-

Owning a home builds equity. Renting builds your landlords vacation fund.

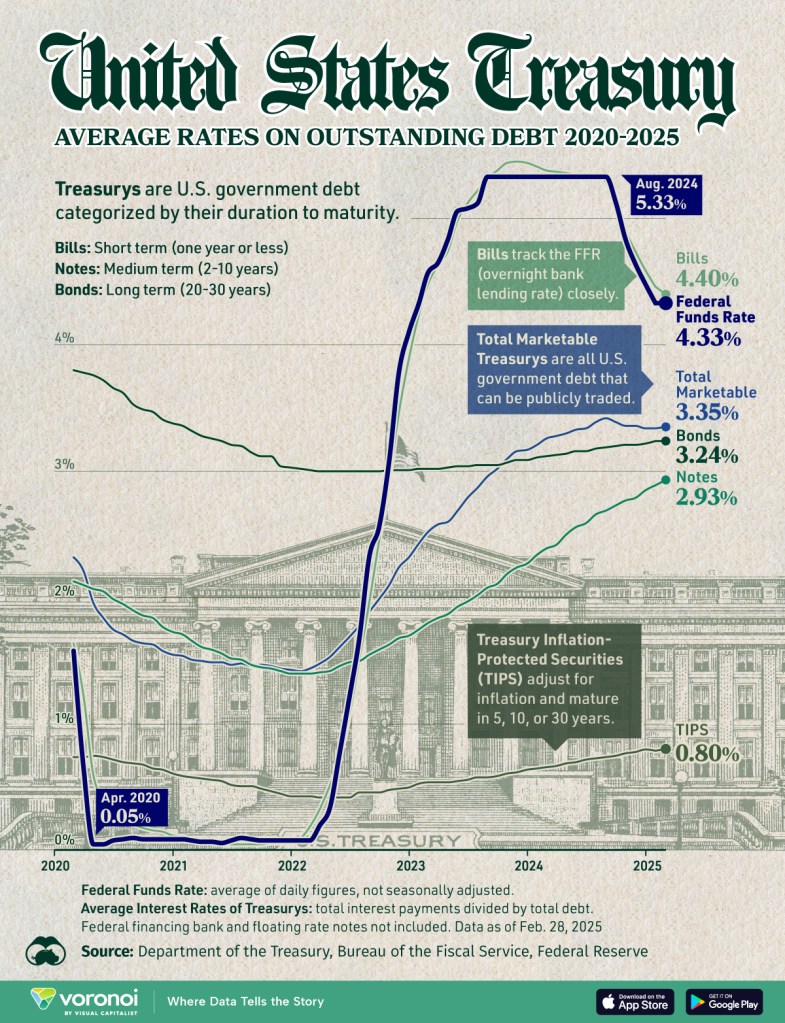

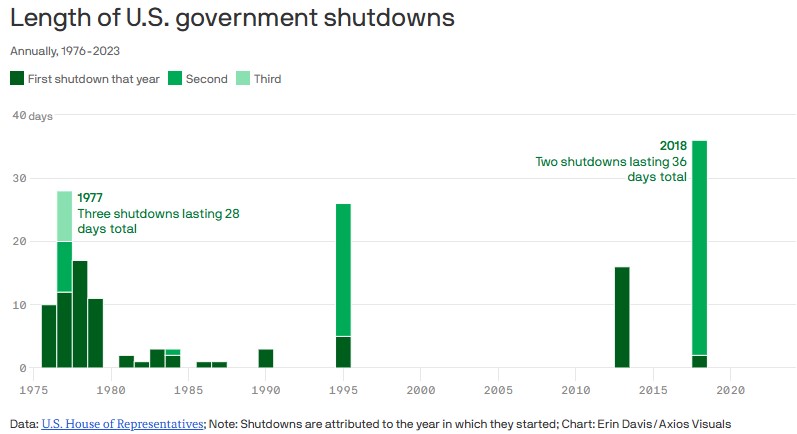

We’ve got a busy week ahead. Bonds are holding their ground for now. Historically, during government shutdowns, bond yields tend to move lower which often translates into lower interest rates.

One idea floating is an interesting way to lower rates. It would be for the Federal Government to sell short-term bonds (6-month, 1-year, 2-year) and use those funds to purchase longer-term bonds particularly the 10-year, which mortgage rates are closely tied to.

My take:

Rates are holding steady for now, while housing inventory continues to rise. Could we see rates in the 5’s by year-end? Possibly. Some clients are already locking into the 5’s with rate buydowns. FHA and VA loans are often at or below 6%, depending on the client’s profile.

Let’s get you pre-approved http://www.YourApplicationOnline.com

-

Government shutdown potential impact buying a home.

A government shutdown doesn’t stop the mortgage industry, but it does slow things down. Here’s how:

- IRS Transcript Delays Lenders often require IRS tax transcripts (4506-C). If the IRS is closed, those transcripts can’t be processed, delaying loan approvals.

- Verification of Employment (VOE) For government employees, lenders may struggle to verify employment and income if HR departments are closed or minimally staffed.

- FHA, VA, USDA Loans These rely on federal agencies to issue commitments, guarantees, or insurance. During a shutdown, those pipelines slow dramatically, creating backlogs.

- Consumer Confidence & Markets Bond markets can become volatile during a shutdown, and since mortgage rates are tied to Treasuries, rates may swing unexpectedly.

- Closings Conventional loans with strong documentation often move forward, but anything dependent on government checks, transcripts, or approvals risks delays.

Bottom line: Loans will still close, but borrowers should expect extra time, especially with government-backed programs. Clear communication between lenders, agents, and clients becomes critical during these periods.

Let’s get you pre-qualified http://www.YourApplicationOnline.com

-

A.I. Sucks… Power that is. How is A.I. revolutionizing the Mortgage industry.

AI is transforming the mortgage industry by streamlining processes that once took days into tasks completed in minutes.

From automating income and asset verification to detecting fraud and reducing underwriting errors, AI helps lenders work faster, smarter, and with greater accuracy.

It also enhances borrower experiences by delivering quicker approvals, personalized loan options, and clearer communication.

The real power of AI in mortgages is its ability to combine efficiency with intelligence, freeing loan officers to focus more on relationships and strategy while technology handles the heavy lifting.

Highlights this morning

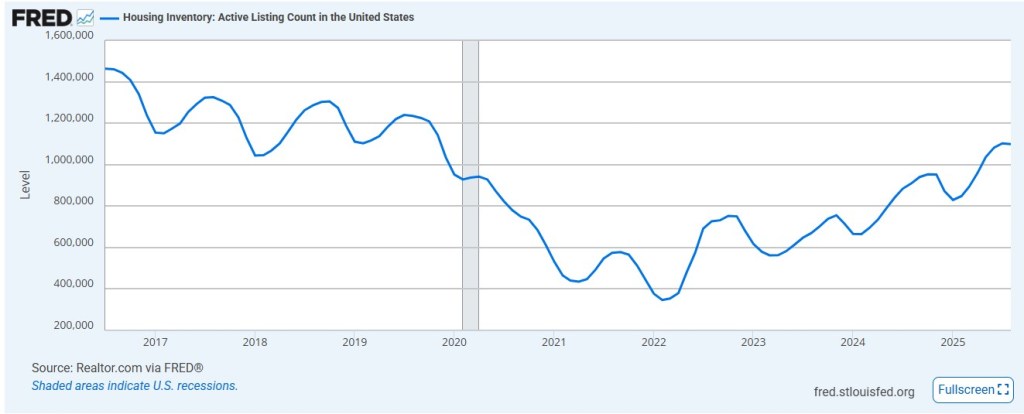

- Housing Inventory up 11% year over year

- GDP increased 2% slightly below expectations

- Initial Jobless Claims lower than expected, but revisions will follow.

Lets get you pre-qualified http://www.YourApplicationOnline.com

-

It’s hard to make Predictions especially about the Future – Yogi Berra

Last week the market was feeling good and had already priced in the Fed’s 0.25% cut until Powell, in all his wisdom, reminded us that everything is still “data dependent.” Translation: don’t get too comfortable. Classic Debbie Downer move.

As a result, we gave back some ground over the past couple of days, though we’re still holding on to part of last month’s gains.

On the bright side, we’re now seeing the biggest spike in mortgage applications since 2022, with a big chunk of that being refinances.

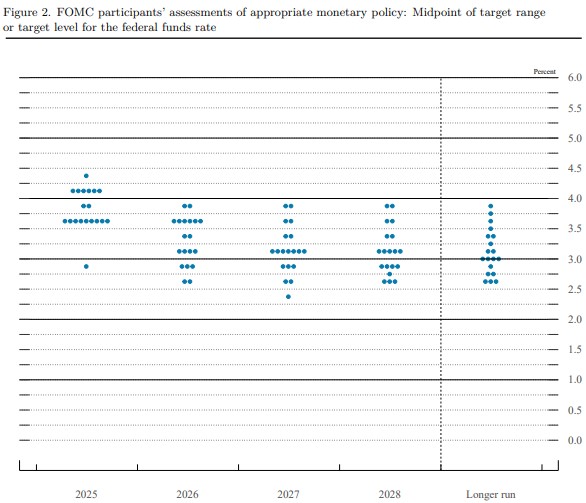

My thoughts: no matter what data you read, it’s always a look in the rearview mirror. It’s the classic case of analysis paralysis. A slew of Fed members spoke yesterday and this morning, with the general consensus pointing toward continued rate cuts.

Powell, however, continues to play the cautious parent, reminding us that “you can’t have your pudding if you don’t eat your meat.”

Refinances and purchases are on the move.

http://www.YourApplicationOnline.com

-

“You’re not the Boss of me” I whispered to my Dog as I put his Blanket on the “Right Way”

So, who’s actually steering the Fed ship? Some days it feels like the Doves have the wheel, other days the Hawks swoop in, and Powell’s just trying not to hit the iceberg. No wonder the markets get seasick.

We have a full slate of Fed speakers this week, setting the stage for a volatile bond market. It’s Doves vs. Hawks and the Fed hasn’t been this divided in years.

Doves continue to push for rate cuts, while Hawks argue the tightening cycle should end here. Today, five Fed members speak three of them voting members, most leaning dovish.

Later this week brings five more, including Powell tomorrow. He remains the wild card: often so hesitant to commit that the lack of a clear decision creates its own uncertainty in the market.

We are carefully Floating our clients refinances and purchase locks today. The Rate is in the details.

Apply now http://www.YourApplicationOnline.com

-

Bond Markets are Forward looking. That’s why Rates went Up Yesterday. What?

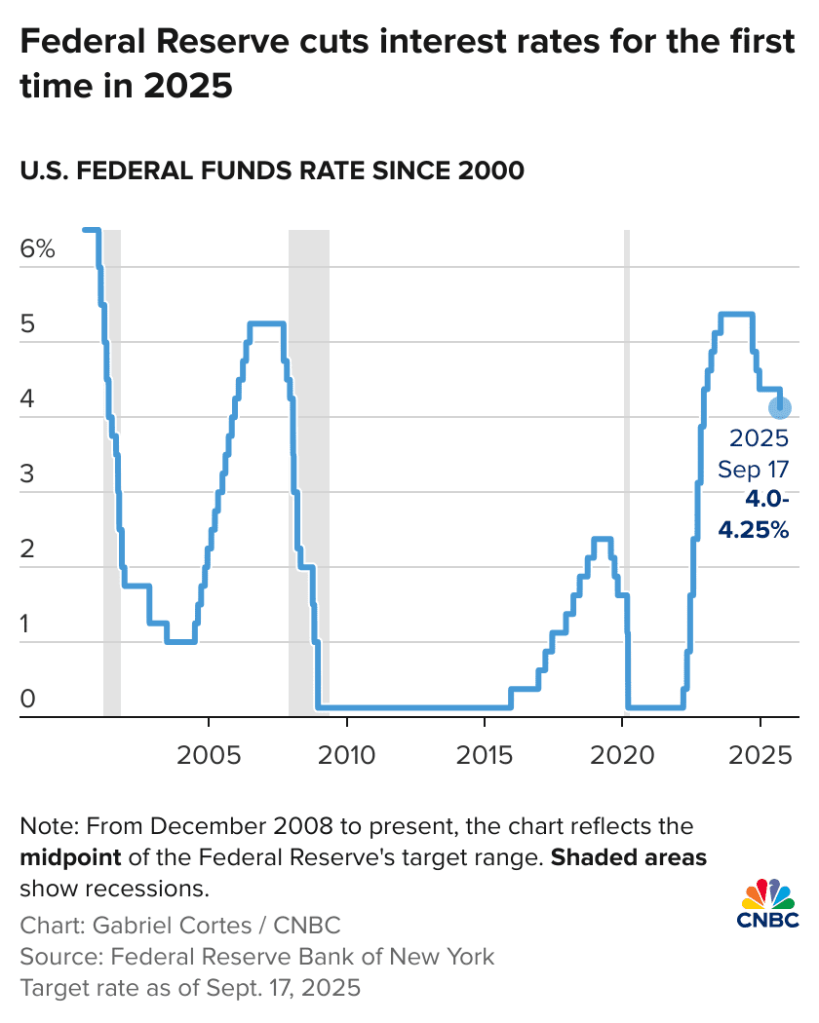

Since Powell’s speech on August 22nd, rates have improved by an average of 3/8%. The market had already priced in, and then received, the Fed’s 25bp cut.

Yesterday, Powell emphasized that policy remains clearly restrictive and signaled there’s still room for further cuts.

While inflation has been the Fed’s primary focus, the shift toward rising unemployment and growing downside risks to the labor market is now front and center.

So why did the rates go up when they are supposed to go down, right?

This morning’s Initial Jobless Claims came in lower than expected, which sparked a bond market sell-off. Money managers in this space react like a feral cat, jumping at their own shadow.

When we invest, we think in terms of dollars and long-term growth. Bond money managers, on the other hand, are often focused on pennies and the very short term.

These expectations are forward-looking, and if the bond market reacts the way it typically does, we should see movement ahead of the actual cuts, just like we saw back in August.

Hang in there… apply online http://www.YourApplicationOnline.com

-

Markets Hold Their Breath as Powell Prepares to Speak

The key this afternoon isn’t just if the Fed cuts, but how. A hawkish cut, done reluctantly, with little sign of more to come, could push bonds lower and rates higher. A dovish cut, signaling openness to further easing, could lift the bond market and drive mortgage rates down.

Let’s take a quick look at what lower rates mean for real borrowers. My client purchasing a $600,000 home with 15% down was at 6.875% back in August. Today, that same loan is at 6.125%, saving about $300 per month on their mortgage payment.

So when I hear critics argue “don’t cut rates, stay the course,” I have to wonder are they thinking about the average person just trying to buy a home?

http://www.YourApplicationOnline.com

-

The Closer It Gets, the Harder to See, Fed Day Arrives Tomorrow

Time flies when you’re having fun, and tomorrow brings the long-awaited Fed announcement on rate cuts. The market has already priced in the expected 25bp cut, but the real story will be whether Powell signals the need for more cuts ahead.

There is a 75% chance of another 25pb cut in October with another 25bp cut in December.

The importers for now are absorbing the higher costs due to tariffs but the lingering fear is higher inflation down the road.

My Take: High interest rates hurt everyone. The job market has clearly cooled, yet inflation remains stubborn. Leaving the Fed rate unchanged only kicks the can further down a road we haven’t traveled in over 80 years.

Mortgage rates have been improving and should continue to trend lower for the foreseeable future, though they can always turn on a dime.

http://www.YourApplicationOnline.com

-

The Rate Cut That Already Happened ahead of the Fed, And Employment Absorption worries.

The market has already priced in the 25bp Fed cut, with the 10-year Treasury yield dropping about 30bp since Powell first hinted at a cut back on August 22.

Mortgage rates move closely with the 10-year Treasury yield because most borrowers keep their loans only 7–10 years, not the full 30. On average, mortgage rates run about 1.5%–2% higher than the 10-year. That extra gap, called the spread, reflects risk and investor demand.

In simple terms: if the 10-year yield rises, mortgage rates rise; if it falls, mortgage rates fall.

Example: A 10-year yield of 4% typically means mortgage rates around 6%.

Job Market overview:

At first glance, fewer hirings matched with fewer job seekers might look like a breakeven but that would not be correct. Without enough demand to absorb those who are laid off, the unemployment rate can climb quickly.

It’s Complicated but bottom line, mortgage rates should continue to decline.

http://www.YourApplicationOnline.com

-

Historically Dips in Rate are Transitory. Cut Wheat while its Sunny.

Over the past few years, we’ve seen rate drops come and go so quickly that it’s hard to convey just how urgent it is for refinance clients to act. The market is truly that volatile.

As the saying goes: watch the dog, not its tail, to see where it’s going. Rates are trending lower overall, but if you watch the “tail,” you can sometimes catch a dip in the movement. Just remember, like a tail, those drops swing back quickly.

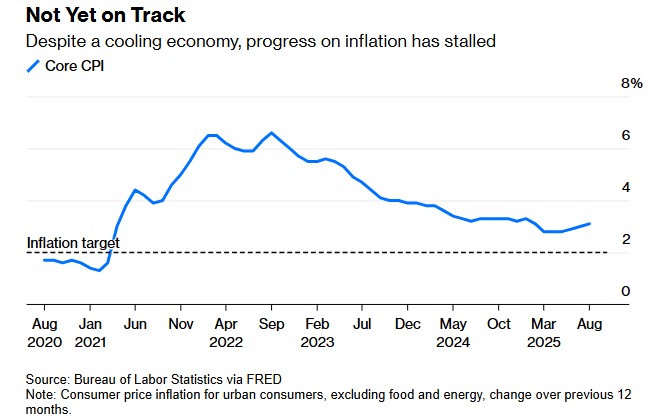

My take: Inflation, while still elevated, appears to be stabilizing, and the labor market is clearly softening. These are exactly the signals the Fed watches, and strong indicators that the market is in need of rate relief.

Let’s get you pre-qualified before the mad rush later this fall.

http://www.YourApplicationOnline.com

Have a fantastic weekend and if you have an open house this weekend, let us know, our team can send you a financial open house flyer.

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.