dovish as expected and the bond market noticed. Global yields moved higher, pressuring borrowing costs.

My Take:

Inflation is still stubborn and hanging on tighter than expected. The Fed needs to stop hesitating and start moving on a rate cut. This constant back-and-forth “we might cut, but only if…” combined with the threat of more tariffs, is creating confusion and volatility.It’s time for consistent policy and less noise. The markets, and the economy need clarity, not more mixed signals.

http://www.YourApplicationOnline.com Soft Credit Pull

-

The Deficit Doesn’t Matter… Until It Does — But Where Will It Show Up First?

Maybe the reaction won’t show up in the Treasury market right away—bonds are pretty subdued today. But it might show up in the price of gold, or in the strength of the dollar. One way or another, it will show up.

The bond market, what drives mortgage rates, isn’t just local, it’s global.

The world buys our bonds, and we issue more bonds to cover growing debt.

More debt = more bonds.

At some point, you have to ask: will global appetite for U.S. debt start to sour?This week will be busy with Trade, Energy, and Earnings reports.

OPEC is increasing August output, housing has cooled a bit, but once the Fed finally cuts rates, we’re likely to see a major boost in activity.Get your financial mortgage house in order and let us pre-qualify for a refinance or purchase. Soft credit pull http://www.YourApplicationOnline.com

-

Why Did ADP show -33,000 jobs but todays BLS Report show +147,000 – Smoke and Mirrors.

I’ve been saying it for years: the BLS report is a masterpiece of BS. Their method for tracking job gains and losses? Brace yourself it’s surveys.

Yes, seriously. Someone picks up a phone, calls 60,000 households and businesses, and asks, “Hey, hiring anyone?” That’s our national employment data, folks. Brought to you by the same process used to figure out who really watches Game of Thrones.

Meanwhile, ADP is over here with actual payroll data, you know, numbers from real paychecks of real employees at real companies. Crazy, right?

So let me ask: whose data would you trust?

The guys with the spreadsheets and timecards… or the ones with a phone and a clipboard?The Bond Market reacted and not in a rate positive way.

Still holding onto gains.

http://www.YourApplicationOnline.com Soft Credit Pull

-

Fed Rate Cut Incoming! Will Mortgage Rates Notice This Time… or Keep Ghosting Us?

Typically, the 10-year Treasury tracks closely with the Fed Funds Rate, but that wasn’t the case last year.

Despite rate cuts in September, November, and December, mortgage rates actually went up.Why? The bond market took a hit from misleadingly strong job creation numbers reported by the Bureau of Labor Statistics, which were later revealed to be way off. On top of that, inflation readings in January and February came in hot, adding more pressure.

This time, things look different.

Job growth is slowing, and inflation is showing signs of stabilizing. The most recent ADP Employment Report showed a loss of 33,000 jobs, far below the expected 95,000. That’s a significant miss, and it supports the Fed’s case for easing.

Bottom line: This could be the window where a Fed rate cut actually leads to lower mortgage rates.

http://www.YourApplicationOnline.com

-

If We are All sure We are right, Who’s wrong. Data Mining and the Dangers of Curated News.

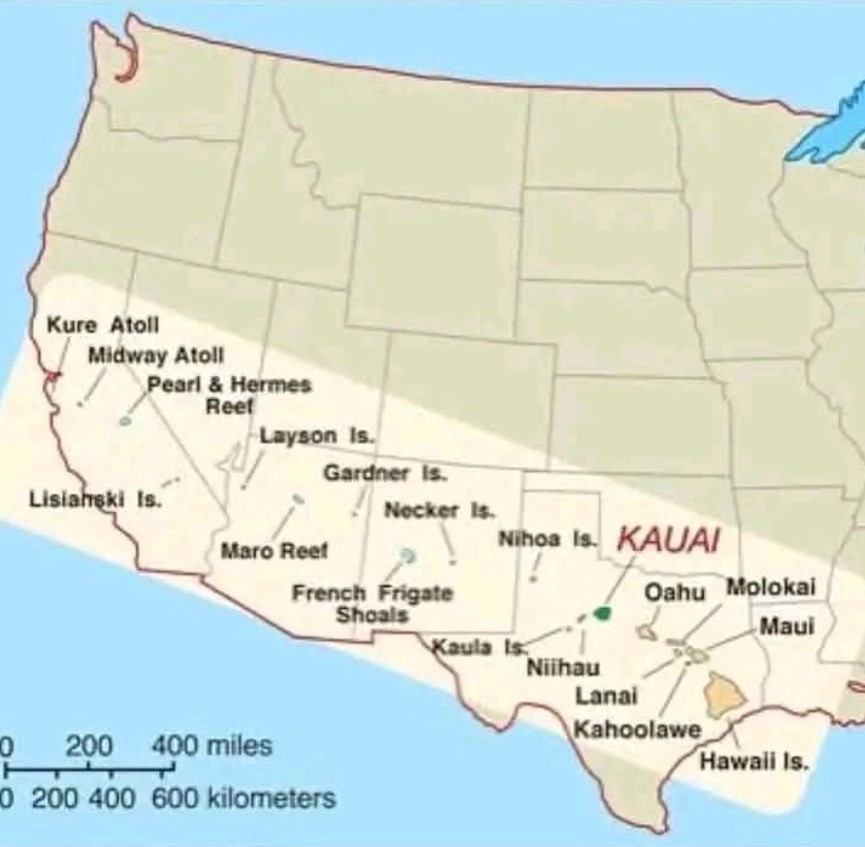

Did you know the Hawaiian Islands are that spread out? It’s like when someone visits the U.S. for a week and thinks they can drive coast to coast and back—nice idea, not realistic.

Today, CNBC real estate contributor Diana Olick sounded the alarm on mortgage delinquencies. But context matters. The increase was barely a blip, rising from 0.95% to 1.01%. Blink and you’d miss it.

There’s a real danger when the news is tailored just for us—not for everyone. It tells us exactly what we want to hear, exactly when we want to hear it. And that’s the problem.

We’re making financial decisions that will shape the rest of our lives—based on what, exactly? Take a moment. Breathe. Mortgage rates are gradually coming down, and real estate has consistently proven to be one of the best long-term investments.

http://www.YourApplicationOnline.com

-

Throwback Thursday. Rollback Capital Requirements could drop Rates a Point this Summer.

Market Update

The Federal Reserve is proposing a reduction in bank capital reserve requirements from 5% to 3.5%. While that may seem like a small shift, it could significantly impact interest rates. Why? Because it would free up billions in capital, giving banks more lending power. If approved, we could see this take effect as early as this summer.

Economic Data Highlights:

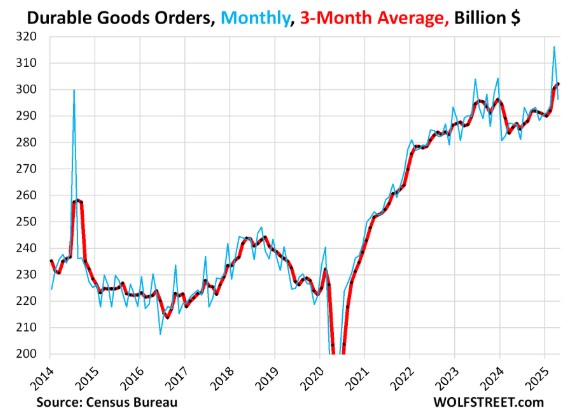

- Durable Goods Orders surged 16.4% last month nearly double the 8.5% forecast. Big-ticket items like appliances are still in demand.

- Jobs Market continues to show stress. Layoffs are rising, and it’s taking longer for people to find new employment. This has been a consistent trend in recent months and may persist.

- Pending Home Sales came in stronger than expected, up 1.8% versus a projected 0.5%.

My Take:

There’s a fundamental shift happening—not just in the economy, but in the bond market itself. This time, it feels real. Palpable.Let’s get you ready. Soft Credit Pull http://www.YourApplicationOnline.com

-

Do I watch Golf for four hours or Powell’s congressional hearing? Its a tossup.

For the second day in a row, Fed Chair Powell is testifying before Congress and yes, I totally geek-ed out. I ended up watching for over 40 minutes… while technically working. Multitasking at its nerdiest.

Powell made a comment I’m paraphrasing.

If we get it wrong our future generations will pay the price.

The thing about waiting on a decision is… well, that is the decision.

A growing group of Fed voters are starting to disagree, I know its shocking. And that ever-elusive 2% inflation target?

Based on data that’s about as precise as weighing an apple by counting every atom. Technically possible, totally impractical. Kind of like expecting perfection in an imperfect world.

New Home Sales came in weaker than expected, but home values continue to climb up 3.7%.

Get outside and enjoy the summer sunshine! Have a great rest of your week. Just two more days until Vegas. I’ll be sure to send pics!

http://www.YourApplicationOnline.com

-

When Doves Cry or Fly… Prince

Rate improvement today isn’t necessarily tied to Powell’s testimony before Congress, but rather to the growing shift among Fed officials. Doves like Fed Governor Bowman and Chicago Fed President Goolsbee are now aligning with Governor Waller in signaling potential rate cuts as early as July.

What’s truly powerful is how much impact a single point drop in the Fed rate can have. It ripples through the economy and directly benefit middle and lower-middle class consumers.

Doves lean towards easing rates, Hawks have their talons poised for a long battle.

Home Values

Year-over-year, home prices rose 2.7%. However, some of the areas in the South and Southeast that saw the sharpest gains are now starting to come back down to earth.

Have a great rest of your week and stay cool. We are headed to Vegas Friday, Temps 104 this weekend.

http://www.YourApplicationOnline.com

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.