-

Feds are Sticking to their guns on 2% inflation target.

I’m in Boston MA this week so this will be a quick post.

Chicago Fed Pres, Austan Goolsbee stated this morning that the risk of inflation remains higher than they would like.

Bess Freedman CEO from Brown Harris Stevens stated the obvious or what I have stated for the last year, that demand remains high and no inventory. Once rates come down, More inventory will come onto the market and home values will decline.

Except the last part. There is so much pent up demand for homes that even if we doubled or tripled the inventory we still may not have enough. Home values may adjust but The consensus is not meaningful.

We are headed for a perfect storm in a very good way. Rates will drop with inflation but when we can’t say. Get yourself ready and call us or your lender to get pre-approved with a mortgage checkup.

-

It must be easier was is to make a living but not this much fun…

That was deliberately confusing and Chat GPT agreed, but the point is there.

The Mortgage and Real Estate industry has been put on its head with everyone thinking if we just walk a little further, just over that hill the skies will open.

The reality is the housing market is stuck. Stuck with home owners afraid to let go of their low interest rate mortgages, afraid of what they can or can’t get after they decide to sell and afraid to do the wrong thing.

Not that long ago we went through the 2008 global financial crisis. The same buyers who lost homes 14 years ago and purchased in the last 5 years, don’t want to live through that again and will hold onto their homes even tighter.

Jerome Powell made it clear that 2024 looks to be the same as 2023. Like it or hate it, it is what it is. Get busy or stay on the porch, you decide.

-

Thank you FED … NOT

We continue to see interest rates rise the last two weeks and Jerome Powell, our fearless Fed Chair, did not disappoint.

Though he did not raise the Fed Rate he did state that the rates will remain high for the foreseeable future meaning deep into 2024.What you are seeing below is the UMBS 30YR. This is the 30year Uniform Mortgage Backed Securities. They are passthrough securities, representing an undivided interest in a pool of residential mortgages.

To make it more clear, Down is Bad – higher rates. But as you can see it’s cyclical so we are not falling off a cliff, I hope. To put this into perspective, the top compared to the bottom is about a point and a half of interest rate.

-

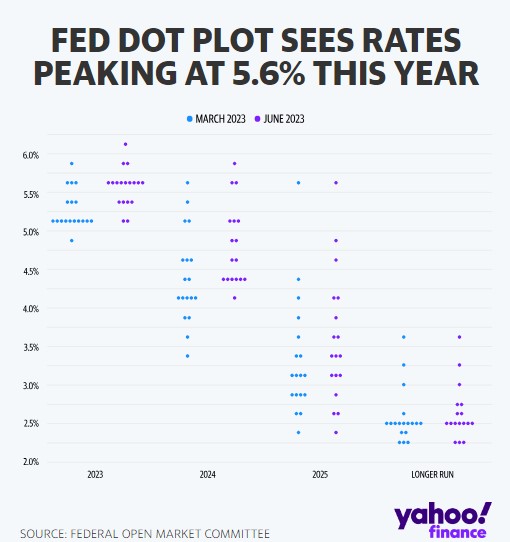

What is a FED Dots Plot chart and why you should care.

The Fed Dots Plot is a chart that shows you where each FOMC – Fed Open Market Committee member thinks interest rates will be by the end of the current year, two consecutive years after, and the more ambiguous “longer run.” Each “dot” represents a member’s individual view.

The graph below is the March and June Plot. Later today we will see the FOMC members projections.

What you are seeing is a strong consensus that the Fed rate will drop in 2024.

We have new projections on GDP, the unemployment rate, PCE Inflation and the new Dots Plot.

Look for Tomorrows post for mor information.

Are you Purchasing or refinancing? happy to help.

-

“The economy is weaker than it appears.” – Kaplan, former Dallas Fed Pres.

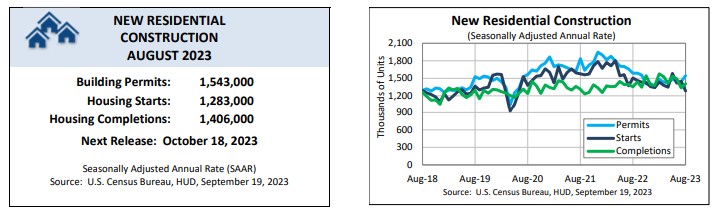

Supply is not keeping up with demand. Housing Starts fell by 11% in August. This means we are 15% down from last year. The decline was mainly in Multi-Family homes.

Single family starts fell 4% last month but up 2% Year over Year. Housing permits, which foreshadow the future supply, were up 7%, but down 3% from last year.

To put this into context. The Demand for new construction housing is 2M+ units. Actual production is 1.4M units. This is one of the reasons housing prices continue to rise.

Not to be too depressing but here are a bit more data points.

Current Sales fell 6%, Future Expectations fell 6 points and below 50%. Buyer Traffic fell 5 points.

Rising mortgage rates, lack of workers and buildable lots, and ongoing shortages of distribution transformers that connect the home to the grid.

To defend the Builders, they are the ones taking the risk. Spend all that money on land, materials and labor in hopes that one year or two years later you made the right decision with no control over inflation or interest rates.

I promise I will be happier tomorrow.

-

Fed Speak, You tell me.

Here are a few quotes from different Fed Presidents across the Country.

“Acknowledged shelter lags and said inflation would be at 2.5% today.”

“Said Fed policy is appropriately restrictive”

“Can be patient and hold rates steady, let actions taken do their work”

“Not how high to take the Fed Fund Rate, but how long”

“If tighter financial conditions are a headwind to the economy, the path of Fed Funds Rate may be lower.”

I will predict today that the Feds will not raise the Fund Rate 25bp. Some top economists disagree but let’s see. Feds meet later this week.

-

Signs signs everywhere a sign. – 5 Man Electric band

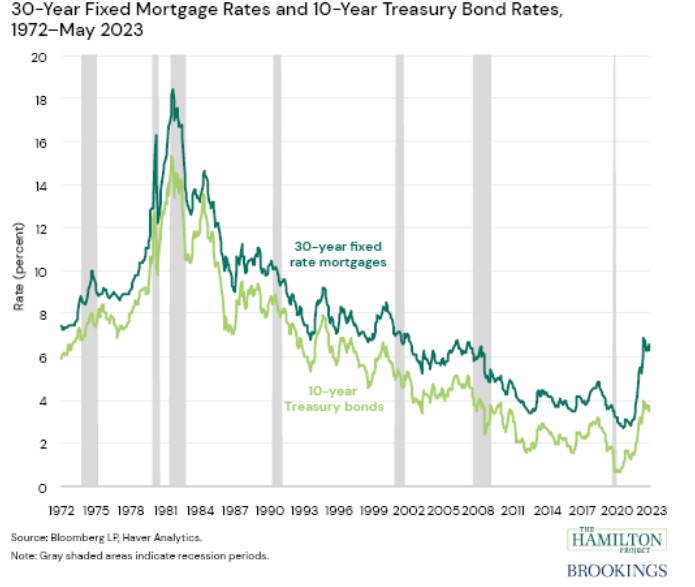

Did you know that the Fed Funds rate at 5.5% is above the 10-year Treasury yield.

Here’s what is interesting. It’s only happened 4 times in history, including right now. Though they don’t follow each other it does show once the Feds start lowering the Fed rate, the Mortgage rates will follow.

Zillow Home Price Index

Home Values rose 0.2% now 4.5% since the beginning of the year. Looking at a 7% full year appreciation.

Have a great weekend and enjoy the song.

-

Only the Past can’t be Changed

NY Fed President John Williams commented on inflation and the real estimates of inflation being closer to 2.5%.

This is the first sign that the Feds are not looking back but forward and projecting the data correctly in our opinion.

An example is retail sales. It rose 0.6% in August, hotter than the 0.2% expected. But when you strip out gasoline, sales only rose by 0.2%.

The idea is to look closely at the numbers and not have a knee jerk reaction.

There are 17% more homes on the market compared to January. This is good news.

-

It’s baked in. Let’s crunch the numbers on Inflation.

There is a feeding frenzy in the news. Inflation is up, oil prices keep climbing….The world is ending… Let’s break down the numbers and take a deep breath.

Yes the CPI August Consumer Price Index which measures overall inflation increased 0.6%, and was in line with expectations. The Core CPI decreased from 4.7% to 4.3% again as expected.

Energy prices rose by 7.3% Y/Y, and was down from 7.7%.

Rents rose 0.5% last month and up 7.8% Y/Y but down from 8%.

Lodging away from home also fell 3%.

A wealth of data flows in, yet many news outlets seem reluctant to delve deeper into the true essence and beauty of the data. It’s akin to observing a single bird soaring through the sky, swiftly changing course from left to right. Only when you step back and broaden your perspective do you witness the mesmerizing spectacle of a flock of birds engaged in a graceful ballet.

We are headed in the right direction. The FEDs will most likely pause on the rate hikes in September given the true long term data that has been coming in this year.

-

Disneyland Opened its gates 68 years ago.

I’m just trying to find my happy place.

Wednesday the CPI Consumer Price Index and Thursday the PPI Producer Price Index for Retail Sales comes out. These are two important gauges of inflation for the FEDs.

Remember the FEDs are data driven.

Definition of CPI: It is the Measure of the overall change in consumer prices based on a representative Basket of goods and services over time.

Forecast for tomorrows CPI is 3.6% from 3.3% but the Core CPI estimate is 4.3%. But it’s down 0.2% for July from 0.6%.

Definition of Core CPI: Is the change in prices of goods and services, except for those from the food and energy sectors.

In a nutshell, Inflation is not going away. The FEDs may say, one more rate hike then we are done.

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.