I had asked ChatGPT to rewrite my original headline “important inflation numbers this week.”

The Consumer Price Index (CPI) and the Producer Price Index (PPI) are set to be released this week. These reports are eagerly awaited indicators of inflation in the market.

We expect a decrease in the inflation figure, but the challenge lies in comparing or replacing figures in the year-over-year calculations.

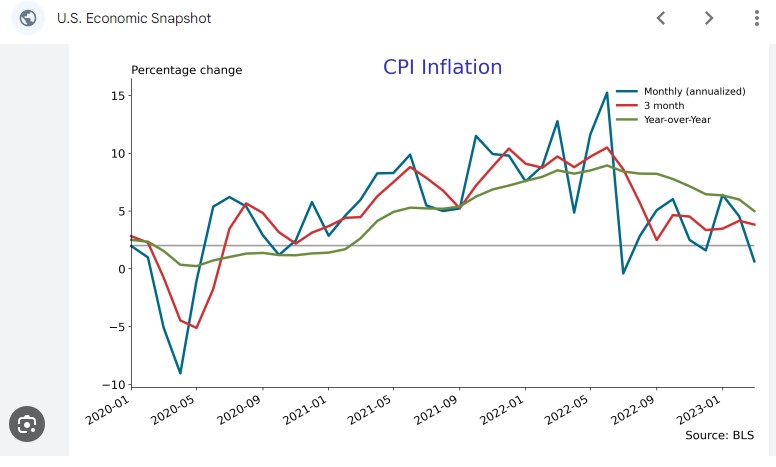

The graph below illustrates the difference between month-to-month, three-month, and year-over-year analyses.

The Bureau of Labor Statistics (BLS) reported the creation of 199,000 jobs in November, slightly stronger than the expected 190,000.

The birth/death model contributed only 4,000 jobs, virtually having no impact. This model considers the birth and death of companies and analyzes the trend in their ratios.

Average Hourly Earnings, which examines wage pressure from inflation, rose by 0.4%, a bit higher than expected.

Average weekly hours worked increased from 34.3% to 34.4%, a minimal rise, resulting in a 0.6% increase in weekly earnings.

In summary, it’s not the ideal jobs report for the bond market. The trend in job growth is clearly lower, yet undeniably strong.

Federal Reserve Chair Powell will likely maintain a hawkish stance, i.e., holding or potentially raising rates at next week’s meeting, though uncertainties persist.

All in all, the market did react, bringing positive news for interest rates.

The November Jobs report will be released tomorrow morning. The BLS Jobs Report estimates 180,000 jobs added year-over-year, with the unemployment rate expected to remain at 3.9%, and average hourly earnings to decline from 4.1% to 4%.

What this means is continued data pointing towards a soft recession or the absence of one.

Jobless Claims, which measure individuals filing for unemployment benefits, rose by 1,000 to 220,000. While not a significant increase, it’s noteworthy. Continued Claims, indicating those who continue to receive benefits, fell by 64,000 to 1.861 million.

This suggests a weakening labor market, providing another data point for the Fed’s consideration.

The CoreLogic Home Equity Report in Q3 shows a 6.8% year-over-year increase. This is attributed to amortization (mortgage payments over time) and appreciation, with the average Loan-to-Value (LTV) ratio at 42%. It means you have 58% equity in the house.

It’s worth noting that during the Bubble years, the average LTV was 81% or 19% equity.

What this means is get off the couch and buy a house….

Anticipate significant data in tomorrow’s Jobs report. Hang on and have a great rest of your week.

We begin the day with stocks higher and Mortgage Backed Securities, i.e., Bonds, lower, bringing rates down.

The ADP Employment Report indicates an increase of 103,000 jobs created in November, slightly below expectations of 130,000. The previous month’s figure was revised lower from 113,000 to 106,000.

The Mortgage Bankers Association released their Mortgage Application Data for the week ending on 12/1, showing a 2.8% increase. Perhaps someone out there is paying attention and getting prepared.

What does all this mean? It’s more data telling us that the economy is slowing down as expected, nudged or pushed by the Fed rate hikes. This implies that we may see those Fed rate cuts sooner rather than later. It also means we should start seeing further declines in mortgage rates. So, get ready, put on your seatbelt, and get pre-qualified.

My idea is simple: look forward, not backward. It’s almost impossible to drive a car while constantly looking through the rearview mirror.

The CoreLogic Home Price Index rose by 0.2%, bringing it up by 4.7% year over year.

According to Black Knight, home prices increased by 0.2% in October and are now 4.6% higher year over year.

The JOLTS report for Job Openings and Labor Turnover showed a decline from 8.7 million to 9.25 million, while we expected 9.3 million. This slowdown in the economy wasn’t good news for my two recent graduates looking for work, but it does contribute to overall inflation and recession data. The Quit rate remains at 2.3%, unchanged.

In Leisure and Hospitality, there were 1.2 million job openings, reflecting a 10% decrease or 136,000 fewer openings. This suggests that the post-pandemic re-employment in this sector has completed.

Rates continue to improve. Will Powell indicate a Fed rate cut sooner rather than later? I think so.

Now that I have your attention, let’s talk rates, mortgages, and the Fed. With the holidays upon us, the inevitable question at gatherings is, ‘What do you do?’ The next question is, ‘When will rates drop?’

The short answer is, no one knows. That’s the safe response. However, given that I woke up way too early this morning, even for me, I’m not feeling safe.

There are strong indicators that rates will drop. Inflation is set to decrease significantly. The car industry has returned to reality, and big-box companies may have overstocked their shelves. It’s all about supply and demand.

Supply is up, and demand is waning. Oil prices have also declined, including rent, particularly with commercial rentals. We are running out of Pandemic government money and waking up to the correct reality.

I am excited for 2024.

Look for the Fed to make overtures in January/February for potential rate cuts. Home inventory will grow, as will demand. Get ready for 2024.

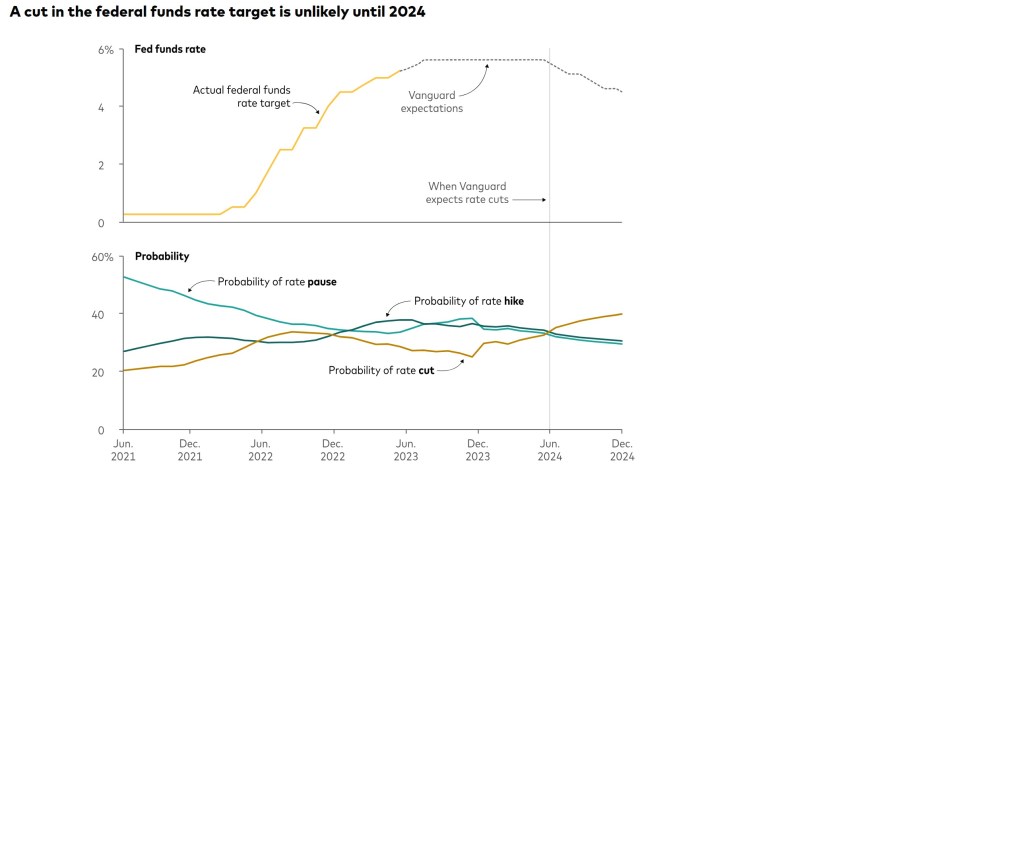

Translation: Feds will hold Fed Rates and eying cuts in 2024

Fed Chicago Pres Austan Goolsbee said that worries by economists that inflation would get stuck above 3% have been proven unfounded. “I just don’t get that. There’s no evidence that we are stuck at 3%.”

Translation: We will hit the Target 2% inflation number sooner than later.

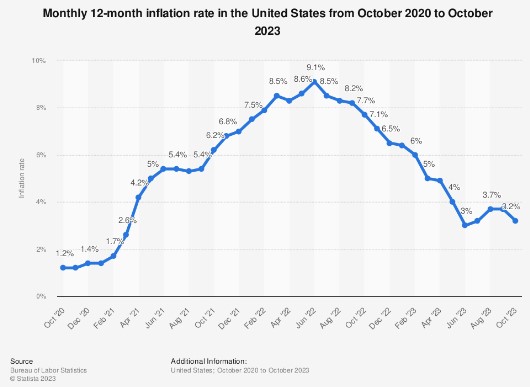

PCE, Personal Consumption Expenditures is the Fed’s favorite measure of inflation year over year, the index decreased from 3.4% to 3%. CPI as we mentioned yesterday was down as well.

Looking at the last 6 months of core readings (strips our food and energy), which Powell mentioned at the last meeting shows the core inflation at 2.4%.

What this means is the rates will likely continue to drop. The Fed’s may cut rates as soon a March. Three months ago, this was not even on the radar.

If you are looking to sell or ready to buy, get prepared. If your a Realtor, get your clients pre-approved and ready to go.

We are here to help with the pre-approval process.

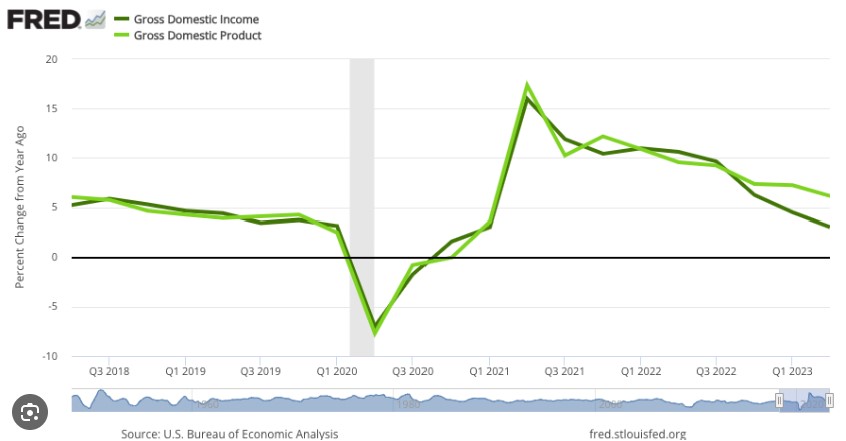

The Gross Domestic Product (GDP) increased by 5.2%. Why does this matter? The data from the July to September period serves as another indicator pointing to a booming or robust economy, defying gloomy warnings of a slowdown.

GDP measures the value of the final goods and services produced in the United States.

What else is going on? The Q3 data reflects stronger spending by corporations. It also shows increased state and local government spending and imports.

Here’s the kicker: Gross Domestic Income (GDI) increased rapidly compared to the second quarter, with GDP increasing by 1.5%, a full percentage point above the last quarter.

GDI stands for Gross Domestic Income, representing the total income generated by all sectors of an economy within a specified time period. This includes employee wages, profits from businesses, taxes, and costs incurred in production.

How does this affect mortgage rates? Surprisingly, bond market yields have been dropping, as have rates.

The Case Shiller Home Price Index, considered the ‘gold standard’ for home appreciation, indicates a 0.7% increase in home prices in September, marking a 3.9% rise from last year. The index is on track for a 6% appreciation this year.

Apartment List Rental Data’s November Rental Report reveals a 0.9% decline in new rents for November, down 1.1% from the previous year. This marks the fourth consecutive monthly drop.

This is referred to as a Shelter Cost, a substantial component of inflation, similar to the drop in oil prices this year.

What does it all mean? Inflation is continuing to decrease, surpassing the Federal Reserve’s expectations. As we reflect, we might find ourselves thinking, ‘I wish I had been more prepared for 2024.’ Consider me your time-travel buddy; 2024 has yet to arrive, so you still have time.

Below is the link to a Buy vs. Rent video I created, illustrating the advantages of purchasing a home. I’m sharing the longer 4-minute video, but the 2-minute version is also available. Feel free to forward .