-

Fed Gov Bowman wants THREE rate cuts this year. Finally

Her point: with employment growth averaging just 35,000 over the past three months and unemployment at 4.3%, there’s already more than enough reason to start cutting rates now.

It’s like a rock rolling down a hill, much easier to stop early than to wait until it’s gained momentum and rolls right over you.

We expect inflation to rise, but not for the reason you might think.

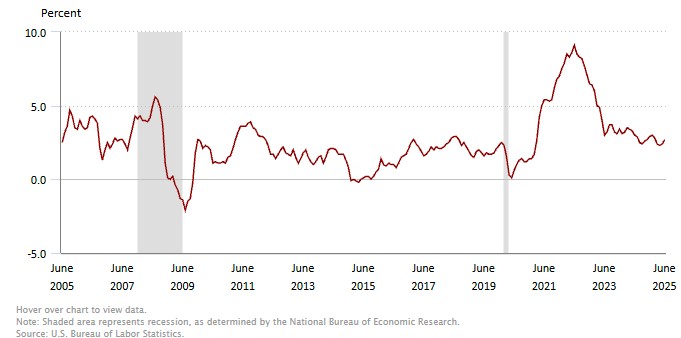

Remember, inflation is measured against the previous 12 months. This month’s reading will likely be a modest 0.16%–0.20%, replacing an already low 0.19% from last year.

It’s a busy reporting week ahead. CPI as mentioned above, PPI, initial Jobless Claims, Retail Sales and more.

We’re continuing to float our clients as current technical indicators show no signs of imminent risk.

Shout out to the open house agents working hard this Sunday, always great to hear your perspective from the field.

Apply now http://www.MortgageNews.Blog soft credit pull.

12-month percentage change, Consumer Price Index.

-

Sub-6% Rates Are Coming. Let Me Show You How

The spread between the 30-year fixed mortgage rate and the 10-year Treasury yield has narrowed to 2.36%, and that matters.

When mortgage rates were in the 7’s, investors were worried about clients refinancing out of their high rates, so investors demanded a large spread to compensate for the risk.

Now, as rates begin to come down and those fears ease, the spread is shrinking, a sign that the market sees less risk of early refis.

Banks are getting a deregulation boost, and Fed rate cuts are looming.

If the 10-year Treasury yield drops to 3.90% (currently at 4.288%) and the spread narrows to 2.25% (currently 2.36%), we could see mortgage rates fall to 6.125%.

And this is just the beginning.

As the Fed continues to cut and the spread keeps tightening, rates will drop well below 6% by years end.

Online Application http://www.YourApplicationOnline.com

-

More Global Rate Cuts: The Writing’s Not Just on the Wall — It’s in Bold Ink

The Bank of England just announced a 25 bps rate cut, bringing the benchmark rate to 4.00%.

Notably, one dissenter pushed for a more aggressive 50 bps cut, signaling growing concern about economic momentum.As for the image above, it’s interesting, but it doesn’t accurately reflect global GDP contributions, where the U.S. and other Countries still accounts for the lion’s share.

Jobless Claims rose 7,000 to a still low 226,000. Continuing claims are still elevated and hit the highest levels since 2021. Rose 38,000 to 1.974M.

My take: we know the economy is slowing, other countries have lower and far lower Central Bank Rates. The pressure for not just September but more cuts through the end of the year which should drive interest rates down.

Lets get you pre-approved and ready to move on your new house.

-

The Wait Is Over: It Might Be Time to Make Your Move

Neel Kashkari, President of the Minneapolis Fed, says the labor market and broader economy are “pointing to a slowdown.”

I’d take it a step further, we’re not heading toward a slowdown, we’re already in it, based on what we’re seeing in the real employment data.

Here’s one clear sign: I’m converting half my clients with 7%+ rates into 20-year mortgages with nearly the same payment as their current 30-year loans.

That’s a huge win, shaving 10 years off without a major payment jump.It’s time to get your house in order — seriously.

Let our team run a quick soft credit pull and get you fully approved for your next home.

Already own a home? We have bridge loan options that can help you buy before you sell. With a full loan approval in hand, you’ll have the confidence to list your current home and move forward with peace of mind.

Website http://www.YourApplicationOnline.com

-

The Jobs Data You Trust? It’s Just a Survey And the Revisions Are Late Homework

I’ve been sounding the alarm for years about the inaccuracy of the BLS jobs report compared to actual ADP data.

Two months ago, the red flags were clear: ADP reported 33,000 job losses, while BLS claimed 144,000 new jobs. Something didn’t add up.

What’s frustrating is that Fed policy leans heavily on the BLS report, even though it’s deeply flawed—not politically, but structurally.

The BLS relies on surveys sent to businesses without a firm deadline, and revisions happen because companies submit their data late, like turning in homework past due.

OPEC+ plans to increase output by 547,000 barrels per day starting in September — possibly bracing for a shift if India pulls back on Russian oil purchases.

Oil prices matter. They ripple through the entire economy, impacting everything from manufacturing to shipping. It’s a key piece of the inflation puzzle.

Rates moved lower Friday and again today — let’s hope this trend continues!

(Heads up: Green is good lower rates)Let’s get you pre-qualified http://www.YourApplicationOnline.com

-

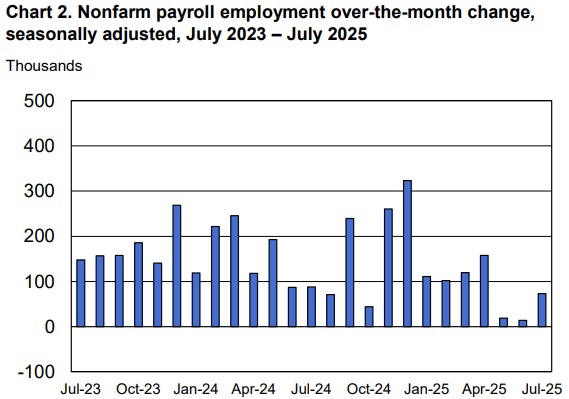

Only 73,000 Jobs in July. Finally BLS report is not BS, rates rally in a good way.

The bond market reacted just as expected to weaker-than-forecast job numbers from the Bureau of Labor Statistics.

But here’s my biggest gripe: revisions.

Remember those “blowout” job reports two months ago? Turns out they were overstated—by 258,000 jobs.This year, monthly revisions are averaging 77,000 jobs lower—more than double last year’s average. That’s a dangerous trend.

Let’s see what July looks like once it’s revised down too.

What does this mean for you?

The bond market is moving toward safety. Employment is sputtering, and the broader economy is showing signs of strain.Pre-approval http://www.YourApplicationOnline.com

-

No Rate Cut but Dissent for the first time. This is Important.

For the first time since 1993, we have two dissenters — Waller and Bowman — both favoring a 0.25% rate cut.

The key shift in language: “The growth of the economy has moderated,” replacing previous references to “expanded,” signals a more cautious tone.

A growing number of Fed members are leaning dovish, pushing for a rate cut sooner rather than later.

Personal Consumption Expenditures (PCE), the Fed’s preferred inflation gauge, rose 0.3% — right in line with expectations.

However, the 3-month annualized rate jumped from 2.0% to 2.6%, a clear sign that tariffs are starting to have an impact.

My take: Powell needs to ease up. These high rates hit everyday people, not the big guys. I get the Fed’s fear of an overheated economy—but from where I’m standing, it doesn’t look like we’re anywhere close. Why not cut now?

-

JOLTS got a Jolt. Job Opening down, rates down as well.

JOLTS Report – Job Openings and Labor Turnover Survey

The latest JOLTS report showed hiring fell by 275,000, coming in 113,000 below expectations. The hiring rate declined from 3.4% to 3.3%, marking the lowest level since 2013 (excluding the COVID period). This points to a clear slowdown in hiring activity.

Quits rate also remained low at 2% meaning less people changing jobs.

Markets responded accordingly, with interest rates moving lower on the news.

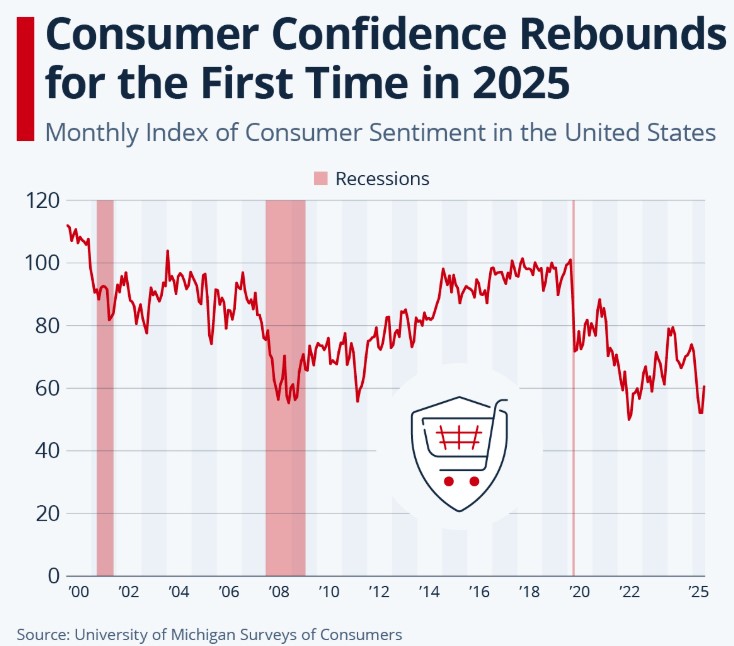

Consumer Confidence: Feeling Good… Kinda

Consumer confidence rose from 95.2 to 97.2 a 2-point boost! 🎉

But before we throw a parade, the expectations component is still dragging below 80.

Translation? Americans are basically saying:

“I feel good today… but ask me about next week and I’ll be hiding under my desk with snacks.”Lets get you pre-approved. Soft credit pull http://www.YourApplicationOnline.com

-

Tariffs are on Import Cost not Total Cost of Goods. I’ll explain why it matters.

I recently went to a clothing store and bought a pair of khaki pants for $76. They were tan, fit well, but I digress. That $76 represents the Total Cost of Goods.

In the context of importing, the Import Cost refers specifically to the price paid to a foreign supplier for the goods themselves. The Total Cost of Goods, however, includes all expenses incurred to get those goods to their final destination, ready for sale. These expenses may include:

- Initial purchase price

- Shipping

- Customs duties

- Insurance

Understanding the full cost is key to knowing where tariffs actually apply.

In my example, the new 15% tariff recently signed between the EU and the U.S. applies only to the cost of goods estimating around $21, not the retail price of $76. That means the tariff is based on a much lower dollar amount—specifically, the price paid to the foreign supplier, not the final selling price to the consumer.

It’s a huge week for inflation, jobs report and the Feds meet.

Lets get you approved. http://www.YourApplicationOnline.com

-

After Yesterday, Less of a chance Powell finishes his term. And Reflective Pic.

After yesterday’s meeting between the President and Fed Chair Powell, the anticipated fireworks didn’t quite materialize—but make no mistake, Powell’s days may be numbered. What that means for rates? We don’t know yet, but the implications could be significant.

Durable Goods Orders dropped 9.3%, but don’t let that headline mislead you, it’s almost entirely due to last month’s spike in large aircraft orders. Context matters.

Looking ahead: next week brings some heavy hitters, Jobs numbers, Q2 GDP, and PCE inflation. Markets are watching unemployment closely, with expectations for a slight uptick from 4.1% to 4.2%.

Found this image yesterday, worth a pause. A reminder to consider the gap between how we project ourselves and who we truly are.

Lets get you pre-approved for a purchase or refi. Soft credit pull. http://www.YourApplicationOnline.com

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.