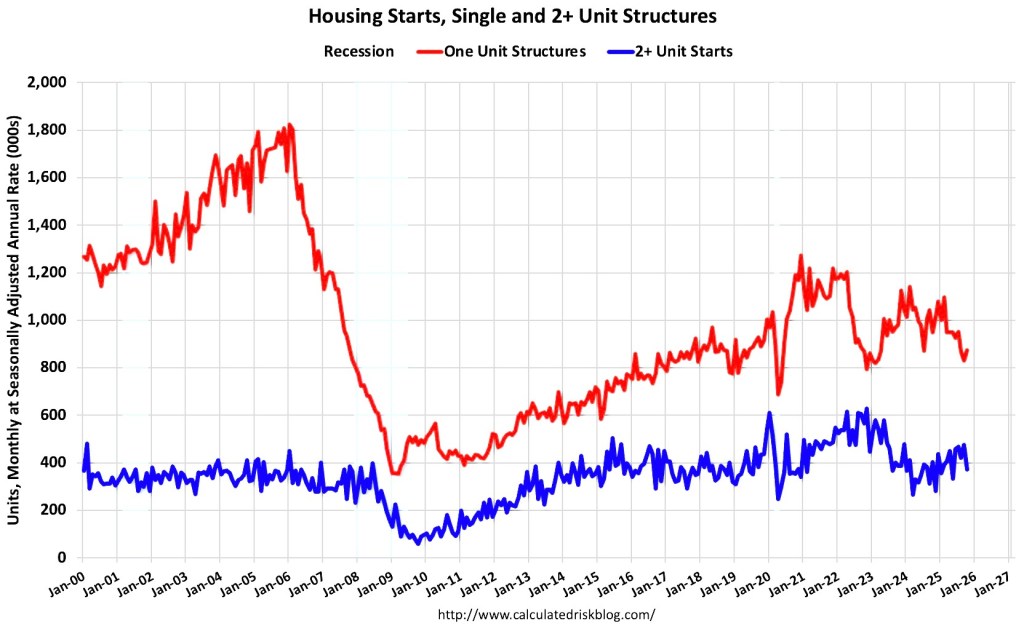

Housing permits, housing starts, and housing completions are all moving higher. While they’re still below last year’s levels, the trend is clearly improving.

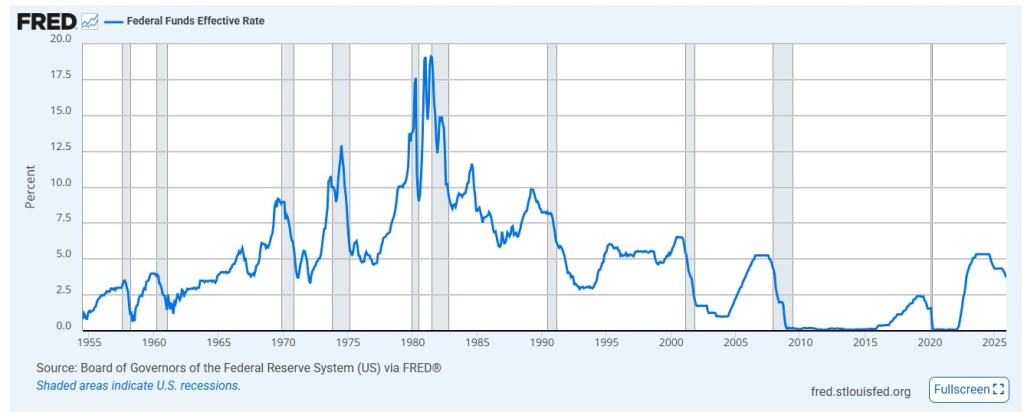

Helped in part by lower interest rates bringing builders and buyers back into the game.

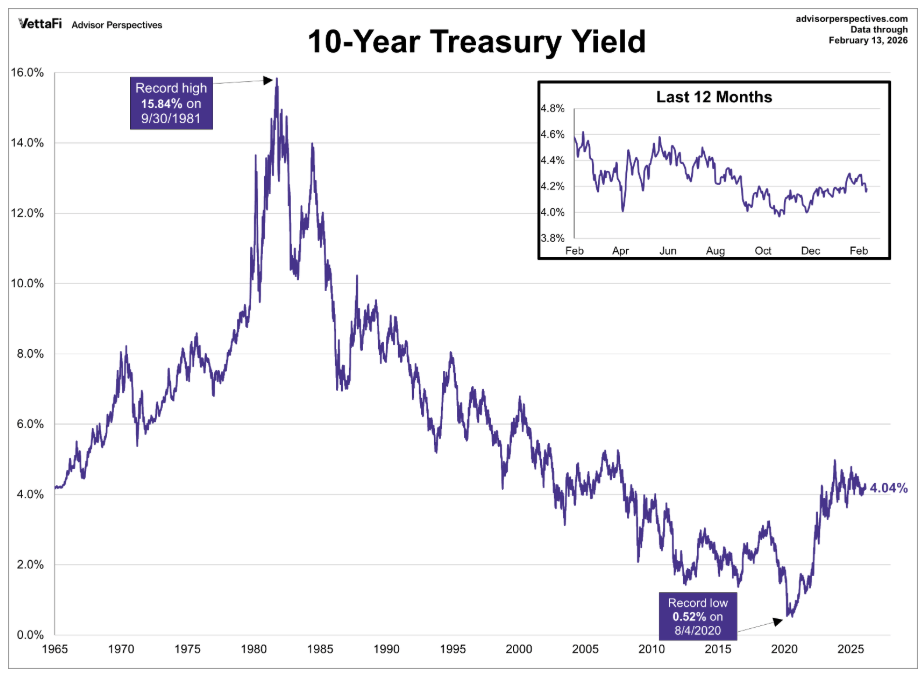

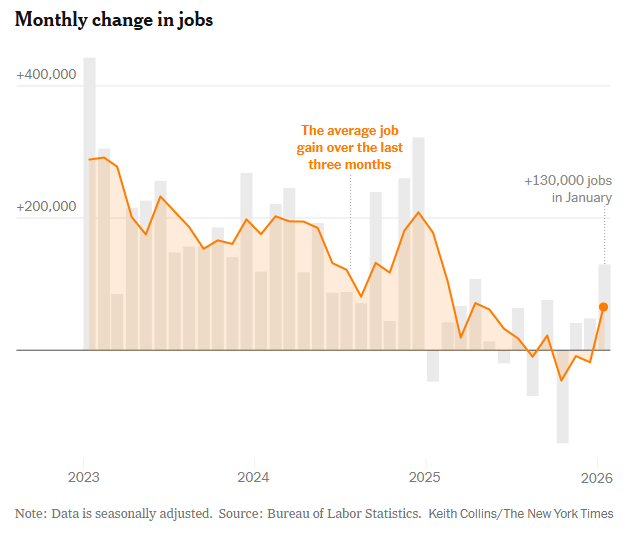

There are still plenty of buyers and sellers sitting on the sidelines. Some are waiting for rates to drop further. Others are hoping for more inventory. And many just want a little more stability in the job market before making a move.

It’s understandable, real estate decisions aren’t small ones.

But here’s the bigger picture: real estate has always been a long-term play. Markets move in cycles. Rates rise and fall. Inventory tightens and expands.

Yet over time, home values have consistently proven to be one of the strongest and most stable wealth-building tools available.

Timing the perfect rate is difficult. Building equity over time is predictable.

The market may not feel perfect, but it rarely is. The key isn’t waiting for ideal conditions. It’s understanding your options and positioning yourself when opportunity knocks.

And right now? The early signs of recovery are starting to show.

http://www.YourApplicationOnline.com Let’s get you pre-qualified.