-

The Battle of the Indicators. Who will win, no one knows? William Dudley knows…

William Dudley is a former NY Fed President and is calling for a 50bp Cut in the Fed Rate tomorrow.

The Federal Reserve focuses primarily on two key factors: inflation and the overall economy. Inflation, heavily influenced by shelter costs and auto insurance, can sometimes paint a misleading picture of the true inflation landscape.

The job market continues to show signs of weakening, with the unemployment rate increasing by 0.8% so far this year.

Dudley highlighted that 92% of the 4 million jobs created were part-time or self-employed positions, yet they are still counted as full-time jobs. This skews the data, masking the decline in job quality.

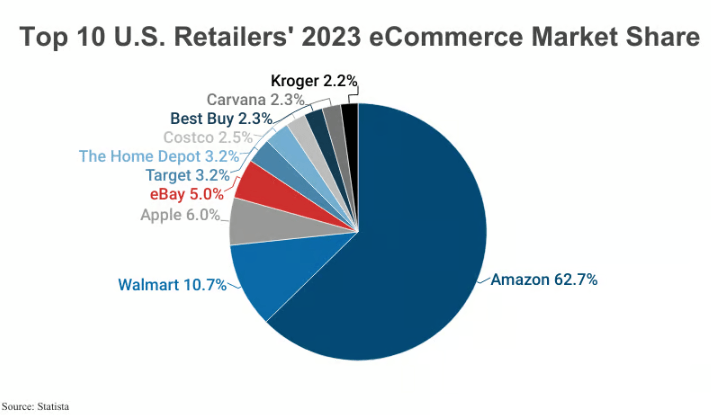

What to know the Power of Amazon? Last months retail sales rose 0.1% primarily due to Prime Day from Amazon. $14.2 Billion in sales on one day.

Rates continue to improve as we hold our collective breath for tomorrows Fed Announcement. I have my money on a 50bp drop then another 25×2 by the end of the year.

-

It’s tough to make Decisions especially about the Future. – Yogi Berra

What will the Federal Reserve do Wednesday. We have some insight.

Former Fed Vice Chair Donald Kohn: “We are at a point where you might say, I could go either way – 25 or 50. but I think the risk management has shifted to the labor market and favors doing 50”.

When we look back, we can see that once rate cuts start, they tend to proceed rapidly.

Later today we will hear from Former Fed Vice Chair, Lael Brainard, now the Director of National Economic Council.

Her prepared remarks were released and highlights that “we have reached a milestone in the fight against inflation”.

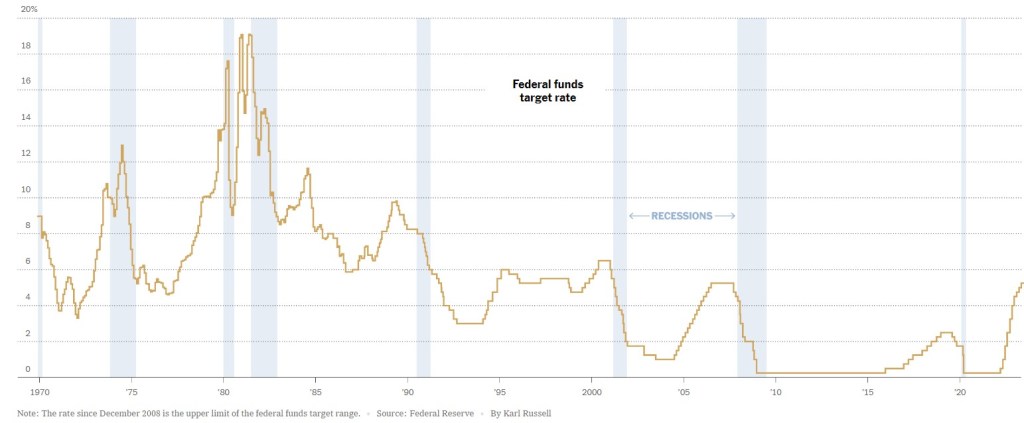

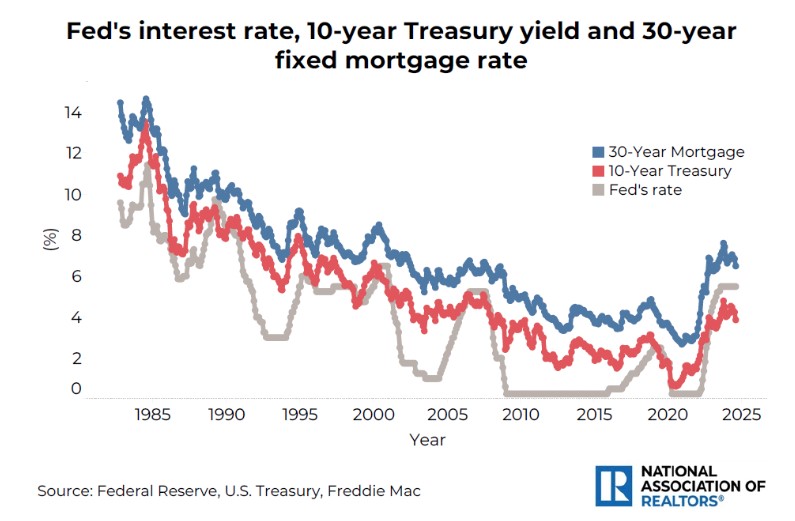

How will this affect the mortgage rates? a picture is worth a thousand words. Mortgage rates have historically followed the Fed Rate.

Feel free to forward, copy and reach out anytime. www.YourApplicationOnline.com

-

To Be or Not to Be.

What will the Federal Reserve actually do on the 18th? The market is expecting, and has priced in, a 0.25% rate cut. Personally, I believe the cut should be more aggressive—at least 0.50%.

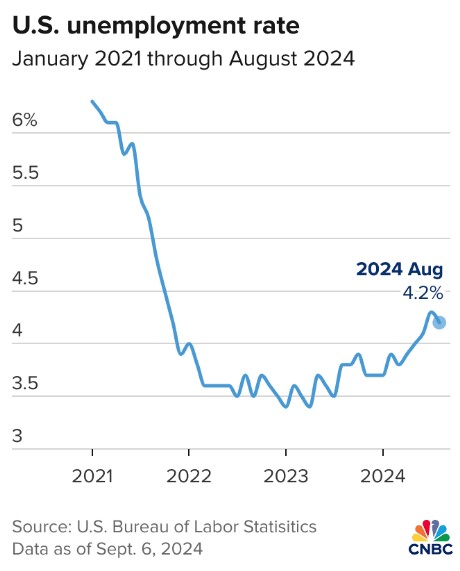

The Fed has effectively shifted the goalposts regarding the timing and size of future cuts. The current unemployment rate is 4.2%, slightly down from 4.3% last month.

Interestingly, 16 out of 19 Fed members predicted unemployment wouldn’t exceed 4.1% this year—yet here we are.

The market is anticipating a 1% rate cut this year and an additional 1.25% next year. Let’s hope the Fed moves forward and breaks free from their analysis paralysis.

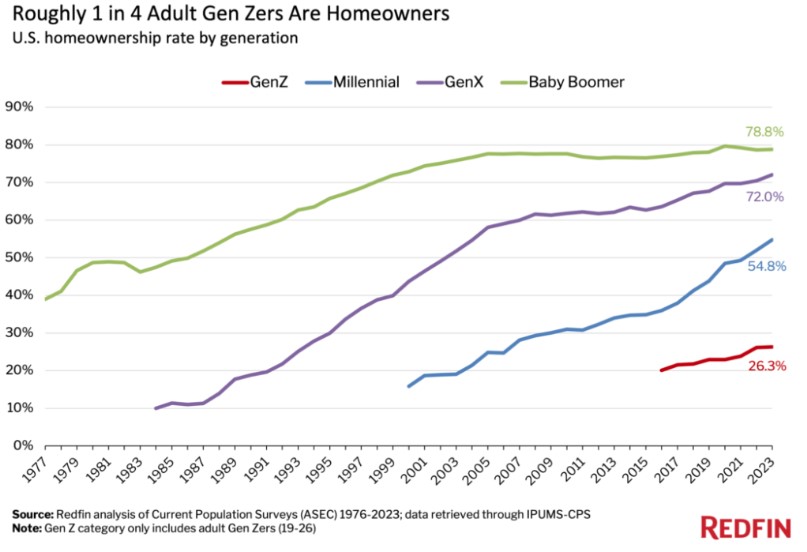

Let’s take a look at the housing market through the lens of different generations.

At age 30, the homeownership rate was 48% for Boomers, 42% for Gen X, and 33% for Millennials. People are waiting longer to get married, have kids, and buy homes. However, by age 40, those rates rise significantly, and Millennials begin to catch up with Gen X and Boomers in homeownership.

-

Let’s Start Paying Attention to 10-year Treasury Note Auctions – seriously

Sometimes, it’s important to step back and pay attention—specifically to the 10-year Treasury’s monthly auctions.

Why, you ask? Here’s why: if you’re an investor expecting yields to continue rising, holding off on buying bonds would seem prudent. However, bond managers who took that approach were caught off guard last month.

Yesterday, demand for bonds surged, proving them wrong.

Producer Price Index, which measures wholesale/Producer inflation rose 0.2% in August. Slightly higher than expected but going in a downward direction from 2.1 to 1.7%. Part of this drop in inflation was due to lower energy prices.

Initial Jobless Claims changed little and inline with expectations.

CoreLogic Equity Insights reported homeowners with mortgages saw an equity rise 8% year over year. 62% of all properties have a mortgage attached.

Interesting Stats:

- 136M total households in the US

- 91M homes owned – 67% homeownership rate

- 56.5M homes currently have a Mortgage – 62%

- 34.5M owned free and clear – 38%

- 45M homes rented – 33%

Time to tune up your financials for a new purchase or refinance. www.YourApplicationOnline.com

-

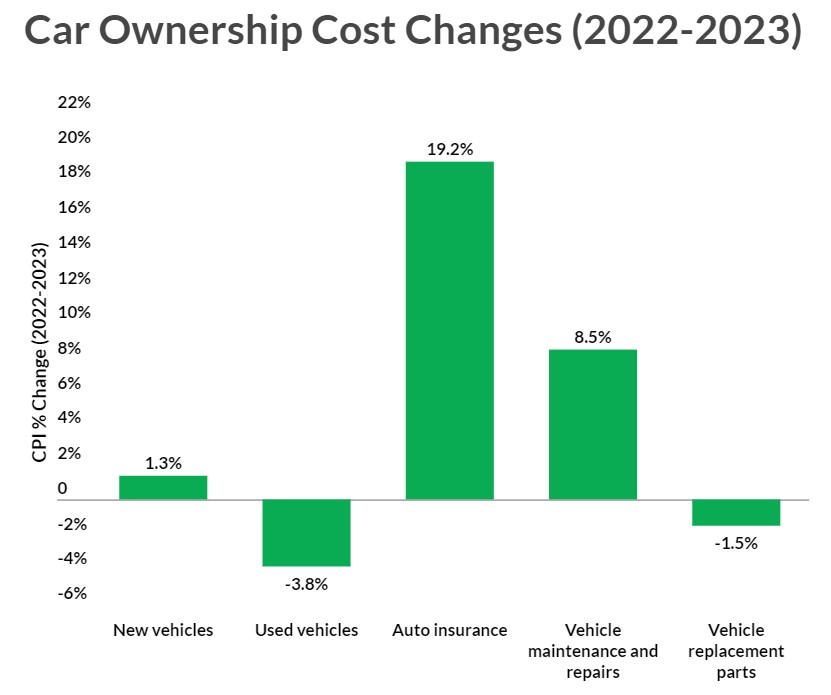

89% of inflation in August was Car Insurance and Rent. But Inflation still dropped from 2.9% to 2.5%.

That’s a remarkable percentage and calculation for the Federal Reserve to consider when making a rate cut decision.

The Consumer Price Index (CPI) report showed overall inflation rose by 0.2% in August, aligning with expectations.

Housing, airfare, and car insurance saw increases, with airfare alone jumping 3.6% last month. While inflation has decreased to 2.5%, 89% of August’s figure was driven by just two key components. Notably, shelter or rent contributes 45.7% to the CPI.

On a year-over-year basis, auto insurance costs fell from 18.6% to 16.5%, making me curious about the profit margins of auto and home insurance companies.

Overall, this was a positive report and provides the Fed with more justification to begin cutting rates.

-

History’s rhythm weaves a captivating melody

In our industry, we are intensely focused on data and the story it tells. At times, it shouts loudly, while other times, it only whispers.

We closely monitor technical indicators, particularly the 10-year and 2-year Treasury Notes. Until this week, the 2-year Treasury yield had been higher than the 10-year for an unusually extended period—longer than at any point in history.

If you’re holding a bond for a longer term, you’d typically expect higher yields as compensation. However, over the past two years, we’ve seen an inverted yield curve, with the 2-year bond offering higher yields than longer-term bonds.

With regards to the September 18th Fed meeting:

Yields goes down on average of 1.5% from the first Fed cut to the last. This would optimistically bring the 10-year bond down to 2.2% from its current 3.7%.

Below is the Bond activity over the last two months. Up or Green is lower rates. We expect this to continue through next week.

-

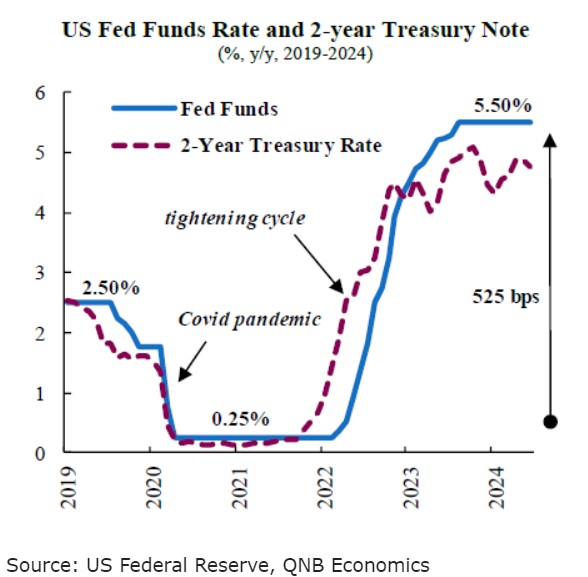

The Differential Argument of the 2-year bond and the Fed rate.

The question I get asked every day is: when and by how much will rates drop?

There’s a compelling case that rates will not only fall, but do so sooner than expected.

If we look at the differential between the 2-year Treasury and the Fed Funds rate, the Treasury is about 1.6% lower. This is a Large gap. Large enough that we have to go back to the 2007 gap.

The Fed aggressively cut interest rates, but ultimately lagged behind the curve, leading to the onset of the 2008 recession.

The Fed is significantly behind the curve and once again needs to take aggressive action to prevent a recession.

The Federal Reserve Meets September 18th.

-

BLS Report is Finally in and…the Bond market responds.

The Bureau of Labor and Statistics (BLS) reported 142,000 Jobs created in August, below the estimates of 160,000.

There were also negative revisions to the previous months as well. This means that 20% of the Jobs originally reported, never existed.

- Average weekly hours increased from 34.2 to 34.3.

- Average weekly earnings rose 0.7%.

- Household Survey showed 168,000 job gains.

- Unemployment rate fell from 4.3% to 4.2%.

Bottom line is it’s incredibly difficult to work with numbers that are constantly revised and getting different conflicting data from independent sources.

The solution is: Watch where the dog is going not how it’s wagging it’s tail.

Rates continue their improvement leading up the the September 18th Fed Meeting.

-

Oil Prices Drop below $70 per Barrel. Deflationary and helpful to rates.

ADP Employment Report for August showed only 99,0000 jobs created. Most with companies with 50 or more employees. This is another datapoint for the Feds September 18th meeting.

We are holding our clients locks until Tomorrow’s Jobs Report.

Now getting back to Oil.

When oil production began, there was no standard container for oil, so oil and petroleum products were stored and transported in barrels of different shapes and sizes. Some of these barrels would originally have been used for other products, such as beer, fish, molasses, or turpentine.

-

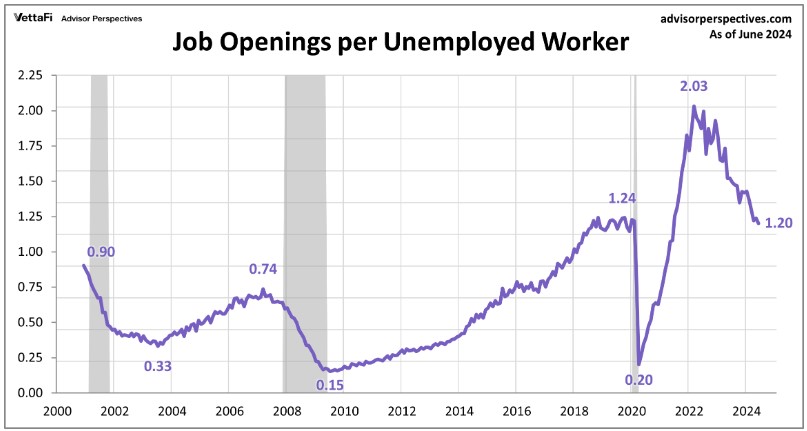

Job Openings drop lower than expected.

JOLTS (Job Openings and Labor Turnover Survey) came in lower than expected, with numbers falling from the anticipated 8.1M to 7.7M.

At some point, actual jobs will be affected. Remember, this is the Job Openings number—another datapoint the Fed is closely watching.

The quit rate was reported at 2.1%, the same as last month and the lowest level since 2018 (excluding COVID data).

ADP Employment and Initial Jobless Claims are set to be released tomorrow, with the BLS Jobs Report coming out on Friday. Friday’s report could be the deciding factor that pushes the Fed towards a 50 basis point cut on the 18th.

That’s just my perspective, but it’s what we’re expecting.

Mortgage bonds have reacted positively this week, and we expect this trend to continue.

Remember, our team offers a soft credit pull. Let’s get your application tuned up and ready for a refinance or purchase.

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.