I listened to Austan Goolsbee this morning, and he shared a powerful analogy. He said the Fed is like someone constantly reading data and sniffing everything out, but eventually, you have to start walking—taking action.

He also touched on the concept of transitory – one month of change isn’t the same as four months. He was referring to tariffs and their ongoing impact on inflation, suggesting that short-term shifts don’t always stay temporary.

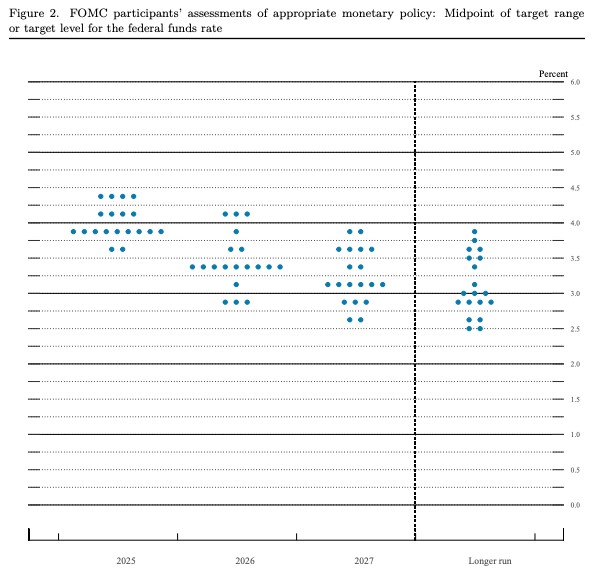

The Dot Plot below represents the The Federal Open Market Committee FOMC 12 members. The trend is lower Fed rates, lower Mortgage rates.

We all have a tendency to delay things that may be critically important. Every now and then, it’s worth looking up to check the ceiling before a leak appears.

From a mortgage standpoint, we encourage our clients to get fully approved through underwriting before purchasing or refinancing. Rates are starting to move in the right direction, and once they shift significantly, the rush will be on. Being prepared now can put you ahead of the curve!

Now lets get to the data:

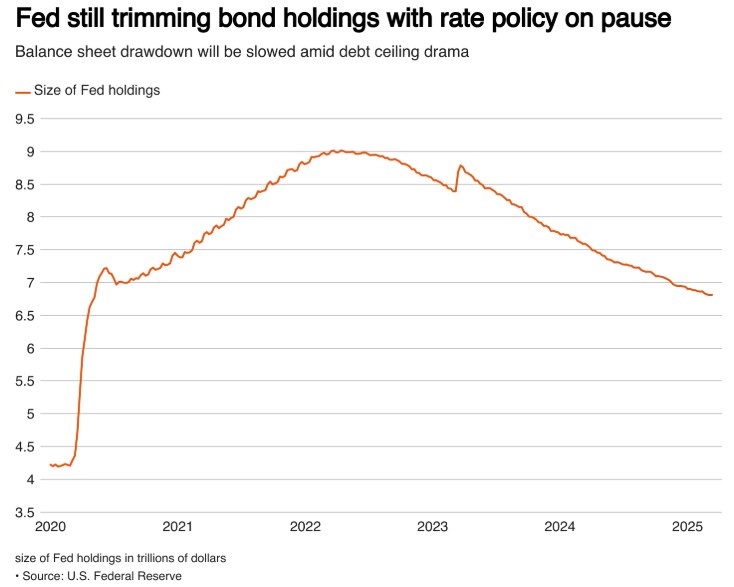

The Fed kept rates unchanged, as expected, and made key adjustments to their balance sheet runoff. Previously, they allowed $25B in bonds to mature and be paid back instead of reinvesting. Now, they’re making changes to this process by re-investing. which could impact the market.

Simply put, Quantitative Tightening (QT) means reducing the Fed’s balance sheet by letting bonds mature without reinvesting. Quantitative Easing (QE) is the opposite—it involves reinvesting those funds to keep money flowing in the economy.

These are all signs of future lower Fed rate and Mortgage rates.

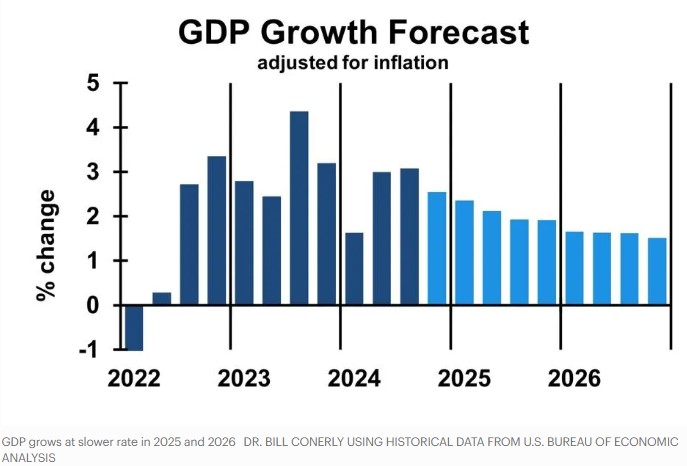

The Summary of Economic Projections (SEP) provides insight into where the 19 Federal Reserve members anticipate key economic indicators, including the unemployment rate, GDP growth, core PCE inflation, and the direction of the Fed Funds Rate.

Let’s take a look back at the last SEP report from December 18th:

Unemployment Rate: 4.3%

GDP Growth: 2.1%

Core PCE Inflation: 2.5%

Fed Funds Rate Projection: 2 cuts

Current Expectations:

Unemployment Rate: 4.1%

GDP Growth: -1.8%

Core PCE Inflation: Trending lower

Fed Funds Rate: No clear guidance

Additionally, the Fed may announce an end to its balance sheet runoff, which involves selling bonds. If this happens, there’s a strong possibility they will begin reinvesting approximately $40 billion per month back into Treasuries (Bonds)—a move that could provide positive momentum for mortgage rates.

Gold has a unique and complex relationship with GDP. Let’s break it down.

The latest Q1 2025 GDP estimate from the Atlanta Fed sits at -2.1%. However, when factoring in gold, the adjusted GDP figure moves closer to zero. Next report scheduled for release Thursday, March 27th.

Here’s why: Strong GDP growth often leads to higher interest rates, which can reduce demand for gold. On the other hand, economic uncertainty or a weakening economy tends to push investors toward gold as a safe-haven asset, influencing the overall economic landscape.

The Feds are paying attention. They are wrapping up their meeting tomorrow afternoon. At that point we will compare their projections on Fed Funds Rate, inflation, unemployment and the DDP from their last meeting.

Why do mortgage rates change? The answer is complex. It’s like looking through a peephole—catching only glimpses of the full picture and making educated guesses as the image gradually comes into focus.

My take on this: Rates are trending downward. As always, be ready—especially if you’re considering refinancing. When the shift happens, things will move quickly, and you’ll want to be prepared.

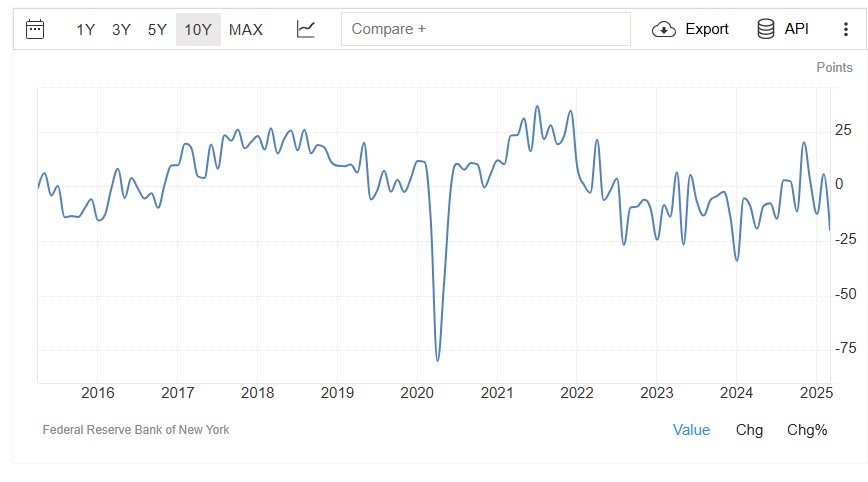

The Empire State Manufacturing Index dropped to -20, significantly weaker than the expected -1. New orders index also dropped 14.9 as well as shipments index to -8.5.

Looking at the long-term trend in the graph, it’s clear that this index has been quite volatile. Let’s take a closer look to determine whether this decline is a serious concern.

Inventory continues to grow. This is concerning. Business optimism continues to decline while prices rose at the fastest pace in two years.

The Fed must consider whether to cut rates sooner rather than later or risk falling into analysis paralysis.

Inflation declines when consumers opt for chicken over beef and brew their own coffee instead of buying Starbucks. Supply and Demand.

The case for lower interest rates is stronger today than it was yesterday. Now is the time to get your mortgage paperwork in order—let’s get you pre-qualified for your purchase or refinance!

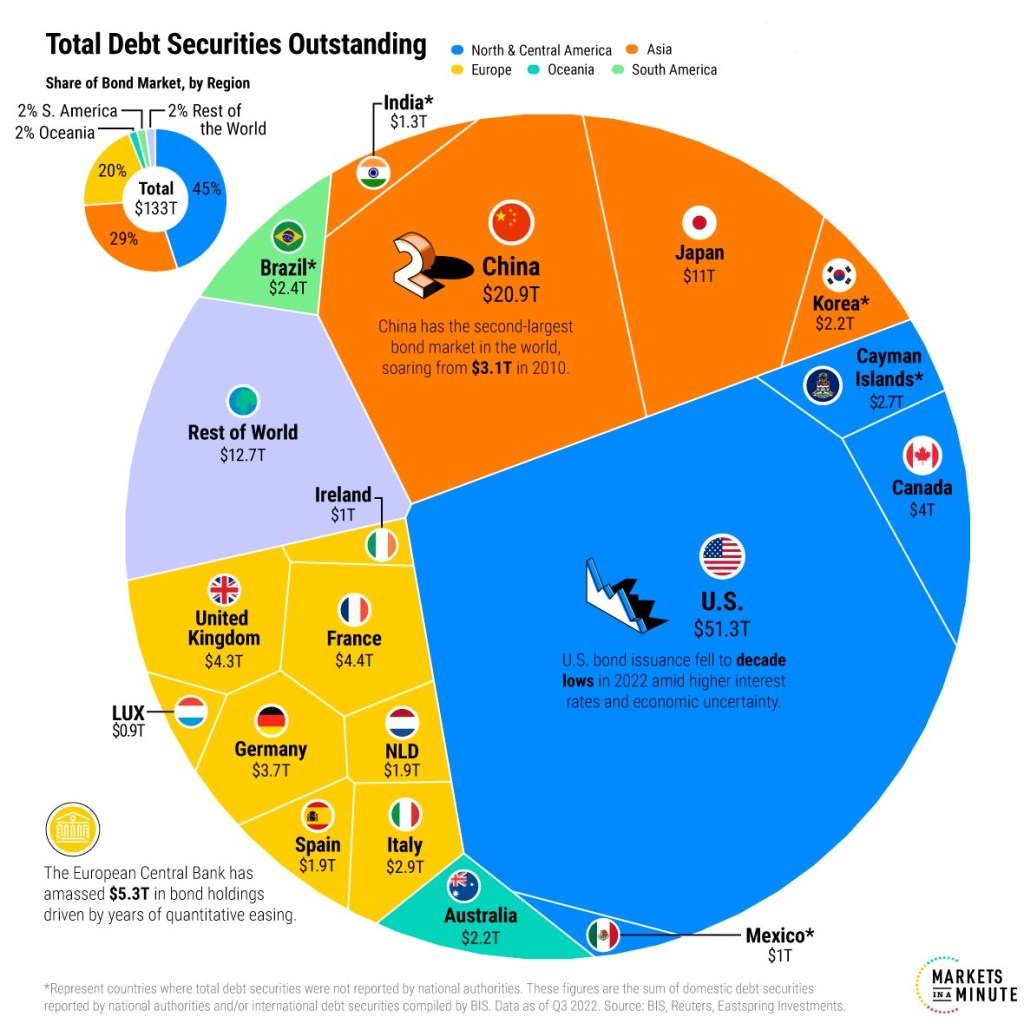

In Global financial markets, there is always competition to attract capital, regardless of the product being offered, and bonds are no exception.

Investors have a wide range of choices, from stocks and real estate to commodities and alternative assets, all vying for their funds. To stand out, bond issuers—whether governments or corporations—must offer competitive yields, favorable terms, and a strong credit profile to attract buyers.

Factors like interest rates, inflation expectations, and economic conditions further influence how bonds compete with other investment options.

In essence, just like any product in a marketplace, bonds must continuously adapt to investor demand to remain an attractive choice.

Mortgage rates have declined since the turbulence of the tariff war but now appear to be stabilizing. The outlook for April 2nd remains uncertain, but we’ll have to wait and see how things unfold.

I’m scratching my head. Yesterday, the Consumer Price Index came in cooler than expected, and we saw a strong 10-year auction—yet the bond market barely reacted.

Today, the February Producer Price Index, which measures wholesale inflation, also came in much lower than expected (0.0% vs. 0.3% forecast).

So, what’s going on? The markets are fixated on tariffs and the trade war. This morning, Europe announced tariffs on American whiskey, and in response, Trump threatened a 200% tariff on certain European wines and spirits.

Imagine a group of kids in a sandbox, each claiming their corner as their own. One child takes another’s shovel, so the other retaliates by knocking over their sandcastle. Soon, they’re all piling up sand barriers, blocking each other’s toys, and making it harder for anyone to play.

That’s the trade war—countries imposing tariffs and restrictions, retaliating against one another, and ultimately making it more difficult for everyone to thrive. Just like in the sandbox, the more they fight, the messier it gets, and in the end, no one wins.

The kitten (bonds) keeps defying gravity, but it won’t hold on forever. When yields drop, they’ll drop fast. The flight to safety is real—and it’s happening now.

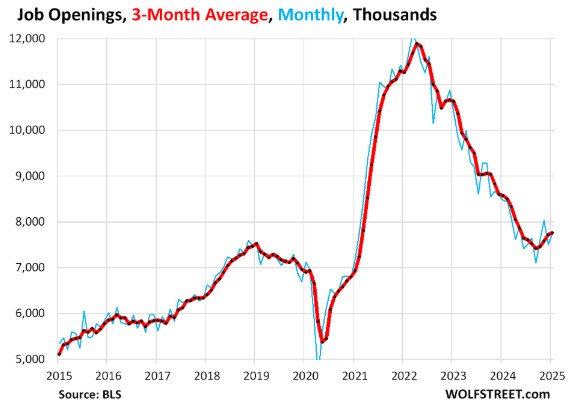

The Job Openings and Labor Turnover Survey (JOLTS) showed a slight increase in job openings, exceeding estimates. However, December’s data was notably weak, and the long-term trend continues to decline.

The BLS Jobs Report saw downward revisions for every month in 2024, totaling a negative adjustment of 263,000 jobs from the original reports.

The Small Business Optimism Index (NFIB) dropped 2 points in February, with the percentage of businesses expecting economic improvement plunging 10 points to 37.

The Atlanta Fed’s Q1 GDP estimate remains negative at -2.4%, with other major forecasters like Morgan Stanley and Goldman Sachs projecting around -1.9% for Q1 GDP.

When thinking about inflation, consider supply and demand. A shift in consumer mindset—such as skipping Starbucks, postponing travel, or choosing chicken over steak—can quickly alter demand and increase supply, impacting overall price levels.

Even if unemployment rises to 5%, that still means 95% of the workforce is employed.

Now is the time to start your home search—get pre-approved and let’s make it happen!

This week’s inflation data is a mixed bag. Shelter costs, which make up 42% of the CPI report, are expected to continue their gradual decline.

Energy prices dropped 6% in February, accounting for 16% of the CPI report.

Keep in mind that inflation is measured as a percentage change over the past 12 months. February 2024 saw high inflation across the board, so while the current numbers may still seem elevated, they reflect a slight decline compared to last year.

What Does This Mean for You?

Global uncertainty, fueled by an escalating trade war, has led to a flight to safety—Bonds. This surge in bond demand pushes prices up and yields down, which in turn helps bring mortgage rates lower.

On the ground, I’m seeing much more market activity compared to last year. If you’re looking to buy a home, expect more competition. If you’re considering refinancing, now is the time to get your paperwork in order so you’re ready to act when rates take a significant dip.