The FHFA just announced a major shift:

Fannie Mae and Freddie Mac will now accept VantageScore 4.0 for mortgage qualifications.

Why does this matter?

Because an estimated 5 million new borrowers, many of them younger, new-to-credit, or underrepresented, could now enter the housing market.

FICO vs. VantageScore 4.0: What’s the Difference?

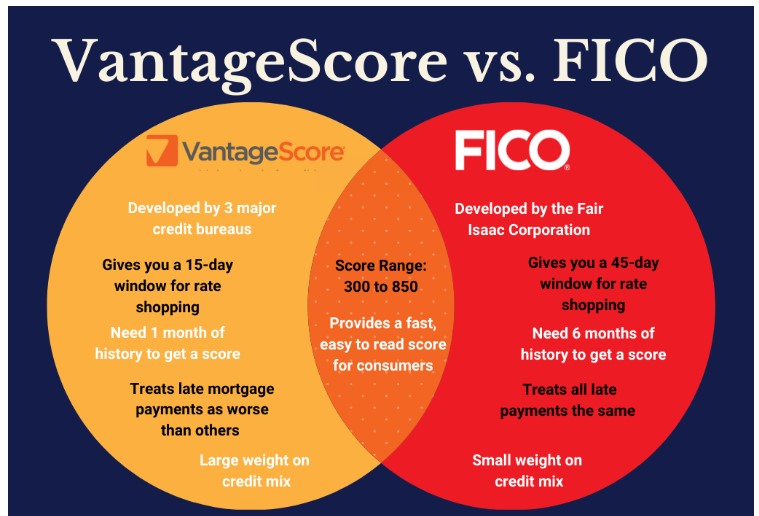

The Similarities:

- Both use your credit report to generate a score.

- Both score on a 300–850 range.

- Both consider factors like credit utilization, payment history, and credit length, just with different weightings.

The Key Differences:

- Credit History Requirements:

- VantageScore: Needs just 1 month of history.

- FICO: Requires 6 months of history.

- Score Versions:

- FICO: Has industry-specific scores (Mortgage, Auto, Bankcard).

- VantageScore: Uses one universal score.

- Payment History Weighting:

- VantageScore places more emphasis on your payment history compared to FICO.

Why This Is a Big Deal

This change opens the door for:

- First-time buyers with limited credit history

- Renters with strong recent credit activity

- Borrowers shut out by traditional scoring models

Want to know if VantageScore could help your clients qualify, or re-qualify? I’m happy to run the numbers. Just reach out!