-

OER: The Fed’s Biggest Guesswork on Rent, and Its Outsized Impact on Inflation – CPI.

What is OER?

OER stands for Owner’s Equivalent Rent. It’s the survey-based measure the government uses to estimate housing costs. In short, homeowners are asked: “How much could you rent your home for, unfurnished and without utilities?”Yes, seriously. And here’s the kicker: OER makes up about 33% of the Consumer Price Index (CPI), meaning this one survey-driven number has an outsized influence on reported inflation. it rose 0.4% last month.

CPI report showed inflation rose 0.4% hotter than expected and brough overall inflation from 2.7% to 2.9%.

Energy prices rose 0.7%, a reminder that energy costs touch every corner of the economy, from production to transportation and everything in between.

My take: Yesterday’s 10-year Treasury auction came in strong, which helped push yields lower, and with them, mortgage rates. The trend continues: rates are drifting down. It may not feel dramatic, but the steady, consistent movement lower is exactly what we want to see.

http://www.YourApplicationOnline.com

-

PPI – Producer and Wholesale inflation cold. Yes we are surprised.

Today’s PPI report came in surprisingly soft, falling 0.1% versus expectations of a 0.3% increase. That moved annual inflation down from 3.1% to 2.6%, giving the Fed even more reason to consider rate cuts — more fuel on the fire for lower rates ahead.

We’re already seeing the impact: national average mortgage rates slipped from 6.625% to 6.5%, which sparked a surge in loan applications. A good reminder, the earlier we get your file fully approved, the better positioned you’ll be to take advantage of these moves.

Tomorrow we get the CPI report, the consumer’s read on inflation. Let’s see what happens.

My take, and I know I sound like a broken record, is this: get ready to buy, sell, or refinance. The pending and current rate drops are exactly what the doctor ordered.

http://www.YourApplicationOnline.com

-

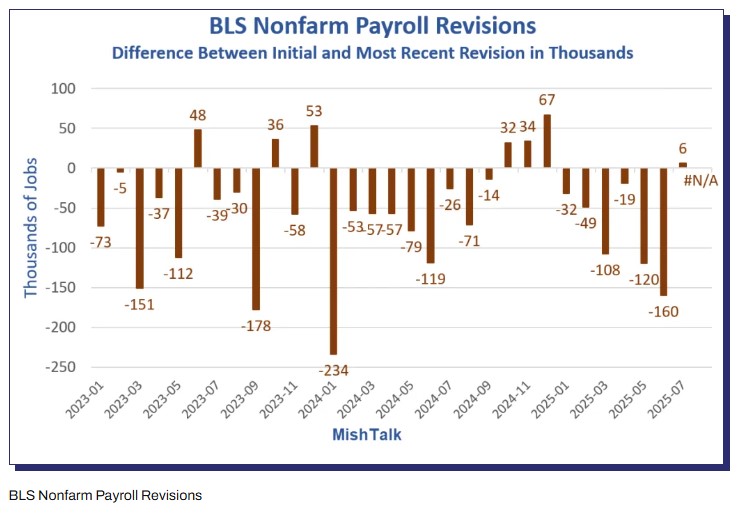

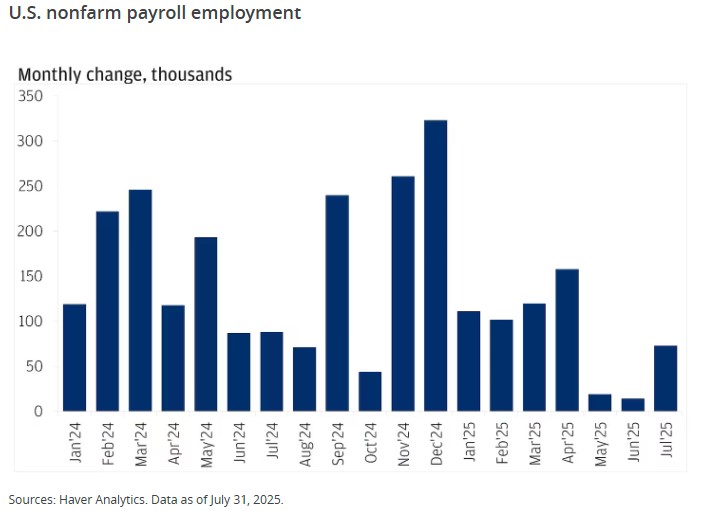

Turns out half the jobs never existed. The QCEW revision just wiped out 911,000. (Told you I wasn’t crazy!)

This is the largest revision on record. On average, that means 76,000 jobs per month, or 52% of the jobs previously reported, never actually existed.

We all knew something was off, and this confirms it. It’s yet another strong signal pushing the Fed toward more aggressive rate cuts.

For now, we’re holding onto the lower rates gained over the past two weeks, following Powell’s testimony at Jackson Hole.

Housing Index Ticks Higher

The housing index finally rose 3 points to 27 on a 100-point scale. While 50 marks the line between contraction and expansion, today’s move shows things are at least headed in the right direction.

Let’s get you pre-qualified so you’re ready when conditions improve. We start with a soft credit pull, no impact on your score.

http://www.YourApplicationOnline.com

-

10:00 AM Tomorrow – QCEW Revision to BLS: And It’s a Doozy

The Quarterly Census of Employment and Wages (QCEW) captures over 95% of U.S. jobs. Tomorrow’s annual revision is expected to show a significant adjustment, potentially 800,000 to 1,000,000 fewer jobs, or about 75,000 per month revised down.

The bond market will react, and the Fed is now almost assured of cutting rates through the remainder of the year, potentially as much as 125bps over the next four months. That means a continued trend toward lower mortgage rates.

If you know friends or family looking to refinance or purchase, send them our way. We’ll take care of them and even start with a soft credit pull, no impact on their score.

http://www.YourApplicationOnline.com

-

Just 22K Jobs: Weak BLS Report Sends Bonds Rallying

Even with a new head at the Bureau of Labor Statistics (BLS), the jobs report didn’t get a makeover. We still saw a weak headline number and downward revisions to prior months. Ouch.

Because as much as we’d all like a little spin… numbers don’t lie.

The unemployment rate ticked up from 4.2% to 4.3%. It may not sound like much, but in Fed-speak, that tiny move can feel like a megaphone. Weak jobs plus rising unemployment = a bond market that starts thinking “rate cuts, rate cuts, rate cuts.”

The odds are now 100% for a 25bp rate cut in September, 75% for another in October, and 70% for a December cut.

Once rates move down in a meaningful way, refinance activity will surge. Let’s get you pre-qualified now so you’re ahead of the rush when it hits.

http://www.YourApplicationOnline.com

-

50 Shades of Beige: The Fed’s Latest Page-Turner

It’s basically the Fed’s “boots on the ground” look at the U.S. economy. Instead of just charts and data, it gathers anecdotal information from businesses, community leaders, and economists across all 12 Federal Reserve Districts.

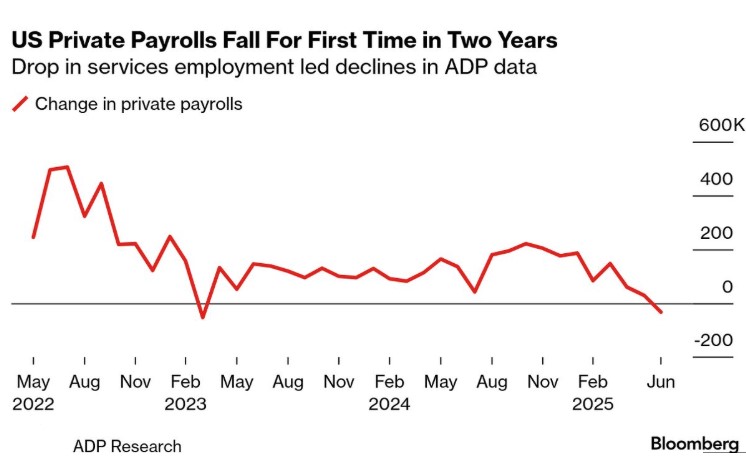

It shows a weakening labor market and with the ADP report confirming, the FEDs have plenty of data to make their move on rates.

We expected 75,000 job gains but only got 54,000 with initial jobless claims rising over 8,000.

Bond Market responded this morning and the mortgage rates dropped.

Remember, the Federal Reserve’s role is to either cool down or stimulate the economy. Raising rates slows things down, while lowering rates helps speed things up. When borrowing costs drop, the cost of doing business becomes cheaper, fueling growth and opportunity.

Lets get you pre-approved today http://www.YourApplicationOnline.com

-

Job Openings JOLTed the Market. And Revisions gone wild.

The July JOLTS Jobs report show job openings fell 176,000 to 7.181M $219,000 less than estimates.

Hiring rate remains low at 3.3%

Quits rate is also low at 2.0%.

FED Gov Christopher Waller said Fed should be cutting next meeting – end of September.

My take:

Labor market is showing its hand and when it does it goes quick. The Feds need to stay ahead of the pain and swallow the rate cut pill now.

apply now http://www.YourApplicationOnline.com

-

Everything and Nothing. How the Tariff ruling affects the Bond Market.

This one caught me by surprise, the lower court’s ruling against using the International Emergency Economic Powers Act (IEEPA) as authority to impose tariffs could have major implications.

Think of it this way: it’s like receiving a generous gift from family, only to spend it on a new car and outfit. Then, two weeks later, they come back and say, “Oops, our mistake. We need that money back.”

The U.S. has collected billions in tariffs, though technically paid by U.S. companies, that may need to be refunded. The big question: where does the government get the money to pay it back? Likely from the bond market.

With that said the Bond market got scared and is trading lower causing rates to move up, slightly.

In other news: Jobs, jobs, jobs! We’ve got JOLTS, ADP, and the always-dramatic BLS report on deck. Could be a real bond mover, in the good way.

Ready to refinance or purchase? http://www.YourApplicationOnline.com

-

Less Demand, Less Supply: Fed Gov Waller Pushes for Half-Point Rate Cut

Waller is looking past the headlines, spotting May–June job revisions (with more likely ahead) and pushing for a 50bp cut in rates. Oh, and by the way… he’s also the frontrunner for the next Fed Chair.

PCE rose 0.2% in July, year-over-year held steady at 2.6%, and Core ticked up to 2.9%, all exactly as expected.

Catch my drift? Everything came in as expected… and the bond market’s reaction was, well, no reaction.

With rates trending lower, I know you have options when it comes to choosing a lender, whether you’re refinancing or purchasing. What sets us apart is not only our expertise in lending, but also our understanding of the market and the timing of when to lock or float a rate.

-

Tomorrow, Tomorrow… Or Not: NVIDIA Beats, PCE Lands, and Markets Hold Steady

The Fed’s favorite bedtime story, Personal Consumption Expenditures (PCE), comes out tomorrow morning. Expectations are for a 0.3% rise, with inflation running at 2.9% annually.

Think of it as the trailer before the big blockbuster: next month’s report will be the real show, for better or worse.

Drama persists at the Fed with Powell pressured to leave and allegations of maleficence. True or not it creates uncertainty which no one likes.

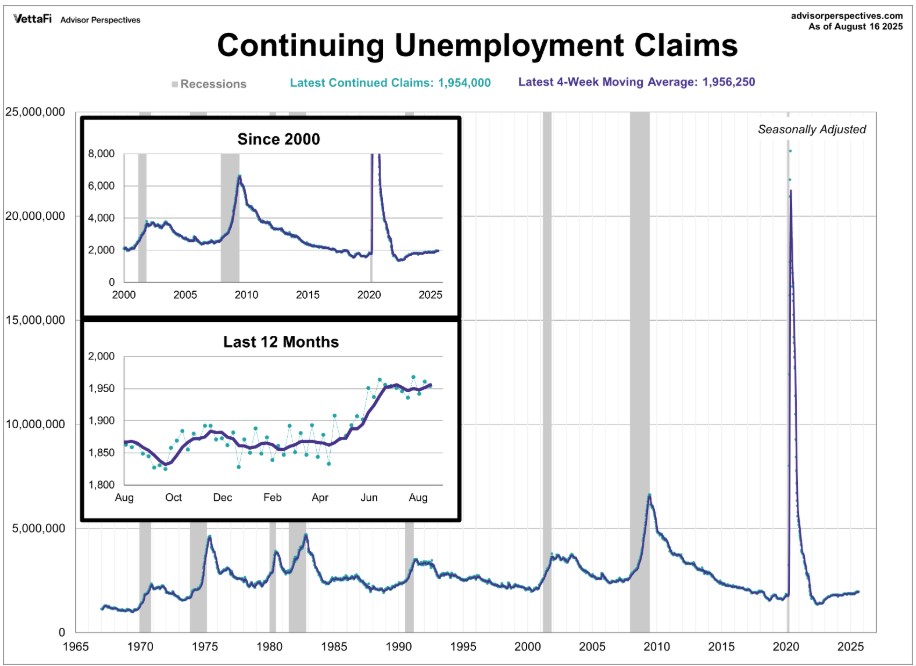

The Initial Jobless Claims report paints the picture of a stable labor market on the surface. But a closer look tells a different story. While about 200,000 people are receiving Continuing Claims, this figure overlooks the 900,000 who fell off the rolls, individuals no longer receiving benefits and still struggling to find employment.

This is a good reminder that headlines and soundbites rarely capture the full picture. To understand the labor market, you have to look beyond the surface.

http://www.YourApplicationOnline.com let’s get you pre-approved.

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.